Market Outlook for Jan 12, 2025 - The Problem with Bonds

16.65k views11002 WordsCopy TextShare

Mark Meldrum

0:00 - 18:58 Duration

18:59 - 25:20 Beta

25:21 - 1:08:23 The Problem with Bonds

Instagram: https:...

Video Transcript:

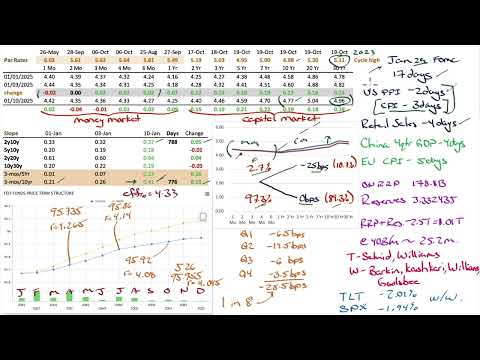

[Music] okay let's start with rates and yields like we always do and this is becoming a bigger and bigger story is what is going on with the long end of the curve uh and it's not just the US I'll show you uh a site in a minute and we can click on any country and any bond and we can get a nice chart up very quickly um of what's going on and we'll see that this is is more Global the bill is coming due for all of that pandemic spending when I say the bill is

coming due uh the bond market is looking at government saying okay you got to you got to rein it in now you you bought all of your growth uh and you have these deficits to GDP that that are just unsustainable we put up with it for a couple of years but enough is enough uh and the conversation uh uh this last week I don't I can't tell you how many times I've heard that the terms term premium thrown around when talking about bonds it's been the story all week long uh watched real yield term premium

watched a few podcasts term premium term premium so we'll we'll spend some time and we'll look at the premiums that are built in to the yield curve and where these premiums would be expected to show up and when they'd be expected to show up uh and it's not just the term premium uh that's that's causing this although the term premium has been has been rising it is it is uh you can't just look at the yield curve you have to look at the shape of the forward curve of 3mon rates in relation to the yield

curve and put them together so we'll look at a bunch of stuff have a look at uh at our data here uh from the one month out to the six month fairly well behaved but then after that uh the bare steepener continues this blue line is this week over last week we see we're up again uh and uh the further out you go the worse it is so the more duration you have the more pain you're feeling look at the slope of the 2 to the 10 increased by five basis points upward sloping by 37

but look at the 3mon to the 10-year the money market to Capital Market increased triple that amount 15 basis points uh now upward sloping 41 basis points by the way I'm going to show you an interesting trade on this one uh that uh that has very high return that hedge funds often do when you have upward sloping curves you usually don't have these upward sloping curves with elevated money market Market rates just to be very clear a bare steepener when I say these uh here are your money market rates over here all the way to

the one year this is Money Market there's Capital Market you have elevated money market rates it's very rare that you have an upward sloping curve um with elevated money market rates a bare steepener at these levels usually is indicative of uh stagflation meaning that you expect that inflation High you expect inflation to continue to be high that it's just going to it's going to just hang around for a while and usually it would put some kind of downward pressure on growth which would lower longer term yields because you'd expect a recession that's why I say

it's very rare to get a bare steepener at these elevated money market rates something is going on we got to figure it out my theory is well it's it's it's the tail end of all the the um deficits and if you look at growth uh again in the G7 uh you look at the level of nominal GDP growth and you look at the deficit to GDP they're almost equal that if governments had balanced their budgets for the last five six years you would have had zero growth in most advanced economies uh 41 41 basis points

uh on this started the year at 21 started the year at 21 I want you to think about that the year was only 11 days ago we're at 41 uh so that is it's the rapid moves uh I'll show you uh some other countries in a little bit let's just go through our data here uh January 29th fomc in 17 days this is post inauguration 9 days after inauguration does Trump have enough time to push them around or is Trump going to let them uh go uh on hold I don't know uh but right now

I think the probabilities are correct uh no change is almost a a certain thing uh up from uh 89% almost a certain thing and a 25 basis point cut call out a zero other than uh financial institutions using zq as a a hedging feature it'll never be exactly zero as a hedging feature it is in Ence zero I think that's the right move PPI we get in 2 days CPI we get in 3 days and I don't know why I keep saying this but it always seems to be true uh every report seems to be

the report to watch right so this is the big thing the jobs report was the big thing and man it came in it came in hot uh which basically cleared a whole basis point of rate cuts out of the uh uh federal funds Futures curve well we have CPI in three days look at where we are on the 30 year for example 496 the cycle high was 5.11 and we're at 4.96 right now uh we're 15 basis points away from that this could cement that if this comes in hot uh I would uh be looking

this is 2023 by the way when we look at the October highs on yields that's all the way back to 2023 I would be uh looking for the long end of the curve to take those out uh on the 30-year maybe the 10year 477 to 498 your 21 basis points away but I don't see it happening uh at the 2-year three or five 440 to 519 I can't see 79 basis points uh on the 2-year not at this point uh if you're going to have it it's going to be in the 10 to 30e range

uh but that's a big big risk event right there CPI what I think might be going on uh with uh some of the data that we've seen is uh some front running uh is uh bringing inventory into the country to get ahead of tariffs is consumers heading out to the stores and buying anything that they were going to buy before the tariffs uh which might uh uh eliminate any price cutting or any price decreases that otherwise would have happen because demand is robust but demand is not organically robust it's just being pulled forward to front

run the tariffs uh that uh perhaps what we want to see is uh after the fact uh we're not going to get that data for a couple of months but it could be that CPI for January the Jan AR read we get reflecting December is going to be hot more than likely going to be hot if in fact there is some front running going on uh so I don't know that I would look for Relief there retail sales in 4 days again that could come in robust if if my thinking is right that there is

