Basic Concept of Accounting By Saheb Academy - Class 11 / B.COM / CA Foundation

5.38M views6086 WordsCopy TextShare

Saheb Academy

In this video I have explained the basic concept of accounting in a simple way and this is especiall...

Video Transcript:

hello everyone you're watching sahab Academy if you like our videos then please subscribe to our Channel and also hit the Bell icon for the regular updates and also follow us on Instagram sahab Academy now let's go to the video hi everyone in this video we are going to discuss the basic concepts of accounting what is accounting how do we do this yeah why do we do it and what is the process of accounting and what is debit credit and all these basic things we are going to see in this video and this video is especially

for the science students who come from a different background right other than the Commerce background students and this is a very simple and straightforward video so please make sure you watch this video till the end to understand the whole concept of accounting very practically and logically right let's start this video now first let's understand what is accounting see here accounting is very simple see in the company what happens in a company there will be lots and lots of financial transactions happening on daily basis right so there will be lots of financial data being generated yeah

so many transactions are happening so many bills receipts vouchers are creating yeah so many things are happening so now here in accounting what we do is as an accountant we record that data properly yeah that financial data yes we record that data yeah not only record that we classify that data properly in a structured format and then what we do is we summarize that financial data into meaningful format that financial data which is being generated we have to record that classify that and then summarize that properly into meaningful format why into meaningful format and how

into meaningful format see here why because because it has to make sense to the users of that financial information yeah who are the users of financial informations it can be management it can be shareholders or the owners of the business yeah it can be you know the government it can be creditors who the people who lend the money to the business or to the company yeah whatever it is so these are the stakeholders or what the users of financial information so this data has to make sense to them why because they can take meaningful and

constructive proper decisions based on that financial data yes so that meaningful format if I tell you basically it is what balance sheet and profit and loss account the balance sheet will give us the information of the financial position of that company all right balance sheet consist of what the capital assets liability we come to that later so all you have to understand is balance sheet gives us the financial position of the business and then profit and loss account or the statement if it's a company then that gives us the financial performance of the company yeah

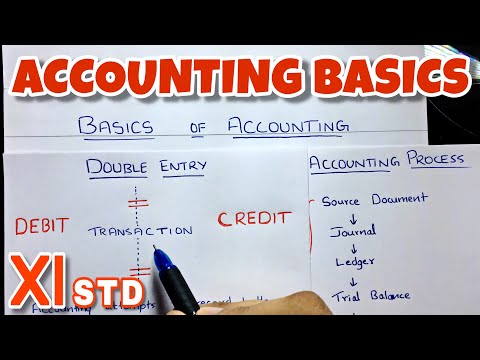

financial performance what is the profitability how well the business is doing right so this is a meaningful format yeah so what is accounting accounting is nothing but recording classifying and summarizing the financial data into meaningful format that's all that's all accounting is right so now let's see the accounting process see here the accounting process is very simple accounting process starts with the source document now what is Source document see here what do you do in accounting you record the data first right so to record any entry to record any transaction you need a source document

yeah the evidence of that transaction it can be a voucher it can be a bill it can be an invoice yeah whatever it is any evidence so that is called Source document a document right So based on that you are going to make an entry a journal entry in the journal book all right and then what you're going to do is you are going to create ledger accounts all right ledger accounts and then from that ledger accounts you will get so many balances debit balances and credit balances we'll come to that later all you have

to understand is we create ledger accounts and then from those ledger accounts we take all those balances and summarize them in one statement that is called trial balance yeah Source document pass the general entry create Ledger account it is called posting and then transfer all the balances to the trial balance and then at last we prepare financial statements yeah what are financial statements this thing only balance sheet profit and loss account only yeah so see here profit and loss statement balance sheet and there are more also cash flow statement and statement of changes in equity

yeah this you will see later so now you can understand this only profit and loss statement and balance sheet simple as that yeah so these are the financial statement that will be prepared at last yeah and the process from Source document till trial balance it is called bookkeeping okay a normal accountant will do this job bookkeeping yeah this is what bookkeeping is known as yeah from The Source document till the trial balance simple accounting job so this was the accounting process which takes long time yeah it takes long time to do all this all right

