Connecting the Income Statement, Balance Sheet, and Cash Flow Statement

33.29k views3478 WordsCopy TextShare

Long Term Mindset

▼FREE Accounting Infographic eBook:▼

📚 https://longtermmindset.co/fssebook

▼Shop Our Store: ▼

🛒 h...

Video Transcript:

Warren Buffett calls accounting the language of business and he noted that it's a vitally important skill for every investor and business person to learn yet the sad truth is that 95% of business people don't know how to read financial statements that's like being a professional musician but not knowing how to read music in this video I'll explain what the three financial statements are and show you line by line how they connect with each other if you watch this video to the end you'll literally know more about accounting than 95% of people in business hi my

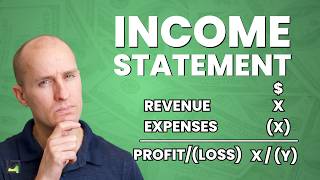

name is Brian Feroldi I'm a financial educator who's been analyzing businesses for more than 20 years now there are three major financial statements they're called the income statement balance sheet and cash flow statement each statement is designed to answer a specific question about a company's financial position to give readers a more complete view of its Financial Health so the income statement answers the question are you profitable it measures a company's revenue and expenses over a period of time to answer that question the top number of the income statement is a company's sales or Revenue During

the period from there we subtract a variety of expenses that the company takes on after we've subtracted those expenses we are left with either a profit or loss on the bottom line from there we divide that profit or loss by the total number of shares outstanding which gives us a profit or loss on a per share basis the second financial statement is called the balance sheet which answers the question what's your net worth the balance sheet lists all of a company's assets on one side which is everything it owns on the other side it lists

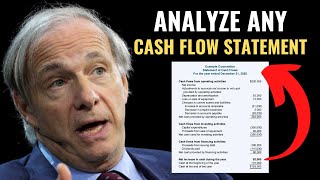

all the company's liabilities which is everything that owes to others and all of the equity in the business which called shareholders Equity the balance sheet is called the balance sheet because of the master accounting equation assets equals liabilities plus shareholders Equity this equation always perfectly balances hence the name of the sheet the third major financial statement is called the cash flow statement and it answers the question are you producing cash the cash flow statement is also measuring a company's cash inflows and outflows over a period of time similar to the income statement but the cash

FL statement only cares about the movement of cash in and out of the business and those cash movements are tracked in three General categories the first category is called operating activities this is all cash inflows and outflows related to operating the business the second is called investing activities these are cash inflows and outflows related to making investments in the business and the third is called financing activities this is cash inflows and outflows due to financing decisions related to the business now each of these financial statements stands on its own to answer that specific question about

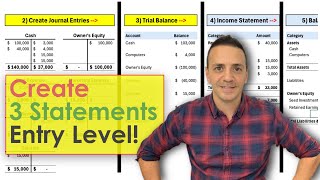

a company's financials however all three of these statements talk to and are connected to each other and it's by studying the connections between the financial statements that we can understand a company's financial position on a far deeper level now that we understand the basics let's take a look at the financial statements of a fake company called best coffee company to see how these three financial statements connect with each other here we have best coffee company's income statement on the Le hand side cash flow statement on the right hand side and balance bance sheet in the

middle notice that the income statement and cash flow statement are measured over a period of time January 1st through December 31st while the balance sheet is a point intime snapshot taken on the last day of the period December 31st 2023 so to understand how the financial statements connect with each other let's start by taking a look at how the income statement connects to the balance sheet to do so we're going to go line by line down the income statement and show you how each category affects the numbers on the balance sheet the first time to

look at would be Revenue which is the total sales generated During the period now revenue or sales can be accounted for or paid for in two different ways the first way would be if the customer makes a cash payment for those sales for example buying a cup of coffee for us and then paying in cash this would directly impact the balance sheet because it would make the cash balance that we have go up however a customer could also pay for that same coffee using credit in which case the business would not receive the cash immediately