some front running ahead of tariffs all of the purchases that might have happened in the first or second quarter being pulled forward well we may as well get it now we can avoid the tariffs it'll be 25% more expensive if we get it later you know so there might be some thinking there so I don't know that I would look for Relief here I'm not holding out a lot of Hope in fact I I think that after CPI is going to be a great buying opportunity on the long end because a a high probability that

we would we would see new highs that's that's sort of where I am I'll be pleasantly surprised if we get Get Low inflation if we do get a lower inflation read on top of what I still think is some front running if you can still pull that off then man do we have a deflationary backdrop China fourth quarter GDP in 4 days uh and EU CPI uh in 5 days the uh reverse repo uh 178 still uh not at its lowest the lowest was under 194 I think this will this will roll off very quickly

reserves back up they were under 3 trillion back 3.3 so uh the reverse repo reserves minus ample 1 trillion still sitting at 25 uh months to get to that level at 40 billion runoff although I think uh that by June July we will have uh a a serious discussion uh at the fomc about ending the treasury part of runoff But continuing the MBS part of runoff some feds speak this week and the calendar does fill up from the time I look at at who is already scheduled Tuesday Schmid and Williams Wednesday Barkin cash KY Williams

and gouby and last week nothing had a good week TLT down 2% week over week SPX down 1.94% week over week let's look at the FED funds Futures curve uh this is uh sort of what happened after the jobs report this is Friday uh the index value lowered significantly meaning the implied rates increased quite a bit uh q1 is showing uh 6 and a half basis points of cuts I think uh you know I think January is a zero for sure Q2 12 1/2 basis points Q3 6 Q4 3 and 1/2 you're down to 28

1/2 call that one cut in eight and since I think January is a shoe in for a zero it's really one cut out of the next seven only one is being priced in now I'm going to show you a little later on that if if the market expects that this is the level of money market rates it will adjust the Capital Market as if that were the base the term premium uh and the recession premium and the time value of money which is really what determines the shape of the curve those three things will will

start to reflect that that is the level of rates uh which means that you'll still get this going on which which will break things let me uh show you the rest of the world I'll just drag this onto the screen here and uh I'm at uh trading economics and here we we can cycle through a whole bunch of countries really quick this is the US uh 10-year note 4.76 n uh and this is just one year and you can see from September here when the FED started cutting interest rates look at this we went straight

up we were as low here as uh what is that 3.6 3.6 on the 10e and you're almost 4.80 basis points up while the FED funds uh Target came down 100 basis points so that's a 220 Point Divergence look at the UK same thing since about uh midt straight up 4.8 uh Japan even Japan's tenure look at that uh from about uh here is September over here you can see from September following it upwards uh as well uh here is Germany uh just more recently just through the month of December uh straight up Brazil Brazil

is ugly look at that uh straight up there Canada not so bad but uh you can see it still is following Germany from the beginning of December straight up we're down around uh 2 point what was that 2. uh 2.97 2.98 to 3.44 not as bad as the us but uh still quite a move up um but we are expecting the Bank of Canada is expected to continue uh cutting uh France look at that uh again following Germany as well since the beginning of December uh straight up China bucking the trend look at China on

their 10year straight down in fact it was uh uh the bond price was getting so high the pboc has stopped uh buying government bonds they were pretty much supporting it but China is facing the very real threat of De deflation uh which would give you a lower even a negative term premium if you have deflation in there because with deflation the value of your currency is increasing over time let's look at some 30 years and all we have to do is to scroll down here we have the whole curve we can look at the 30-year

there is the US 30-year flirting with 5% go to 5 years you got a double top there if you were a technician you're looking at a double top let's go to the UK and let's look at their 30-year this is ugly look at that 5.4 on the thir year go back five years there's your list trust moment right there that big runup uh in bond yields look at that that is above that point go 10 years Go 25 years 25 years uh and look how high that is 5.4 that break stuff uh UK is in

uh in Fairly bad shape Brazil uh look at their tenure uh they don't have anything further than that so we can see that this is not just a us thing this is this is almost a global thing uh that is happening uh I don't think that money is leaving bonds I think money is leaving duration how can you have that well I don't have to be in the 10 the 20 and the 30 I can be in uh bills uh not bills but uh notes so bills are money market Securities notes are 2 year three

year four year 5 year 7e bonds are uh your uh you know your 15 20 25 30y year teners so I think that fixed income managers are saying well I like the yield uh that I can get in the middle part of the curve and we'll just flip back to our screen here in the US you're getting 4.4 446 459 47 in the 2 to the 2 to the 7ear range I just don't want all the big duration that comes with the long end of the curve I don't want to take that risk when you

don't want that risk that's where you get the term premium the term premium is a compensation for undesirable moves in the yield and when you have very high yields usually you typically have an expectation of a lower term premium because you think well they can't go much higher so I'm not too worried about that risk you become more concerned about recession risk which is why this is very rare that at these elevated money market levels at the elevated and we'll call it the time value of money at elevated time value of money levels that you

would get an increasing term premium that creates the bare steepener uh quite rare okay I'm going to show you real yields here because we do have big breaking news on this one uh I've been leaving real yields Break Even rates and OAS sort of out of it and I thought I'd visit it once a month but probably worth watching on a weekly basis we have a new cycle high on the 30-year re yield 2. uh 2.6 happened on January 10th the previous was 2.55 2.6 we're already starting to see new cycle highs on the real