so this was the accounting process now we have to understand the elements of financial statement right so far we have understood the meaning of accounting and the accounting process now we have to understand the five elements of financial statement see here in accounting what we have is we have only five things okay always remember that in accounting we have only five things nothing more than that okay there is no six thing only five yeah and the entire accounting is based around this all right so the first is asset expense liability equity or Capital revenue or

income okay only these five things are there clear and these are also called as five elements of financial statements why because they are represented on the face of the financial statement this expense and revenue these two elements will be shown on the profit and loss statement and then these three elements asset liability and Equity or Capital this will be shown in the balance sheet okay they go to the balance sheet and these two elements go to the profit and loss statement so that is why they are also called as five elements of financial statement now

we have to understand this properly in depth so let's do that okay let's understand the meaning of each and every item properly let's do that now let's see the meaning of the asset first see here an asset is a resource controlled by an entity as a result of past events and from which future economic benefits are expected to flow to the entity that's what an asset is now previously we used to say that asset is something that the company owns if company owns the land in building then that's an asset of the company yes but

now the definition has been revised see here now asset is not something that the company owns but rather something that the company has control on yeah if company has control on something and there are future economic benefit from that then that's an asset simple as that yeah what does this control mean see here it can either be ownership yeah or if you can get Machinery or whatever it is whatever you can get on lease basis yeah by the way of lease agreement then also it means you have control over that and you can use that

and you can utilize the future economic benefit from that right what does future economic benefit means it means that you know if you have let's say you have Machinery Machinery is an asset yes so now that Machinery you will use for the production or whatever it is and then it will help you in the operations of your company and to generate the Revenue yes to generate the income isn't it so that's what future economic benefit yes so here control means what either you have ownership of that thing then that's an asset or you can get

it on lease basis then you have a control over that that asset yes so that Machinery which you can get on lease basis can also be recognized as an asset yes so an asset is a resource yeah controlled by an entity as a result of past event past event means that either you purchase that or you get it on lease basis yeah there has to be a past event you purchase that thing then that's an asset for you yeah because you got ownership of that and from which future economic benefit are expected to flow to

the entity always remember okay asset has future economic benefit if you purchase the asset today yeah if you purchase the asset today then for many years you'll be able to use that in your operations of the company and you will get value in future yes it is expected that you will get value in future so that's what an asset is now let's see the meaning of expense expense see here the meaning of expense an expense is the cost of operations that a company incurs to generate revenue and from which no further benefit is expected yeah

expense is what expense is an expenditure that you incur the cost yeah cost of operations yeah and from which no further benefit is expected yeah the main difference between asset and expenses that you know in asset we get future economic benefit yeah but here once you incur the expenses that means you have taken the benefit already the benefit is already taken for example yeah at the end of the month you pay the rent yes now are you going to get any more benefit from that no if you are paying 5,000 rent today that means you

have already taken the benefit yeah if you have paid the salary of your worker that means that person has already worked for you yeah he's getting the salary at the end you are paying the salary so that is an expense for you expense is something you know the benefit of which you have already taken yeah no further benefit is expected that's the simple logical definition of expense okay expense is the cost of operations that a company incurs to generate Revenue yes you are incurring these things you are paying the rent you are you know paying

the electricity bills you're paying the salaries of your workers because the operations can be run smooth L and you will be able to generate revenue from that yeah yes and from which no further benefit is expected this is the main point okay no further benefit if you pay the electricity bill that means you have consumed the electricity yeah you are not going to get any more electricity from that money itself yeah if you get an electricity bill of 2,000 Rupees that means you have used that much of electricity yes now you paying that 2,000 that

means that's an expense for you now that 2,000 you can't say give me back or something like that yeah you are not getting any benefit anymore you have already utilized the benefit yeah you have already utilized the benefit clear so that's what an expense is now let's see the meaning of liability see here liability is very simple see liability liability is a present obligation of the entity to transfer an economic Resource as a result of past event now what does this mean see it's very simple a present obligation right now there has to be an

obl liation to The Entity your company has to pay something do something or abstain from doing something beneficial yeah so see here a present obligation of the entity to transfer an economic Resource as a result of past event there will be some past event for example you purchased you know 10,000 worth of goods yeah and you didn't pay then you have a present obligation to pay that person pay to pay your supplier yeah so that is what the last event is you purchase those goods yeah now the present obligation is you have to pay in

