have you ever wondered how taxes might change when you retire typically when you're working it's pretty straightforward you simply pay federal and maybe state taxes on any income you earn as a salary unfortunately when you retire it's not quite as simple that's why in today's video I'm going to break down all the different types of income you can earn and how that's taxed as well as show you what you can do to lower that tax bill so let's Jump Right In and start going through the different types of income you might receive and explain to you how it's taxed but before we do let's start by actually understanding which taxes go away when you retire now by the way when I say retire I'm assuming that you're no longer working some people will retire and still have some part-time work but the first tax that goes away is what are called payroll taxes or FICA taxes on any dollar that you're earning as a salary so as a wage so not a dividend or capital gain or rent or anything like that but if you are earning a wage you have 6. 2% of every dollar taxed up to $168,600 now on top of this your employer is also paying 6. 2% taxes on all those dollars up to that base this is how Social Security is funded now any dollars that you earn above that $168,600 those are not subject to Social Security taxes anymore now another aspect of FICA taxes or payroll taxes is Medicare tax that's 1.

45% of every dollar that you earn and this is uncapped so whether you're earning $10,000 or $10 million $ 1. 45% of that is going to fund Medicare now while you're paying 1. 45% your empy employer is also paying an additional 1.

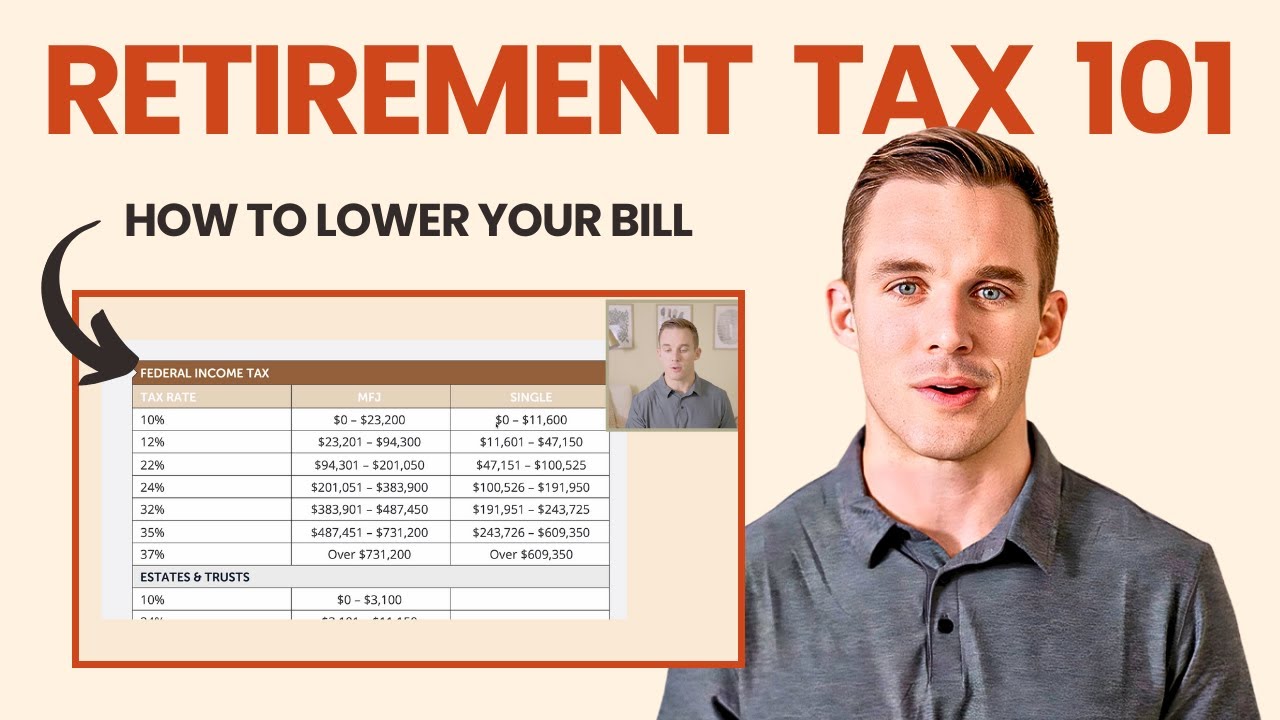

45% on every single dollar that you earn as a wage so to start if we're assuming that you retire and you have zero wage income anymore those taxes go away so the combined 7. 65% of taxes up to a certain wage base those are no longer being paid when you retire so what is being paid well what is being paid is federal taxes and depending on the state that you live in potentially state taxes as well but it's not a universal tax rate on different types of income so let's start to break that down now as we start to dive into the different types of taxes you're going to pay on different types of income it's really important that you understand the difference between ordinary income tax rates and long-term capital gain tax rates so I'm going to go over this real quick in the screen and by the way I'm going to include this as a free download so in the show notes below you'll have the opportunity to download this if you would like so what I want you to focus on in this chart here is what I'm looking at here this is the ordinary income tax rates that you are subject to based on different tax income levels So Married fining jointly if your ordinary income rate is between these thresholds then this is the marginal tax bracket that you're in for single if your taxable income is between these thresholds then this is the ordinary income threshold that you are in or the ordinary income tax bracket the year in and those tax rates go from 10% on the low end to 37% at the high end now those are different than long-term capital gain tax rates those tax rates can be seen here for married fining jointly for single as well as for Estates and Trust what you can see is these tax rates range between 0% to 20% depending upon your income level so I'm not going to fully go through that but like I said this is a free download below if you want to download this so you have access to this as a resource but it's important that you understand this differ between ordinary income tax rates in capital gain tax rates so we can start to understand how different types of income and retirement are taxed so with that in mind now let's start exploring the actual types of income that you might receive and probably the most common income that people will receive in retirement is social security income at the federal level anywhere between 0% and 85% of your Social Security income is subject to federal taxes and it's taxed at the ordinary income tax rate now when I say 0 to 85% that does not mean the up to 85% of your social security benefit is taxable it means up to 85% of your social security benefit is included in your taxable income so let's take a look at what I mean by that let's assume that your social security benefit for the year is $10,000 000 and let's assume that based upon your provisional income which is the income that Social Security looks at to determine what number between Z and 85% of your benefit is going to be included in your taxable income let's assume that the full 85% of your social security benefit is included in your taxable income so you earn 10,000 from Social Security let's also assume that you're in the 10% federal tax bracket what that means is that $8500 of the $110,000 in total benefit you have from soci Social Security is included in your taxable income it's then subject to your ordinary income tax rate which I'm assuming is 10% which means you end up paying $850 in taxes at the federal level on your social security benefit based upon a $110,000 benefit you received so effectively your tax bracket is 8 and a half% on your Social Security even though you in the 10% ordinary income bracket so that's how you think about social security it is fully subject to Federal ordinary income tax rates but only a Max of 85% of the actual benefit is included there now different states treat Social Security differently many states don't tax Social Security at all some of this is simply because