yields all of them elevated 2.08 222 234 252 upward sloping as well this uh the 20-year re yield looks ready to take out the previous high as well I don't know that you get there on the fiveyear you're a long ways away 2.08 to 2.59 51 basis points I don't know that that gets there for that to get there the long end of the curve would have to be uh really brutally high but we're already seeing it look at that inflation expectations all increasing in line as well uh corporate spreads nothing to see here and

look how tight they are look how tight they are high yield is a whole sitting under 300 basis points 282 investment grade as a whole sitting under 100 basis points 83 even Triple C 7.34 the cycle high on that was 12.89 going the other way still continuing to either stay low or go even lower um just to you know sort of put that in perspective there's no there's no concern about the credit spread but lots of concern about uh the term premium itself and about inflation expectations okay let's move over to Beta also not having

a good time uh the forward four quarter operating earnings 27292 I um I checked with SP Global not updated so I'm not sure what's going on uh with those guys but it's hit and miss so I think I'm just going to just leave them out of the the mix for now uh 27292 you had a closing SPX of 5827 so uh a moderation in the forward multiple 21.35% below the all-time high getting to a 10% correction level will put you at 54665 almost a full little over a full multiple down if you had a 10%

correction you'd be pushing down closer to about 20 times forward earnings uh with a bare steepener going on with a capital Market curve increasing and again most Consumer Debt is priced off the Capital Market not the money market that's going to begin to crush things and since this is a global phenomena not just restricted to the US that's going to really begin to hurt Global growth so would you pay 20 times forward earnings if the 10e were 5.25 if the 30-y year were 5.5 and you saw this globally would you would you be willing to

pay 20 times the forward earnings when you could just grab those yields right so this is this is sort of the the question uh uh to ask if you uh took the inverse of the forward multiple and looked at it in terms of a yield you are at this point in time facing a negative equity risk premium in other words that you you are agreeing to a lower earnings yield to be in equities than to be in government bonds it's sort of perverse uh iwm 21683 uh had a very bad week uh they are now

in correction territory the most recent High you have to take the uh the correction from the most recent High not the all-time high the most recent high was 24199 on November 29th and down 10.4 I Jr uh same thing uh 12673 on November 26th they're down 10.8 small cap in correction large cap halfway a little less than halfway to correction territory 54665 uh implied volatility showing back up in uh S&P and if we look at the open interest 2.63 big jump in open interest on the put call ratio 2.63 puts for every call up from

2.16 almost unchanged on TLT in terms of put call ratio implied volatility 15.7 uh on equities now greater than TLT sort of makes sense given the level of overvalued well I say overvalued the level of valuation we can argue if that's overvalued or not but more volatility there than in bonds at this point the biggest threat to the equity Market is higher capital Capital Market yields if you continue with the bare steepener I can't see how how this Market can rally in the face of higher long-term yields at the same time because that is the

discount factor for future cash flows but it's also competition uh for money if you were rebalancing you would say equities uh 2.35 versus really cheap bonds let me reallocate to some bonds let me grab some of this duration nobody wants um both agre LS G and sector spider are in agreement next week both have uh 20 companies reporting and the same 20 companies I am impressed I mean it's it's 20 that's a big number to both be correct on uh the week after gets bigger the week after that is the big week so next week

is inauguration week still with some banks and uh a couple of tech I think Netflix is next week and there's two tech companies next week but it's mostly the Trail end of the banks and the regional Banks the week after is a big week with a lot of tech uh reporting uh what is coming up uh this week with the 20 that are reporting 33.1% of the weight in XLF reports uh this week a third of the XLF uh reports uh this week so my uh my deeper thought here on uh SPX is uh I

I I can't see it rallying uh in the face of these yields if I had to place one bet uh newer highs or a 10% correction I think I would be betting that we' probably touch the 10% first uh and uh I think uh small caps would have a very difficult time rallying uh as well I am uh short iwm and I have covered some because uh that is a a sort of a nice uh a nice Retreat you're in correction mode no point in getting greedy I'm not looking for a bare Market here uh

just a correction but if this corrects down to uh 546 you can expect iwm might see I don't know 20 200 to 205 um but I have covered some of my short position because the large caps have shown almost an unwillingness uh to commit to a correction uh but we'll we'll see with CPI this week if there's going to be a correction it'll be on that CPI report that CPI report comes in hot you're going to get new alltime or cycle highs I shouldn't say alltime but cycle highs on uh the on some Capital Market

yields and I think you'll be well on your way uh to a 10% correction on the S&P what I'm uh going to do here over uh the balance of this video is we're going to take a lot of the concepts that we we've seen in the CFA curriculum uh at uh all three levels uh whether it be in fixed income or economics and we're going to apply it to this problem um so you're going to get a taste if you don't have a subscription to the applied level you're going to get a taste of what

the applied level uh really is trying to do is is taking uh things that you would learn in the textbook and saying okay how do we actually apply this stuff in the real world how does it actually how does it actually work so if you are a uh CFA candidate and now is a nice time to bring this up because we do have results uh coming in this week from the November exam uh if you are a CFA candidate moving to the next level uh and you're getting your subscription on Mark mm.com consider the CFA