somewhere in future yes and what you have to pay you have to pay him cash so transfer an economic resource so that economic resource will be money the cash you have to pay in future yes so you're understanding yeah so liability is a what a present obligation of the entity to transfer an economic resource to do something as a result of past event yeah it is a claim of Outsiders on on total assets of the company yes if you owe money if you owe money to your supplier then that supplier that creditor he will have

claim on your total assets of the company okay so that's what a liability is clear it's just an obligation financial obligation of the entity to transfer an economic Resource as a result of past event you purchase Goods on credit yeah you didn't pay the money so now you have to pay so that's an obligation what you have to pay cash economic resource something you have to give or you have to do as a result of past event past event is you purchasing the item yeah the goods clear so that's what a liability is yeah now

that person that creditor will have the claim on your assets of the company yeah the asset means the cash or whatever it is but it will have the claim on total asset of the company we'll say total assets okay that's what that's what a liability is then we have to see what Equity is equity or Capital now what does this mean see here it's very simple capital is the money that is invested by the owners of the business right whatever money the owner brings into the business that's called Capital simple as that but now you

will be wondering why do we have two names over here you are saying Equity or Capital why two names that's because it depends upon the different types of organization if it's a simple partnership business There Will Be Few owners right who will bring in the money and we can just call it A's Capital B's Capital like that yeah Whoever has Brad the capital and then if it's a sole proprietorship business then we can just call Capital simple as that yeah but now why am I saying Equity that's because you know if it's a company then

in company we don't have few owners no we have thousands and hundreds and thousands of owners right shareholders we call them shareholders because there in company the capital is divided into small small units of shares yeah so that's share Capital yeah so it may be equity share capital or preference share Capital as the case may be so that's why we call it Equity all right it's just different names but the concept Rule and meaning is same only okay see the meaning over here it's same only okay whatever money that is brought in by the owners

of the company that's called Capital yeah either it's just capital or equity share capital or preference share Capital simple as that okay don't worry so see the technical definition over here it is the residual interest in the total assets of the entity after deducting all its liabilities yeah so why is it called residual interest because the equity the owners what do they get they get whatever that is left right whatever that is left that is what they get okay see here when the company you know company wounds up you know what the owners will get

the owners will get whatever that is left okay first the liabilities will be be paid and then the their Capital will be paid so that is what is meant by residual interest they have a claim yeah the owners it is the claim of owners if someone asks you what is capital then the technical definition would be it is the claim of owners in the total asset of the company after deducting all its liabilities why am I saying after deducting all its liabilities because whenever you know if you remember the definition of liability yeah they also

have a claim the claim of Outsiders we have to pay to liability holders right obligation we have an obligation we have to pay something do something so that has to be done first and then the claim of owners will come okay so whenever there will be a liquidation or the company will wound up first payment will be done to the liability holders and then to the owners so that's why these people the liability holders will have first claim these people owners will have second claim all right on the total assets only total asset of the

company total asset of the company okay so this is what equity share capital or just capital is it is simply claim of owners in the total assets now we'll come back to this okay with an example to understand how does that mean okay the claim of owners and the total asset of the company we'll take an example and understand it properly don't worry we'll come back to this but let's see the revenue definition first all right so did you understand what capital is simply whatever money that is invested by the owners of the company company

that's capital and the technical definition is they have a claim it's a claim of owners in the total asset because the owners have a claim clear yes so now let's see the revenue definition see here the revenue definition is very simple yeah what is Revenue income simple as that yeah it is the gross inflow of cash yeah it's inflow that's all it's a gross inflow of cash yeah either cash is coming in or receivables receivables means what receivables means someone has to pay to us all right yeah someone owes US money so they have to

pay to us so we are getting income so that's receivables or other consideration it can be you know uh see other consideration arising in the course of ordinary activities of business such as sale of goods yeah if we sell the goods then we'll get the money right yes so sales is our revenue and then rendering of services if it's a service business then we will render the services we will not make sales we will render the services and we will get the money Etc and also interest received all these things okay other things also Etc