the state itself doesn't Levy income taxes on its residents but some states that have quite high taxes so California for example where I live California has quite high taxes but does not actually tax Social Security benefits so this is very much a state-by-state issue but the majority of States either don't have a social security tax or they tax social security at a lower rate than you would be ordinarily subject to on other types of income so what can you do to minimize the taxes on Social Security well as I mentioned the amount that you pay on Social Security and taxes is based upon what's called your provisional income I made a video that you can check out right here where I walk through how does Social Security actually get tax what's included in that provisional income so check out that video if you want to see what I'm talking about here but in general most people pay close to 85% if not the full 85% of their social security benefit have that included in their taxable income the next type of income that you might receive is a pension now in general most pensions are fully subject to federal state income taxes at the ordinary income rates sometimes this isn't the case you know if you're a disabled veteran and you have a VA benefit for example that benefit is tax-free but the overwhelming majority of Pensions whether they're government pensions or state pensions are subject to taxes at the federal level and those taxes are based upon the entire pension amount so earning a dollar and a pension benefit is the same in many ways as earning a dollar in salary the only difference is you're not paying payroll taxes on pension income like you would be on a salary States it's a different story some states fully tax that pension as if it's fully included in your ordinary income many other states have exclusions for a certain amount of pension income so it's either not included in your taxable income at the state level or at least it's only partially included so for example if you live in California and you have a pension well the entire amount is included in your state income taxes versus if you live in Pennsylvania if you're above age 60 then Pennsylvania does not tax your pension at all so these are little nuances to be aware of of depending upon where you live your federal taxes will be the same but the state tax implications could be very different depending upon your state of residence next let's talk about interest how is interest tax when you're in retirement well first off I should say it's taxed the same am in retirement as it is when you're working but the type of interest that you're earning is what's going to determine how much of that interest is actually taxable let's say you have interest from your savings account at the bank or you have interest from a corporate bond that you're receiving semiannual coupon payments each year that interest is typically fully taxed so at the federal level it's fully included in your ordinary income rates so those are the rates that go from 10% to 37% at the state level it's typically included in that income as well although like I said some states treat different things differently but if you have interest from a savings account or a corporate bond or something like that it's going to be fully included at least at the federal level in your taxable income now let's say you have a treasury bill so you're lending money to the US government well that interest is fully subject to federal taxes but it's taxfree at the state level now being taxfree at the state level this might be irrelevant if you live in a state like Texas or a state like Florida where you're not paying income taxes anyways but if you're living in a state like California or New York or a state that has high income taxes that could be a very interesting benefit because not just the interest that you're receiving on that treasury bill that you're looking at it's the fact that that interest is tax-free at least at the state level so on treasury bills you are paying federal income taxes at ordinary income rates but you're not paying state income taxes on that interest then you have what are called municipal bonds so municipal bonds are bonds issued at the state level Municipal bond interest is taxfree at the federal level and if you are owning a municipal Bond within the state of your own residence so I live in California and I purchase a bond issued in California a municipal bond in California it's also typically tax-free at the state level so municipal bonds can be double taxfree at both a federal and state level if you are owning a municipal Bond within the state that you are also residing in however if you own a municipal bond from a state that's not the state of your primary residence that interest could be taxable now here's what you want to be mindful with bonds if you're owning bonds outside of a retirement account you want to be looking at it's called the after tax yield so if you go look at a bond or an interest rate that you're receiving on a CD or savings account typically we're looking at that number that's promoted on the brochure or the website or whatever it is that is a good starting point but really what we should be mindful of is what's the after tax yield on that CD or on that Bond some are subject to federal taxes but not state taxes While others are tax free at both the federal level and state level so don't just look at what's the yield on this Bond or the interest on this Bond understand what's the after tax yield based upon the type of bond it is and on your individual tax