Plus subscription because you do get the applied level with it and often times when we learn something abstract it doesn't make a lot of sense to us but when we actually see it applied oh that's how that works suddenly the abstract becomes much more uh much more useful for you uh you get a better understanding of what the textbook is saying when you see it in the real world you also get a better understanding of the limitations of some of the stuff that you see in the textbook When You See It applied in the real

world let's see if we can make sense of uh the rise in long-term yields by breaking uh the components of yield down to three uh three broad components number one is just pure time value of money everything else will stick in the term premium uh that could be higher inflation expectations the increase in Supply on Treasury all of that will just call the term premium uh and then we have a recession premium a recession premium think of uh think of a bond as like a that has an embedded put that you're going to pay for

that is the recession premium uh for those of you who are recent or new uh to the Market Outlook uh you'll notice that this is what I do I write on screens uh I don't I don't have a high production video of me talking with a background with a whole bunch of b-roll over it I don't try to bring a lot of entertainment into it it really is just about you know trying to uh um create as many informed uh participants as possible so if this feels you know like a classroom let's basically what it

is I was a professor for much of my professional life so if it feels like a classroom uh it's because what that's what it is really so feel free to take notes uh there won't be any quiz or exam on this but uh real life will be your exam so let's break this down uh for time value of money uh obviously we're not going to lend money and just get our money back we want to be paid for that uh money has a time value we're going to proxy that with the 3mon T bill and

the forward curve why would we not just use spot rates why would we not say well we can use a three-month spot rate a six-month spot rate a one-year spot rate wouldn't the one-year spot rate be the time value of money for one year well the spot rate is derived from the par curve uh which means if the par curve has within it a term premium what will get imported into all the spot rates is some of that term premium and some of that recession premium will get imported into the spot rate so the cleanest

time value of money rate to use well the cleanest one would be an overnight rate would be one day Sofer but we're not going to use that we'll proxy it with the 3-month T Bill and then we'll just look at the shape of the forward curve to determine whether or not money is getting more expensive or less expensive who sets the price of money the Federal Reserve that is the target rate and it tries to uh Target uh interest rates especially money market rates to be within that primarily the 3-month T Bill we should expect

to be fairly close to whatever the effective federal funds rate is then we'll look at the shape of the forward curve this is Market determined uh and also influenced very heavily by Guidance uh from the fomc when we lend money we get paid for the time value of our money and if there were no other premiums involved we would we would basically see that every tenor uh would be equal to a three-month T Bill rolled over again and again and again and again and again at whatever the forward curve looks like so let's just be

nice and clean on the time value of money there we go for the term premium this is compensation for interest rate risk if I say well I'm going to take a I'll take a 10-year Bond however a 10-year bond has interest rate sensitivity that price could change on me a 3-month t bill has almost no duration meaning it has no interest rate sensitivity almost no interest rate sensitivity so if interest rates change quite a bit we shouldn't expect to see that t- bill budge very much in fact we buy T bills at a discount they

mature uh at par we should see almost every day a steady walk upwards on that t-u but a 10-year bond uh what if I need my money in 3 months uh I'm taking on price risk to take on price risk I have to be compensated for that that's why it's called a term premium because I'm going for a longer term I should be compensated for the risk that interest rates may change but specifically it's not the risk that interest rates may change specifically its yields may change in an undesirable way in other words I need

to be compensated for interest rates increasing this is important because if we think about uh return let's say here is yield right if yields are dropping uh that is reward if yields are increasing that is risk I don't need uh a premium for reward for reward I'm willing to pay a premium uh I I don't need to receive a premium for uh for that I need uh the risk premium uh to be up here I need my term premium to compensate me for the risk that rates go higher typically when money market uh interest rates

are very low there is a higher risk that yields will increase so the term premium tends to be very high at very low levels of money market rates and very low at very high levels of money market rates it's typically inversely related to the effective federal funds rate I will show you some chart on Fred that prove that that is true you typically have a high term premium when the effective federal funds rate is low because when it's low it's like well it probably can't go lower and when the effective fund effect of federal fund

rate is high you probably say Well it probably can't go any higher it's more likely to go lower right so there's this inverse relationship which is why again at elevated money market rates getting a bare steepener is very very rare it's odd that you would get an increasing term premium at high levels of the effective federal funds rate then there's also a recession premium this is something you're going to pay for you pay for it by accepting a lower yield uh us treasuries are a good hedge against Bad economic outcomes what does that mean it

means if the economy tanks treasuries are a great place to be because the Federal Reserve are going to cut rates very quickly and you'll get a beautiful return out of that Bond because it has duration so it's a good hedge against Bad Economic Times the higher the probability of recession the more willing you are to pay a premium uh for the uh for the put the basic uh put which is what we'll call the recession premium greater expectation of recession you pay more for the risk premium that means you willing to accept lower yields so

let's add the three together you have a high 3-month rate at 4 .33 if we look at the uh for the term premium uh here we can look at the level of the forward curve to determine what the term premium would be you have a if you have a flat or upward sloping uh forward curve you would have a rising term premium so if your forward curve look like this and then it starts looking like this and looking like this that will cause the term premium to increase uh so you we that has been going

on so we have Rising basis points so you have your time value of money you have your term premium but you would subtract some yield uh for the probability of recession however nobody sees a recession anymore probability of recession is dropping so I'm not willing to pay a lot for that premium so how it looks is like this you have your time value of money you have your uh term premium and then you would go backwards like this for the recession premium well now we're not so the uh amount that's built in for the recession

premium is very very low so it's the rising term premium and the shrinking recession premium that's really causing uh yields to increase on the long end of the curve all right let's uh look at some stylized charts here and then we will go to Fred and look at what actually happened to see if it matches uh this uh sort of framework I'm laying out here let's start with a low level of the effective federal funds rate you will have very low money market rates typically this happens after an economic shock after a recession fed lowers