means right interest received rent received whatever it is dividend received whatever we get whatever income we get that's called Revenue simple as that yes so now let's see one example to understand practically yeah all these elements yes now here we have the example see here let's say you have a sole proprietorship business you are a single owner and you started your business with one lakh Capital all right now this is the balance sheet yeah here we take Capital liabilities on the left hand side and and on right hand side we take what we take all

the assets yes so now what I said you have a business and you started your business with the one lakh yes so now one lakh means what you have cash of one lakh now in your business yeah yes and you have invested Capital right so here you have to show the capital capital 1 lakh clear so now how is the cash our asset how is it our asset that's because see the definition of an asset asset is a resource controlled by an entity do we have control over this cash of course we have yes you

invested money here so you have control over that yes and future economic benefit do you have future economic benefit from that of course you have you can do whatever you want from this cash yes you can invest it somewhere you can do whatever you want so you have complete control as well as future economic benefit is there so this is your asset clear yes and how is this your Capital this is your Capital because you invested this money yes and now you have claim on the total assets of your company now total asset of your

company is 1 lak only so you have entire claim on this one lakh is that clear yes that's what I said in the definition of capital right yes now let's say you purchased a Machinery to do business yeah you wanted to do some production or something yeah so let's say you purchase Machinery of 20,000 clear yeah and this was a cash transaction you paid cash immediately so of course your cash will reduce yes your cash will be now only 80,000 because you have purchased Machinery of 20,000 now what is this Machinery this is an asset

of yours how is it an asset because you have control over it you own it right and you expect future benefit from it because you will use it in production or something and it will help you to generate income yes future economic benefit is there so this is your asset clear then let's say you wanted to invest in a huge project so you needed more money right so what you did was you went to a bank yeah you went to bank you went to a bank and you got a loan of 40,000 yeah let's say

you got a loan of 40,000 now what will happen when the loan is sanctioned immediately two things will happen one thing is you will get the cash yeah you will get the cash immediately yeah it will be your cash 40,000 cash you got but now there is an obligation that is being created now yeah immediately obligation is being created that you have to pay 40,000 back to the bank isn't it so this obligation is called what this obligation is called now liability a present obligation yeah present obligation now obligation is there you have to pay

to the bank yes you have to yeah what you have to pay you have to pay them cash transfer an economic resource that's cash why because as a result of past event what was the past event the past event was you took a loan from them you took what you took a loan from them them yeah this was the past event yeah present obligation is there you have to pay you have to transfer them economic resource and that economic resource is Cash simple so that's what liability is yes so now immediately you have to recognize

on the face of your balance sheet that you have got a liability and that liability is bank loan rupees 40,000 is that clear I told you right here we take all the capitals and all the liabilities yes yeah then here cash also has to be increased because you have got an asset also now yes you have got your own cash also now 40,000 from the bank yes it's the bank cash but now you own it so it's your cash now so 40,000 yeah so it will be increased so 80 + 40 is 1 lakh 120

so now the cash that is there is 1 lakh 220,000 is that clear does that make sense yes so you see see this now what is happening Capital before you had claim on the total assets of the company yes but now there is liability holder also Outsider also now this guy this Bank also has a claim on your total assets of the company what is the total asset see here let's tally the balance sheet 140 yeah 1 l40 here the capital and liabilities is 1 lak 140 it will always be equal okay 1 140,000 yeah

120 + 20 is 1 140 so so now you also have I mean the owner you also have claim on the total assets of the company if you see the definition of equity Capital see here it is the claim of owners in the total assets of the company after deducting all its liabilities residual interest yeah whatever that is left that's yours that is what is meant by Capital whatever that is left so now what is left what is left if you want to see that then simple see here the liability holders they also have a

claim so their claim comes first then your claim comes okay the first priority goes to the liability holders and then the owners okay so these people will have claim on the total assets and also you but you will get only after deducting liabilities okay your claim is only one lakh so your claim is one lakh means that what total asset is total asset is 1 l40 after deducting all its liabilities it will be your capital lak 40 minus liability 40 1 lakh 1 lakh is your claim 1 lakh is your Capital yeah so what is

capital it is the claim of owners in the total assets after deducting all its liabilities yeah after deducting the liability whatever that is left whatever residual interest is there that's yours okay that's the owner's capital is that clear yeah so that is what it practically means yeah whatever that is left that is the owners okay and the liability what it is a claim of Outsiders on total assets of the company clear so did you understand this practically simple and what was the asset something that is controlled by the entity as a result of past event