rate to understand what am I getting after taxes now I say do that in non-retirement accounts because if you're investing in a bond or a CD or something that pays interest inside of a retirement account well all that interest is either taxfree or tax deferred depending on the type of an account that it is and this is really important to know because a lot of clients will come to us and I'll see that their old adviser put municipal bonds in their Roth IRAs or their traditional IAS and we'll look at this and say why on Earth would we do this to own a municipal Bond we are accepting a lower yield than we could get on an equivalent type of bond this not immun Bond so why would we accept a lower yield if we're then going to stick that in an IRA or Roth IRA where it's taxfree or tax deferred anyways so make sure that when you're owning bonds you understand which account type is best to own it in and which Bond type is best to own based upon what your individual tax situation is next let's talk about dividends so the taxation of dividends depends depends on whether it's considered a qualified dividend or a non-qualified dividend if you have a qualified dividend then it is subject to those long-term capital gain tax rates that we looked at the beginning of the video so anywhere from 0% to 15% to 20% depending upon your actual taxable income now this is a great benefit because those income rates those income tax rates from 0 to 20% are a lot lower than the ordinary income tax rates which range from 10% to 37% so the more of our money we can have subject to long-term capital gain tax rates the better generally speaking all else being equal than it is to have those subject to ordinary income tax rates I say that because not every dividend is a qualified dividend only qualified dividends are subject to that tax bracket if it's a non-qualified dividend then that dividend is fully subject to ordinary income tax rates which are the ones are taxed between 10 to 37% at the federal level in order for a dividend to qualify as a qualified dividend you have to ad held it for 60 or more days during the 121 dat period before that stocks X dividend date can get a little confusing but essentially you have to own that stock for a certain period of time in order for the dividend that you're receiving from it to be qualified as a long-term capital gain in terms of the taxation of that dividend next let's talk about those actual capital gains so let's assume you own a stock or a bond or any type of investment that's hld outside of a retirement account if that investment increases in value and you then sell it that is considered a capital gain so what's the capital gain tax rate again it depends if it's a short-term capital gain so anything held for one year or less you are paying taxes at ordinary income rates 10 to 37% at the federal level if it is a long-term capital gain then you are now paying taxes anywhere between 0 and 20% so if you're holding that investment or if you have held that investment for over a year your tax bracket goes down when you ultimately realize that gain now this is where you need to be very careful about the types of mutual funds that you're owning outside of an IRA or Roth IRA I'm saying outside of those not because it doesn't matter inside of an IRA or Roth IRA it absolutely does for performance reasons but not for tax reasons if you're holding a mutual fund outside of a retirement account you might hold that fund for two years three years 5 years and not touch it but if internally within that fund the mutual fund manager is constantly turning over your portfolio buying and selling stocks buying and selling bonds buying and selling whatever security are owned in there and they're not holding those Securities for the 12 plus month holding period well they're not paying taxes on those short-term capital gains those are flowing through to you as the investor so be very mindful What's called the turnover within your mutual funds held outside of retirement accounts because even if you think you're being a good disciplined investor by holding something of them for over a year to qualify for long-term capital gain tax treatment well the internal turnover that's happening within the fund that gets passed along to you as the investor to ultimately pay the tax bill on so make sure that you're mindful of that when you're selecting the funds that you're going to invest in outside of retirement accounts next let's talk about Roth IRAs thankfully Roth IRA are one of the easy ones in general you're not paying any taxes if you're taking money out of a Roth IRA in retirement now this must be a qualified distribution from your Roth IRA I can go all the ins and outs of that but I did a podcast here that you can access this podcast will walk you through what qualifies as a qualified distribution from a Roth IRA but assuming you meet that definition of a qualified distribution that income is completely tax-free which is an amazing thing to have in your retirement next let's talk about Ira distribution so traditional IRA distributions which could also include traditional 401K distributions any money that you pull out of a traditional IRA or traditional 401K is fully subject to Federal ordinary income taxes now the money that's in your IRA or the money that's in your 401k even when you're retired that continues to grow tax defer so it's not the total balance you're paying taxes on it's just whatever amount you you pull out so if you have a million dollar in your IRA and you only pull out $10,000 you're only tax on $10,000 