rates dramatically the curve steepens a lot but it steepens from a low level of money market rates what you end up getting is an elevated 10year to 2year slope you can also look at the uh 10year to three month slope not just the 10e to 2year but you the 10 year to 3 month is another proxy of the level of term premium by looking at the level of the slope uh you have very high term premium because the risk of an increase in yields is greater uh than a decrease in yields because money market rates

are already very low uh you would have to have something going on at the longer end of the curve let's say quantitative easing where the uh Federal Reserve is buying these to start to begin to lower the term premium by pushing uh yields uh down by pushing the price up but with uh very low rates uh in in in the money market the expectation is that is going to cause future inflation thereby building up the term premium because uh the risk of rates increasing from here is higher than the the risk of them lowering because

they're already so very low your forward curve would be upward sloping like this uh what is this saying this is the forward curve of the 3 Monon by the way so it's saying well the 3mon is here the the front month would be here and then as you keep going out we expect the 3 Monon rate to increase over time as monetary policy normalizes after the recession so you have a recession rates drop all the way down and the market anticipates that well they'll normalize as the economy uh begins to improve here's your time value

of money uh so you would be looking at the current 3mon and then you You' just daisy chain multiply all of the forward rates and anything uh you know out to 2 years 3 years four years anything different than that we're all just going to dump it into the term premium but your term premium would be elevated um let's look at uh uh for uh the recession premium would be very very low because you are either in a recession now or just exiting so you'd have a very low level of money market rate you'd have

a elevated turn premium but almost no uh uh reduction in yield because of the recession premium thereby giving you a very steep uh yield curve Let's uh go to uh a top of the business cycle late expansion inflation pressure has built up and now we're just talking about demand induced inflation here so you have very high levels of the effective federal funds rate typically you'll get an inverted curve uh and a very low term premium at high levels because the risk of yields increasing from these already high levels are very low the belief is that

these rates will slow economic growth which will slow inflation so it's more likely going forward that yields will drop not increase hence the term premium begins to shrink because I'm less concerned about buy about the insurance of risk of yields increasing and I'm more concerned about the rewards of yields decreasing there'll also be a high recession premium because that is expected at higher rates remember last couple of years we had elevated money market rates and uh we were looking at um uh analysts projections of the probability of a recession they were elevated that means the

risk premium is elevated so you have very high money market rates but you have a very low term premium but a very high recession premium and that would lead to if this is your money market rate there's your 3mon and a very high recession premium there's your 10e notice you have an inversion of the curve 3 month to 10 year and we had an inversion for a long period of time because we had we had a downward sloping forward curve because that was considered the path so you have the time value of money decreasing you

had very low term premium because it was more likely that yields were going to decrease and a very high recession premium because that was likely that creates your downward sloping curve this is very typical with very low money market rates we should see an upward sloping forward curve with very high money market rates we should see a downward sloping forward curve with an upward sloping curve we would have a high term premium and a low low recession premium with a downward sloping curve we would have a very low term premium and a very high recession

premium uh well what do we have right now we have high money market rates but we have a high term premium and a low recession premium kind of doesn't make any sense if rates are if money market rates are high we would expect that uh to slow down economic growth we would expect a higher probability of recession uh and we would expect uh a uh lower term premium because we would think that yields would be headed downwards but we're getting this in this scenario okay let's look at some actual evidence to see if anything I

said on the previous screen actually works out in the real world because of it doesn't well then all that was was academic gymnastics uh and it wasn't very useful I have two panels here let's uh focus on the top one this uh in blue that is the 10year constant maturity minus the 2-year constant maturity in other words it's the 10-year par minus the 2-year par and so it's measuring the slope of uh the the yield curve from the 2 to the 10 uh you can do the same thing uh the 10 to the 3 month

and I'll show you in a minute it it gives you the same relationship so you have very high levels of the effective federal funds rate here here and you have an inverted yield curve as the rates drop the yield curve steepens as rates increase when I say rates I mean the the the effec of uh the the funds rate uh look what happens to slope it decreases so you have this inverse relationship all the way through uh increasing decreasing increasing decreasing decreasing increasing um and if you think about the slope as uh having a heavy

component being the term premium we are seeing an inverse relationship the higher the level of the funds rate uh the lower the slope the lower the term premium would be let's have a look at what the 3month uh would look like and I've got that on the screen uh so the blue line here as you see at the top is the 10-year constant maturity minus the 3mon you're seeing the same relationships look at uh here you have rates that are coming down you have a curve that is steepening you have uh the funds federal funds

rate going up look at uh the curve uh decreasing it's hard to point at this screen without this thing happening but just eyeball it and everywhere you see the red line increase you see the Blue Line decrease so there is there's some good solid evidence uh that uh wrapped up in that slope is is the term premium that we're seeing that as the uh fomc as the Central Bank ra raises interest rates it squeezes out the term premium because the higher interest rates go the more you the more the bond market begins to say wow

the risk of higher rates gets lower the higher the higher rates go so I'm more concerned about the reward from being in duration when interest rates are high than the risk of being in duration let's go back to uh our uh chart here so there we go there is good evidence of that inverse relation ship let's look at the term premium now and you can't because the term premium is dependent upon or at least uh largely determined by the level of the effective federal funds rate you cannot just look at the term premium you have

to look at it in relation to the effective federal funds rate in other words you need to normalize it if you just looked at the term premium uh it would be difficult to interpret uh because it wouldn't because it's a Time series but it wouldn't have stationarity this is a a a technical term uh uh in in Time series that to to evaluate to have some kind of information in a series some kind of tradable information we must have stationerity so uh what I've done to get stationerity is I've normalized it by dividing it by