we would record that transaction on the balance sheet under a category called accounts receivable and that transaction would cause the company's accounts receivable balance to increase the next line item on the income statement is called cost of goods sold this is all of the cost directly related to producing the cup of coffee that was sold and would include things like the beans the water and the paper products used to give the coffee to the customer now best coffee company could pay for those supplies in a few ways first it could make a cash payment to

the supplier for those supplies which would decrease the company's cash balance or it could use inventory that it already has on hand which would decrease the company's inventory balance or it could buy those supplies using credit in which case it would increase the company's accounts payable bound now the next number in the income statement is called gross profit which is simply Revenue Minus cost of goods sold this figure has no impact on the balance sheet so we'll move on to the next number the next category here is operating expenses which is a catch-all category for

all overhead expenses that a business takes on now there are multiple ways that a business could pay for its operating expenses as well if it paid for those operating expenses using cash that would immediately decrease the company's cash balance it could also pay those operating expenses on credit and it would do so by increasing the payables that it owed to others now those others could be employees of the company or suppliers that provide some of the overhead now one final category of operating expenses that could be paid is something called a noncash expense these are

real expenses that the business takes on but they don't result in an immediate I cash outflow to the business an example of a non-cash expense would be depreciation or the gradual writing down of the company's fixed assets this would directly impact the balance sheet because we would mark down or depreciate the value of the fixed assets on the balance sheet another non-cast charge would be amortization which is the writing down of the value of intangible assets just like with depreciation taking an operating expense charge of amortization would result in the gradual writing down of intangible

assets on the the balance sheet the final non-cash category is stock-based compensation this is when an employee is compensated with stock instead of cash now when stock-based compensation is paid to an employee it's marked as an operating expense on the income statement but it also impacts the balance sheet because it increases the additional paid in capital of a business and simultaneously decreases the amount of retained earnings that the business has that brings us to another profit metric called operating income which is simply gross profit minus those operating expenses the next line item is called nonoperating

expenses or income and this could impact the balance sheet in several ways first any interest generating assets that the company has such as cash marketable Securities and other long-term assets would generate interest income for the business this would be recorded directly on the income statement next any interest bearing liabilities that the companies has such as short or long-term debt would increase the company's interest expense that interest expense would be recorded on the income statement finally we could also generate nonoperating income if we sold an asset now those asset sales could include selling fixed assets intangible

assets or even selling off a part of the business whenever we would do an asset sale we would increase our cash balance but we would simultaneously decrease our long-term assets the next number in the income statement is simply pre-tax income which is operating income plus or minus any nonoperating expenses or income the next line item here would be taxes now there are multiple ways that a company can pay its tax bill the first way would be to pay directly with cash on hand which would lower its cash balance the second way would be to delay

the payment of those taxes which would increase our accounts payable total that brings us to the bottom line on the income statement which is called net income which is revenue minus all of the company's very expenses on the income statement now our net income total gets added to a company's retained earnings balance on the balance sheet retained earnings is the cumulative amount of profit that a company has generated over its lifetime as a business so we directly add the company's net income from that period to the company's retained earning total the next number on the

income statement is the total number of shares outstanding and then finally we have earnings per share which is simply net income divided by the total amount of shares that we have outstanding so there you go that is how the income statement directly impacts the balance sheet now let's move on to showing how the income statement directly impacts the cash flow statement to show this we're going to go line by line through the company's cash flow statement and show how each category could be impacted by the income statement now the first and most important way that

these two financial statements are connected is through net income the bottom line on the income statement net income is the top line on the cash flow statement so the cash flow statement starts with how much profit we generated during that period from there we need to make various adjustments based on whether cash came into the business or out of the business depending on that net income the first thing we need to account for is any non-cash charges that were recorded on the income statement remember on the income statement we recorded some non-cash charge expenses but

these did not result in an immediate outflow of cash so we have to account for that on the cash flow statement now the two categories that could include non-cash charges are the cost of goods sold on the income statement and the operating expenses on the income statement those non-cash charges could include things like the depreciation of fixed assets the amortization of intangible assets and stock-based compensation these non-cash charges would result in a positive impact to the company's cash flow statement since they did not result in a cash payment the next item here is to track