if you have a million in your IRA and you pull out a million dollars well you're tax on the full million doll so make sure you're being mindful of how much are you pulling out each year because one of the things you can do to decrease the taxes on your IRA is to implement a good Roth conversion strategy a good Roth conversion strategy allows you to control the timing of when you're actually pulling money out of the IRA and not just pulling money out to keep your cheing account but typically pulling it out to then convert to your IRA or your Roth IRA I should say where it then grows tax-free qualified charitable distributions are another great way to decrease the tax liability on any IRA distributions so I have other videos on this channel that you can go and look at where I walk through that in more detail but those can be excellent things that you can Implement to decrease a tax bill on your IRA distributions so that's all the federal level every state just like I said before has different types of ways that it will tax IRA distribtion tions some states fully include those distributions in your taxable income other states will exclude a portion of the distributions from your IRA from taxation some states will fully exclude that from taxation so depending upon what state you're in talk to your financial adviser talk to your accountant to see how will those distributions be taxed when you pull that from your portfolio next let's talk about rental income in retirement so you have a rental property you're collecting income there that income is subject to ordinary income tax rates at the federal level but only the net income so if you're renting out a property for $2,000 per month you're not paying taxes on that full $2,000 each month in federal ordinary income taxes what you do first is you deduct any of the expenses involved with that property so what could deductions look like for a rental property well this could be mortgage interest if you have a mortgage this could be property taxes that you're paying on the rental property this could be any basic operating expenses with the property this could be depreciation now depreciation is a big one because it's not actually a cash expense you're not actually paying someone depreciation and then writing that off depreciation is just writing off a certain portion of the building the building expense each year it's kind of like a phantom expense but it's saving you money in taxes now there is depreciation recapture if you later sell that property but depreciation allows you to deduct some expenses from the property that you're not actually out of pocket with when it comes to paying for them whatever is left after all that so if you rented out for $2,000 per month but then you have mortgage interest then you have property taxes then you have depreciation then you have all these other expenses associate with the property whatever is left that is what's subject to ordinary income taxes at the federal level so those are the big types of income that you're going to be paying taxes on the retirement now a couple things I'm going to include as an honorable mentioned they're not necessarily income taxes but they are taxes that you need to be aware of the first is what's called net investment income tax this is assessed on things like interest income div dividend income capital gain income you only potentially pay this income if your modified adjusted gross income is above $250,000 and you're married or it's above $200,000 in you're single the numbers for this are actually on the cheat sheet that I mentioned above but this is something to be mindful of so sometimes when you're thinking about taxes on things like rental income or dividends or capital gains yes look at federal taxes yes look at state taxes but you might also potentially be subject to net investment income taxes which an additional 3. 8% on some of that income and then the other thing to be mindful of is what are called Irma Sur charges so Irma Sur charges are the extra amounts you might potentially have to pay on any of your medicare premiums so when you retire and you have Medicare you pay a premium for Medicare Part B and Part D and there's the base level premium that everyone pays but once your income starts to exceed certain thresholds you may have Sur charges on those premiums those Sur charges are listed on the important numbers fact sheet that I mentioned above as well but something else to be mindful of not traditionally a tax or not thought of as a tax in a traditional way like other income sources are at the federal level and state level but it's something where the higher your income is the more you're going to be paying so in a way it is like a tax so these are all the different ways that you might be taxed on various income sources in retirement this can seem quite overwhelming so the next step isn't just to understand how are these different income types taxed but how do I start to think about where I should pull money from first in retirement based upon these different tax rates so if you're wondering that well I made this video here and what this video is going to walk you through is based upon the portfolio that you have and based upon your tax situation where should you begin to pull income from person retirement to ensure you're minimizing the tax bill that you owe once again I'm James canol founder root financial and if you're interested in seeing how we help our clients at root Financial get the most out of life with their money be sure to visit us at www.

root Financial partners.