the effective federal funds rate so this is the term premium on a 10year zero coupon bond which is the purest form of term premium uh because there are no coupon payments in there a bond with coupon payments coupon payments and then your final payment which is your principal and interest you can conceive of that as a portfolio of bonds a whole bunch of tiny little bonds and then one larger Bond well each of these tiny little bonds will have some kind of term premium in there so when we're looking at the whole thing as a

whole it's sort of the weighted the weighted average of all of the little term premiums in there let's just be clean and use a 10year zero and we'll divide that by the effective federal funds rate so you have a numerator and you have a denominator and here's what we should expect to see if we have an inverse relationship that as uh we raise the funds rate the denominator would increase because that is the effective federal funds rate it should increase uh the term premium if we're right should decrease in other words this ratio should tend

towards zero as interest rates increase so here is a zero here is zero here is zero rates increasing rates increasing rates increasing aha we do we do observe that relationship that at high levels of the effective federal funds rate we should see a low term premium and as the uh uh Central Bank Cuts rates it should reintroduce the term premium because at low levels of money market rates we should see a uh a upward sloping yield curve a steep upward sloping yield curve usually the steepest yield curves come at the bottom of recessions when rates

are very low that's what we should see look at that right rates are held low over this period of time look what happen over this period of time you have term premium you have slope uh you have some negative term premium in here but you had the uh Greek debt crisis that sort of went away for a while then you had the bond temper tantrum there is that temper tantrum there uh where you had a bare steepener going on uh so turn premium building into here because the thinking during this period of time uh was

that rates were going to have to rise at some some point you got to start raising rates so the market said well that's exactly what I don't want if I'm buying bonds I want to be protected from that so I need a premium call the term premium to protect me from the downside of rising yields uh and then that just didn't show up you did uh uh at this time so it sort of went away and then you did have the rising yields so your denominator increasing term premium decreasing Flatline Flatline there you go so

we've got that relationship down we have enough empirical evidence to suggest that the framework that we're thinking about is a useful framework at very high levels of the effective federal funds rate we should expect to see a low term premium but that is not what we're seeing we're seeing a high term premium which is very odd and if you have uh high levels of the effect of federal funds rate and a high term premium which means the market is more concerned about Rising yields than lowering yields it should also be concerned about the rising probability

of a recession but it's just the opposite there's the conundrum there's the problem on the long end of the curve is one of those two things are wrong and they're going to have to uh uh uh resolve themselves either the probability of recession is much higher than what we think it is if yields are going to continue to increase which means we should be paying more for the put which would mean lower yields or no there is going to be uh no recession uh but yields aren't really going to go much higher than where they

are now they may not change from where they are but they may not go any higher which means we would revert back to a lower term premium which means lower yields it would be difficult to say we need a higher term premium from these higher money Market rates with no chance of a recession you see where I'm going with that okay I'm going to introduce you to another reason why a term premium really really doesn't get too far out of hand uh it introduces a yield curve carry trade so right now uh we have a

10year at 4.77 we have a 1 Monon repo rate at 4.25 so from a money market perspective the reverse repo rate or the ver reverse repo income is 4.25 477 to 425 that opens up a carry trade uh so what you will begin to see more of is um hedge funds uh buying 10-year uh 10-year par Bonds in other words on the run so whenever there's an issuance it'll probably be well Bid And if we look at the the issuance the treasury issuance this last week they were all really well bid in fact even across

the globe uh I was uh uh listening uh to real yield and they were going through Market over Market uh talking about how well bid every single Market was at these high yields they're really well bid well these are going to be uh in demand uh any new issuant are going to be in demand reason is is because you're going to get a par Bond you get the coupon 4.77 it is the coupon that matters to get this done because your funding costs have to be paid for you want the coupon you don't want you

don't want your yield to be made up of a low coupon and potential uh pull to par you want it to be made up of the coupon Go finance that in the repo Market which is a reverse repo for money market funds uh 4.25 and let's just assume a 3% haircut uh which means you're going to be putting in 30 bucks to get that Bond you're going to buy it for 1,000 then Finance it for 970 your haircut 30 uh 30 bucks you're spread over a year you're going to get 4770 on your coupon minus

4250 on your financing you get $520 off a $30 investment 17.33% on that carry trade uh using uh using the repo Market uh plus any change in yield uh this is what starts to make this trade a little bit more exciting bessent wants to shift rollovers from money market to Capital Market this is going to create a lower supply of money market Securities so money market funds will be looking uh to create 30-day uh uh 30-day money market funds by using secured repos like this so you package a tenure uh into a repo uh the

money market fund is still getting a 30 a 30-day money market security because it's a 30-day repo but they don't need a money market security to get that done if you shift some of your uh rollover from the money market to the the Capital Market you do create a lower supply of money market Securities and bessent has been critical of yelling for uh uh uh issuing way too much in the T Bill market and not enough in notes uh and bonds uh the higher the yield on the 10e uh if the 10e starts heading up

towards 5% the higher the yield on the 10e the more attractive the trade becomes uh plus the probability of recession increases at higher levels and the probability recession is what you would pay for on it so it once you start pushing up to 5% on the 10-year the probability of recession has to start to increase so it's difficult to see how you can get much higher than the 10year for any longer period of time the term premium should shrink out at higher levels it shouldn't keep increasing it should shrink out meaning that it at that

at some point the term premium would start to turn against it and the recession premium would start to build up which means you start to get lower yields on the 10-year well the change in yields would be positive but you've already bought this bond that is going to continue to pay you 4.77 and if the probability of recession increase and you get a recession what happens to your funding costs they drop on the way down right the term premium if we uh zoom in on the charts that we had the term premium as a percent