a company's changes in working capital now working capital just means things like accounts receivable accounts payable and inventory these categories do not impact the income statement they impact the balance sheet so we'll talk about those in the next section the next number here is cash flow from operating activities which is simply net income plus non-cash charges Plus or mindus to changes in working capital this is the amount of cash flow that a business produced from operating itself During the period from there we next need to account for Capital expenditures this would be cash outlay spent

on things like property plant and Equipment all of which are fixed tangible assets that a business uses to operate itself now those Capital expenditures are not expens immediately on the income statement rather since they have a long duration life to them the way that we expense them on the income statement would be through taking a depreciation charge during that specific period now that depreciation charge could be recorded in one of two places either in cost of goods sold if that equipment is used to make the product or service or as an operating expense if that

property plant equipment is used for General Corporate purposes the next line I'm going to hear would be any cash outlays for Acquisitions now making acquisition could actually impact every single part of the company's income statement because the acquired business income statement would get incorporated into our income statement the next line item here would be sale of an investment the sale of investment would be accounted for in nonoperating income if it resulted in an income to us and the final number here is cash flow from investing activities which is all the cash inflows and outflows related

to making investments in the business the next number here would be related to any changes in the company debt balance we could either borrow new money which would increase our debt balance or pay down debt that we already have which would reduce our debt balance now the amount of debt that we have directly impacts how much interest expense that we pay which would directly impact nonoperating expenses the next number here to track would be if the company issued or repurchased any stock if the company issued stock that would increase our shares outstanding and if it

repurchase stock that would decrease the shares that we have outstanding the next number here would be any dividend payments that were made those dividend payments would be made to each of the individual shareholders which is tracked on the income statement and that brings us to our next total which is total cash flow from financing activities from there we add up the net income cash flow from operating activities cash flow from investing activities and cash flow from financing activities and that gives us the total change in cash during that specific period we then take that change

in cash and add it to the cash at the start of the period which gives us the total cash at the end of the period so that's how the income statement relates to the company's cash flow statement that brings us to the final connection which is how the balance sheet connects to the cash flow statement here we have best coffee company's balance sheet and cash flow statement and to show you how these two statements connect I'm going to go line by line to the cash flow statement now we already talked about net income which is

the top number on the cash flow statement net income directly impacts the retained earnings that is on on a company's balance sheet next let's account for the company's non-cash charges if a company records a depreciation charge that would lower the fixed assets that the company keeps on the balance sheet if a company takes an amortization charge that would lower the total value of intangible assets that the company keeps on its balance sheet finally if a company takes stock-based compensation expense that would increase the amount of additional paid in capital that a company has and decrease

the amount of retained earnings that a company has the next category here is changes in working capital and there are multiple categories that can be affected on the company's balance sheet first would be the company's receivable balance during a period a company can either increase its receivable balance which would be bad for cash flow or decrease its receivable balance which would be good for cash flow it's a similar story for the company's inventory balance if a company's inventory level is increasing that results in a cash outflow and if a company's inventory level is decreasing that

result results in a cash inflow the next number here is in a company's account's payable and it's the opposite impact of receivables and inventory if a company's accounts payable balance is increasing that is good for cash flow and if a company's account's payable balance is decreasing that's bad for cash flow but then we take all of those changes together receivables inventory and payables which will have a severe impact on the direction of a company's cash production the next number here would be a company's Capital expenditures or spending on property plant equipment now there are multiple

ways that spending on Capital expenditures can impact the company's balance sheet if those Capital expenditures were paid for in cash that would decrease the company's cash balance if those Capital expenditures were paid for with the issuance of debt that would increase the company's debt balance finally those Capital expenditures would be added to the company's fixed asset balance which would increase the fixed asset that the company has on its balance sheet next let's talk about Acquisitions if a company pays for an acquisition in cash that that would decrease its cash balance if a company pays for

an acquisition by using debt that would increase its debt balance if a company pays for that acquisition with Equity that would directly impact the amount of equity issuance that a company has finally Acquisitions would also impact the company's Goodwill balance remember that Goodwill is the premium paid to acquire another business over the fair value of its tangible assets so making that acquisition would result in an increase in the company's Goodwill balance finally when one company acquires another the acquirer takes full control of the acquiree's balance sheet so that could literally impact every single category on