and future economic benefit should be there yeah you can do whatever you want with the cash yeah you can do whatever you want with the machinery and you can expect that you will generate income revenue from this Machinery yeah you will use it in the operations yeah and you will do business you will sell the whatever you produce with that machinery and you will earn income yeah that's what an asset is Machinery is an asset cash is an asset clear now let's understand a double entry concept yeah let's go there are you clear with Equity

liability and everything yeah simple yes let's go to the Double Entry Double Entry what is this double entry see here it's very simple to understand in accounting what we do is whenever we recall the transactions we follow this methodology that is called double entry where we record two aspects of every transaction and every transaction will have two aspects or two effects all right one effect will be debit and another effect will be credit but now you will ask me what is this debit and credit see here debit and credit doesn't mean anything these are just

two abstract terms that we use in accounting to represent something okay and that's something you will understand once you start building the concepts of accounting yeah when you will learn how to pass the general entries and the balances of accounts then you will understand what is this debit and credit yeah directly I cannot tell you what it represents or what what it you know what it means actually yeah because it doesn't have like that meaning if I ask you what is plus what is minus can you tell me you will say plus is ADD minus

is subtract but what is ADD what is subtract what is that it doesn't have any meaning itself but if you tell me 2 + 2 is equal to 4 yeah then it makes sense similarly here it will make sense when I relate this with assets liability and everything okay so wait for that just remember that debit and credit you know they just signify The Duality principle or aspect okay we'll come to that see here we were in Double Entry so in Double Entry what it means that you know every transactions have two effect debit and

credit and both of them are recorded okay accounting attempts to record both effects of a transaction or event on the entity's financial statements yes and those two effects are as I said debit and credit and every transaction will have One debit one credit okay and the effect of them will be equal always equal That's The Duality principle yeah that's what I said debit and credit represent The Duality principle or dual aspect principle of accounting all right yes so it will always be equal okay the FX will always be equal LHS equal to rhs clear so

this is what double entry is now I will relate this debit and credit with the asset and those these five elements then you will understand what is this debit and credit okay yeah because you can't say debit is Plus credit is minus something like that okay most of the people do that that's the biggest misconception they say debit is good credit is bad or debit is Plus credit is minus something like that no it's neither good neither bad okay it's not like that yeah it represents something else it represent The Duality principle okay so we'll

come to that now so do you understand what double ENT is yeah see here let me tell you let me show you see here in this transaction when we saw when we went to the bank when you went to the bank and when you got a loan what happened this transaction had two effects one effect was that you got the cash 40,000 yeah this was your asset isn't it and then here what happened immediately you had to recognize the liability also because a present obligation was created you have to pay so a liability was created

right so asset is there liability is there so this is the dual aspect I'm talking about yeah when you purchase the Machinery what happened when you purchase the Machinery there was Cash yeah asset this asset cash was reduced yes and then this Machinery 20,000 this asset increased isn't it so every transaction will have dual aspect it will have two aspect that is what is meant by double entry and both the aspects have to be recorded yeah we have got the cash when we got the loan we got the cash our asset increased over here and

here what happened the liability also increased we have to pay to the bank isn't it bank loan so that's what when you brought the money into your business what happened cash increased Capital also increased yeah so this is what yeah and one one of them will be debit and another of them and another will be credit okay so we will learn that so this is what is double entry okay every transaction will have two effects yeah do you get this yeah Bank example simple bank example when you got a loan yeah money is coming in

liability is also being created simple as that so Duality principle yeah now let's see what kind of balances does these five elements have yes these are the five elements right asset expense liability equity and revenue so now you must know what kind of balance es do they have yeah it will help you to pass the journal entries as well as to do The Ledger posting so entire accounting is based on this yeah modern equation and you will also be able to relate the meaning of debit and credit over here yeah listen to this properly so

see here asset always have debit balance asset always have debit balance why is that see I can't tell you similarly how you can't tell me why sugar is sweet why salt is salty or you know if you remember high school chemistry then why protons have positive charge and why electrons have negative charge you can't tell me that so similarly here I Can't Tell You Why AET have debit balance it just is okay that's it period yeah asset always have debit balance expense always have debit balance it's just a rule yeah so they always have debit