of the effective federal funds rate or controlled for the effective fed federal funds rate uh is is got a range this is the zero range this is a plus2 minus point2 it tends to range within in in this area here currently it's near the upper range of 0 2 uh and the uh recession premium is very low and that's why you have this high level uh uh this this this increasing level over here because we've pushed up to the upper bound over here so if the term premium continues to increase up we go and if

the belief is that no recession there is no recession in sight the economy is strong the recession premium can even turn negative because you could say there's no upside to bonds here there's more upside to equity but higher yields do give competition to the market how this resolves itself uh is is going to be interesting to see my suspicion is that this can't hold is that this is an overreaction so on the next screen I'll uh lay out some arguments for what would cause it to go higher what would cause it to go lower so

from here uh what would cause us to get higher yields the big one I see is momentum is everyone's talking about higher yields and everyone's talking about I shouldn't say everyone but the conversation The Narrative is getting louder and louder oh it's a five 5% tenure we're going to see a 5% tenure so that it's almost it's almost being stated like a fact well we're going to get there it's going to be 5% we're going there that's momentum you get this momentum in there uh sometimes you get trades that don't even think about it anymore

they just look and say we're not at 5% sell the 10 you're short to 10 year we're not a 5% yet so you have that momentum that is hard to change uh you have inflation expectations that are also fueling that momentum uh we are seeing robust growth you had uh a very good jobs report uh the idea of deportations and lower immigration uh will create uh wage inflation uh and you have tariffs that are coming uh which will create inflation even though it is a one-time hit to inflation because it's not ongoing it's not inflationary

it raises the price level once and that's it so that means it's not inflationary but you could have some front r running going on of that now creating the illusion that there's inflation as opposed to uh uh it being nothing more than urgency right increased treasury Supply is the thinking that you have a lot of role over coming next year and much of that will be moved out of the money market into the Capital Market you'll have an increased supply of Capital Market Securities uh coming online uh Fede hasn't been very helpful we're in no

rush we're on hold um a couple saying oh I still see uh lower rates uh going into 2025 and some have said I don't see any or we're in no rush we're on hold uh plus we know they have a reaction function that is data driven so we're going to be data point to data point and February and March data which is after Trump takes office and we start to see that okay maybe it's not going to be across the board tariffs and maybe it's a little bit slower on the deportation and not much has

changed on immigrations or H1B visas okay so maybe that was all just rhetoric talk uh and uh but we're not going to see the uh February data and the March data till March and April so we've got some time before we see that so if there is some front running going on if there is concern about well what would we expect we're not really going to see it in the data till later in the first quarter beginning of the second quarter that you know if we thought about well in the near term where are yields

going to go probably higher uh inauguration isn't for another week so we have a whole week of uncertainty ahead of us and I don't I don't expect Trump to calm down the markets uh I do I do have a suspicion uh that he is more than happy to see markets sell off before he takes office because it's easier to get markets uh to accelerate from a low lower level and he can blame all of that on Biden and take all the credit for the recovery um I don't see him being a calming Force until he

can take full credit for it so if I had to bet for this week being blind and not not being able to see till next Sunday I would probably uh bet it all on higher yields during the week so for duration I expect the if you're holding duration there'll be some pain but if you're looking to add duration I think this will be the week this will be a great week uh for duration CPI will tell us a lot but CPI will tell us a lot about December uh which I think has some front running

going on it because if you tell me that the stuff that I buy that's coming from outside the country is going to go up in price by 25% on day one across the board or 60% on day one because it's coming from China and there's stuff I want I'm going to buy it now I'm going to front run uh which I as a retailer would say the robust demand the stuff is flying off the shells I don't need to discount it in fact I could probably raise my price right now that you might see some

of that inflationary pressure so January is not going to tell us anything about the future but it's going to tell us a lot about how people reacted in response to the potential of this going on yeah I think it could be a brutally ugly week uh this week which I think again I have a suspicion that that would only serve Trump's Purpose By him saying ah okay good I take over at these low rates so now the narrative is as as Biden was leaving he was destroying the world look what he did he was sending

money to Ukraine California was burning he destroyed the market he destroyed the bond market and I saved it all what a story um lower yields uh I think we have to wait until after inauguration day before we really start to see uh an attack on momentum here a shifting narrative a spending cuts begin to drip out and they will uh uh the EV credits they'll be gone Ukraine support will quickly fall to zero there'll be a bunch of program Cuts announced uh it's not just going to be one big announcement on day one it'll be

drip drip drip drip drip this is cut this is cut that's cut this is gone that's gone executive order after executive order that may begin to change the narrative on the momentum saying okay we are they are reigning it in they are serious about it they are getting stuff done right you don't have to say oh all we found was 400 billion all you have to do on day one is say 20 billion cut here 12 billion cut there next day 13 billion cut there next day five billion cut here next day 12 billion here

and it's this drip drip drip drip drip that will give the impression that a lot is going on that uh that that could change that momentum story continued progress on inflation because I do I do see uh uh that as the backdrop any increase in inflation I think is is caused by some kind of Supply disruption uh or some kind of state of urgency like front running ahead of tariffs or front running ahead of a Port strike remember December you had the looming issue of the Port strike the East Coast Port strike ahead of you

as well well that has been resolved but that that was not the case in December so when we get the CPI and the PPI it will reflect December it will reflect consumers concerns about the tariffs and it will reflect importers concerns about the Port strike because negotiations were starting again at the beginning of January that's all solved now but that's not going to be in December number will the markets uh uh if we get a hot read Will the Market say yeah but let's keep in mind that this psychology in December was in place and