a company's balance sheet if it results in buying another business outright next category here would be sale of Investments generally speaking when a company sells an investment that results in a cash infusion so this would directly impact the company's cash balance at the same time the sale of an investment where a company divested one of its pre Acquisitions could result in the company decreasing its Goodwill balance moreover depending on the nature of the asset it could also decrease the company's long-term asset category related to the asset that was sold for Investments the next category here

would be changes in the company's debt if the company borrowed money that would result in an increase in the company's cash balance and a similar increase in the company's debt balance if the company repaid debt that it already had that would result in the decrease of the company's cash balance and a decrease in the company's debt balance too it's a similar story for the issuance or rep purchas M of stock if a company Issues new stock that generally results in an increase in the company's cash balance and an increase in additional paid in capital if

a company repurchases stock that results in a decrease in the company's cash balance and a decrease in the company's retained earnings the next number here would be dividend payments if a company pays a dividend to its investors that results in a decrease in its cash balance and a decrease in the company's retained earnings balance now as we've already talked about the cash flow statement tracks a changes in a company's cash balance from the start of a period to the end of the period we take that change in cash and we add it to the company's

cash balance at the start of the period which gives us the total cash balance at the end of the period which goes directly on the balance sheet to become the company's new cash balance now an important caveat to understand is that not all companies use these exact terms and layouts when they're making their own financial statements companies have a lot of leeway with the categories that they use to create their financial statements and even with what they call their financial statements to make this easier to understand I created a free ebook that has all of

the different names that you might see used on a company's financial statements if you want a free copy of that ebook simply visit LongTermMindset.co/fssebook or click the link in the video description well thanks so much for watching I hope that this this video was useful if so give it the thumbs up that really helps us out on YouTube if you want to keep learning accounting for free I highly recommend you watch this video next

Related Videos

13:33

Reading An Income Statement IS EASY When Y...

Long Term Mindset

11,232 views

16:19

How To Analyze a Balance Sheet

Daniel Pronk

651,391 views

11:21

EBITDA vs Net Income Vs Free Cash Flow Exp...

Long Term Mindset

640,512 views

1:19:24

Principles of the Balance Sheet. A mini cr...

The Financial Controller

91,883 views

2:20:59

accounting 101 basics, learning accounting...

selfLearn-en

12,437 views

![Build a 3-Statement Financial Model [Free Course]](https://img.youtube.com/vi/Rmi9fwkJjHw/mqdefault.jpg)

1:34:25

Build a 3-Statement Financial Model [Free ...

Wall Street Prep

261,792 views

1:19:07

Complete IFRS Consolidation Lecture: IFRS ...

Silvia of CPDbox

15,071 views

18:49

Free Cash Flow Explained

Long Term Mindset

28,385 views

10:01:51

Full Financial Accounting Course in One Vi...

Tony Bell

1,991,953 views

6:21

Balance Sheet Red Flags (4 Warnings Signs)

Long Term Mindset

76,250 views

22:45

How To Analyze a Cash Flow Statement

Daniel Pronk

348,054 views

9:58

The INCOME STATEMENT Explained Simply

Long Term Mindset

22,040 views

23:57

How to Build a 3-Statement Financial Model...

Josh Aharonoff (Your CFO Guy)

16,850 views

30:28

Financial Statements Explained | Balance S...

365 Financial Analyst

200,584 views

12:04

TOP 10 Ratios to Make You a Professional I...

Long Term Mindset

35,098 views

13:45

Learn 80% of Accounting in under 20 Minutes

The Financial Controller

14,676 views

9:55

The CASH FLOW STATEMENT: all the basics in...

Long Term Mindset

86,954 views

16:12

How to Analyze a Cash Flow Statement Like ...

Investor Center

745,501 views

1:24:37

3-Statement Model: 90-Minute Case Study fr...

Mergers & Inquisitions / Breaking Into Wall Street

217,016 views

8:35

Top 5 Income Statement Red Flags

Long Term Mindset

18,459 views