balance these two things yeah so whenever asset increases or you want to increase the asset then you have to debit the asset okay or when you want to increase the expense or expenses have been incurred then you have to debit that yeah and whenever you want to decrease any asset let's say you have sold off the asset or the value of the asset is decreasing then you have to credit the asset okay simple they have debit balance you want to increase them then debit them more yeah if you have a sugary drink you want to

make it more sweet then you have to add more sugar isn't it just like that yeah it has debit balance to increase it you will debit it more to decrease it you will do opposite credit simple as that expense also debit balance to increase you have to debit to reverse the expense sometime what we do sometime we make an error yeah expense never decreases if you want to reverse the expense then only you will decrease the expense by crediting it simple yes then liability equity and revenue they always have credit balance yeah credit balance always

credit balance so to increase them what you're going to do you going to credit them simple as that yeah Equity also Capital also Equity or Capital Credit balance to increase them you have to credit them yeah revenue or income whenever you get Revenue that means revenue is increasing so you have to credit Revenue yes whenever they decrease you have to do opposite you have to do debit simple this is the modern equation okay so from here you can understand that you know debit doesn't mean plus or minus and credit also doesn't mean plus or minus

you know it can be both it can be plus and minus also because it depends upon the type of element if it's an asset yeah for asset debit means plus yeah and for expense also what plus yeah debit means but for liability equity and revenue what it is minus isn't it so you can't say debit is good credit is bad or debit is only Plus credit is only Plus or only minus something like that yeah so just understand this modern equation it's very simple simple they have these debit and credit balances to increase them you

are going to do whatever the balance is simple as that clear easy right okay then so here I'm going to end the video yeah yeah simple so we saw so many things we saw the meaning of accounting and then meaning of the five elements yes what is asset expense liability equity revenue yeah liability means what they have claim on the total assets Equity or Capital means also they have claim on the total assets and then Revenue inflow of cash expense means what outflow of cash yeah and then asset means what asset means something you have

control or ownership on and you will get future benefit from that yes and this was the accounting process Source document you prepare the general entries so yeah in the coming videos we are going to see how to pass the general entries how to prepare The Ledger account and everything okay so stay tuned so I will make a separate playlist in that I'm going to upload all the basics of accounting okay okay okay then see you in the next video all right bye

Related Videos

45:07

How to Make Journal Entries by Saheb Acade...

Saheb Academy

2,185,292 views

33:53

LEDGER Posting with a Simple TECHNIQUE - C...

Saheb Academy

1,289,076 views

36:09

Jira Training | Jira Tutorial for Beginner...

Intellipaat

1,704,565 views

18:30

#1 Financial Statements - Concept - Easies...

Saheb Academy

27,066 views

43:57

William Ackman: Everything You Need to Kno...

Big Think

12,558,773 views

54:55

Excel for Beginners - The Complete Course

Technology for Teachers and Students

6,989,617 views

24:05

Golden Rules of Accounting with Journal En...

Saheb Academy

151,500 views

29:45

HARD Journal Entries by Saheb Academy - Cl...

Saheb Academy

1,280,778 views

45:15

How to do a full month of bookkeeping in Q...

Clara CFO Group

642,004 views

17:05

How To Pay Yourself As An LLC

Karlton Dennis

5,274,954 views

27:15

Accounting for Beginners | Part 1 | The Ac...

Counttuts

690,142 views

32:43

FA14 - Adjusting Journal Entries EXAMPLES

Tony Bell

426,691 views

9:45

Accounting Basics Explained Through a Story

Leila Gharani

1,424,303 views

34:45

Bookkeeping Basics

Halon Tax

406,738 views

22:05

Learn Accounting in 1 HOUR First Lesson: ...

Executive Finance

3,548,637 views

14:13

ACCOUNTING BASICS: a Guide to (Almost) Eve...

Accounting Stuff

3,104,122 views

27:26

Introduction to Accounting

365 Financial Analyst

482,207 views

34:47

Journal Entry Bootcamp

Tony Bell

183,643 views

18:33

FA1 - Introduction to Financial Accounting

Tony Bell

1,202,197 views

36:26

Learn Microsoft Active Directory (ADDS) in...

Andy Malone MVP

943,226 views