and one of those issues is resolved now uh but I do see continued progress on inflation but then again uh that data won't be available until March or April uh technology will continue to progress productivity is fairly High uh I think you're going to have limited and or targeted tariffs uh and uh you'll probably get retaliation now if you get retaliation you're T you're not going to be so willing to do across theboard tariffs retaliation uh keeps Supply in the US that otherwise would have been exported so that then uh increases the supply of certain

things in the US because they they uh um with retaliatory tariffs uh the importers other countries uh will lower their demand that will create a glut of those things in the US and lower those prices because inflation is not just certain things it's a whole basket of goods and the stuff that they export is in there as well slower progress on deportations uh you're not going to deport 11 million people on day one that's not going to happen uh without any increase in spending you're not going to increase the pace at which you Deport but

you will start to do it and I think it'll be a slow drip drip drip of all the successes they've done we've deported this many people five more buses are leaving three plane loads are leaving but I think it'll be slower uh slower progress on deportations than than uh than hollowing out the workforce of 11 million people really quickly uh the FED I think is going to end US Treasury runoff uh uh because it's it's running off by uh 25 billion a month the reinvesting uh only uh 15 uh or sorry they're reinvesting they're running

off 15 reinvesting 25 I think by June or July that will that will end and they'll start to um that will add demand uh on the long end of the curve uh and the carry trade is attractive uh right now the carry trade that I just laid out it is attractive uh and I think uh as the 10year gets closer to 5% it'll become more and more compelling uh that it's a great carry trade to be in because if you consider 5% tenure uh 30% haircut uh let's go with uh not 30% sorry three let's

even go with 4% haircut so you're putting out uh 40 you got 75 basis points uh in there so you're making 750 on the 40 uh per year $7.50 on every 40 plus any change in yield well at 5% a 10year would have a duration of about 8 8.2 at high interest rates at at yeah at at at four at 5% it probably have call it around eight uh which means you'd have an 8% change in price for 100 basis points which means if it goes to to six the bond would drop from 1,000 uh

to uh 9 if it had duration of eight would drop to 9 920 so you you you can still uh Finance quite a bit of that 920 if you have a uh even as much as a 4% haircut so the the collateral the extra collateral you'll have to point isn't uh isn't that brutal as if you were doing it if the 10year were let's say 1.6% with a uh 25 basis point uh money market rate uh or uh repo rate that's a little bit more dangerous for any change in in yield but at 5% are

you going to get to six probably not so the closer you get to five the more attractive and the less risky uh this trade the less risk I say the risk the trade is all in here right the less risky this trade becomes uh which means that the market can probably absorb a lot of issuance uh without yields necessarily Rising because you introduce this carry trade so all in all I do expect this to dominate for uh uh the next week or two and then once you start seeing the uh executive orders coming out I

think you'll start to shift towards this which means uh for adding duration if you have no duration I think the next couple of weeks will present a great opportunity to add duration if you already have duration next couple of weeks will be will be un comfortable but if you take a longer term view uh all of this will pass if you take a longer term view because I think we're in a period or in an area where it doesn't make any sense high levels of the effective federal funds rate along with a high term premium

but no recession premium something doesn't make sense there something isn't quite right and if you have an event like this which is extremely rare then the event can't hold because if it does hold if the market is right then the recession premium is significantly higher something will break which will cause the FED to lower rates dramatically I can't see how you lose on duration uh given given what's going on right now but I can't see how you win on duration in the next week if you if you want to balance that anyways uh there we

go [Music]

Related Videos

55:41

2025 Economic Outlook with Mohamed El-Erian

Walker & Dunlop

312,653 views

42:07

Have We Narrowly Avoided A Recession? | IT...

ARK Invest

43,404 views

21:25

Crypto Currency Fallacies Part 1 - Long L...

Mark Meldrum

21,935 views

26:20

Larry Williams 2025 Market Outlook: The Go...

StockCharts TV

149,833 views

4:41

DeSantis Interrupts Reporter He Says Is Co...

Forbes Breaking News

216,789 views

8:31

What is Going on with the US Treasury Market?

Capital.com

62,754 views

43:10

Crypto Fallacies Part 2 - If bitcoin were ...

Mark Meldrum

11,805 views

41:32

Microstrategy's real game is gamma not delta

Mark Meldrum

42,972 views

38:05

The Seven Pillars of Market Bubbles

The Compound

5,354 views

10:02

This Winter Pattern Will Be VERY Different...

Ryan Hall, Y'all

795,297 views

5:21

'Fast Money' traders talk tech sliding and...

CNBC Television

6,707 views

56:01

Howard Marks’ Most Iconic Interview Ever (...

Investor Center

32,336 views

4:17

Stallone's brother goes off on 'inept' lea...

Fox Business

217,487 views

14:05

Economist Paul Krugman on Trump Tariffs, I...

Bloomberg Television

140,289 views

38:11

‘The End Is Close’ For Markets; 25% Crash ...

David Lin

191,180 views

35:28

On Bubble Watch

Oaktree Capital

63,182 views

15:04

Nissan Is Fighting To Survive But Its Futu...

CNBC

271,642 views

14:38

What Is The Yield Curve & Why It’s Important?

PensionCraft

53,272 views

13:32

Goldman Sachs Reveals 2025 Investment Play...

Bloomberg Television

66,468 views

LIVE FIRE UPDATES: California wildfires in LA

FOX 11 Los Angeles