The WORST Retirement Lies Told By Finance Gurus

83.07k views3990 WordsCopy TextShare

Retire with Julia, CFP®

Take control of your retirement → https://www.ursadvisory.com/retirement-roadmap

Join our Email Lis...

Video Transcript:

in today's video we're going to break down two of the worst retirement lies told by Finance gurus that everyone believes my company and I help clients all over the United States follow proven advice that allows them to achieve the retirement success they've been looking for unfortunately the internet is Rife with bad retirement advice in many cases leading people to fall for the pitfalls that prevent them from achieving the retirement they've always dreamed of let's look at two dangerous lies promoted by some very well-known Financial gurus I want to start by saying that Dave Ramsey and Susie Orman have done a lot of good helping people with debt paydown strategies the psychology around money and just motivating people to get their financial houses in order and while it's suitable for them to give General personal finance advice retirement planning is an entirely different discipline one that requires the professional giving advice to have experience helping individuals retire in real life the first of these lies is Dave Ramsey's 8% withdrawal rule Dave Ramsey does many things well but his 8% withdrawal rule is one piece of advice that I find to be quite destructive this rule is based on the same concept as the 4% rule which was founded by William benan in 1994 where he states that retirees can safely spend about 4% of their initial retirement portfolio over a 30-year time Horizon adjusted for inflation without running out of money let's say that Kathy and Sam have $2 million at the start of their retirement and will use an annual inflation rate of 3% using the 4% rule they would safely be able to withdraw $80,000 in year 1 and then adjust that amount each year for inflation over that 30-year time Horizon without running out of money so in year two with 3% inflation they would pull $82,400 in year three they would pull 82872 and so on and so forth the study used historical data on stock and bond returns over the 50-year span between 1926 and 1976 there are a number of underlying assumptions behind this rule the most important being that the re must have at least 50 to 75% of their portfolio invested in stocks after many stress tests Benin concluded that even during economic depressions a 4% withdrawal rate would not exhaust a retirement portfolio over 30 years this serves as a good rule of thumb for many DIY investors though it does neglect to account for several risk factors that should be considered high fees the sequence of returns risk which I'll review in just a minute inflation and just general psychology around money you see humans don't spend in a linear fashion meaning that in reality nobody is spending the exact same amount every single year adjusted for inflation some months and years we spend far more than others and we as humans cannot stick to any method that's too strict or too rigid for any length of time a great example of this is trying to lose weight right so crash diets and quick fixes only work temporarily before we give way to our old habits the same way we' fail if we were forced to spend the exact same amount of money every single year we've all heard of the go- go years or those early retirement years where we're still young and healthy and we spend a bit more than we did when we were working then we have the slowo years where we spend a little bit less and then finally the no-go years at an advanced age where we typically only spend 70 to 75% of what we spent in our go- go years this phenomenon is very real and it's what I've seen for the past 15 years in working with retirees so the 4% rule just isn't Dynamic enough to work in the real world well Dave Francy took all of the flaws of the 4% rule and turned it into an entirely unrealistic rule of an 8% safe withdrawal rate if you watch his show or read his books he'll say that if you invest in 100% stock via an S&P 500 mutual fund that your rate of return will be 12% per year and that based on that rate of return you can safely withdraw 8% of your initial retirement portfolio without running out of money in retirement so back to our original chart using $2 million this means using his rule you could safely withdraw $160,000 per year or actually in year 1 and then we can see that that amount inflates each year at 3% now while it may be obvious why this 8% rule is just flat out unworkable I'm going to break down the top three reasons firstly the S&P 500's 50-year average return is 11. 47% not 12% Dave Ramsey may have cherry-picked the top performing years to come up with that 12% return but it's not an accurate long-term average in fact the hundred-year average which is much more thorough right and accurate as it has 50 more years of data is only 10. 69% per year so almost 2% below his claimed rate of return furthermore he neglects to account for very real things like fees and taxes this exaggeration on his part gives investors false hope on realistic returns which one puts their retirement funds at undue risk and two may cause them to run out of money in retirement this brings me to my next issue with this 8% Rule and that is the sequence of returns risk we all remember the Great Recession of 2008 and 2009 where the S&P 500 lost 53.

1% of its value did any of you know someone or maybe that someone is you that had to work longer than anticipated because they lost half of their 401K during that time frame I do that's when I first started in the business and this is the risk that all retirees face experiencing a market drop in the early years of retirement can create problems that go well beyond the immediate hit to your portfolio in fact those who retire during a down Market have a much higher chance of running out of money than those who retire during an up Market think about it if the market drops at the beginning of your retirement your assets will be worth less and more will need to be sold to generate income this can drain savings more quickly and leave fewer assets to generate growth in the future furthermore it prevents the retire you from Gaining back all that they lost during that market drop and that is exactly why his 8% rule would only work if you happen to retire during a great Bull Run if we use the 50-year stock market average of 11. 47% per year and I round it to 11. 5 5% here let's see what kind of results you could get with this rule let's say that you have $500,000 at the beginning of your retirement and your 8% annual withdrawal will increase at 3% per year in this row you can see the returns both positive and negative that amount to an average of 11.

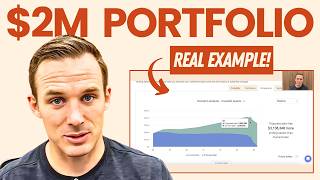

5% or the 50-year S&P 500 average certainly I'm not going to use the Goldilocks 12% of return each year because that's not at all how the stock market works okay so 8% of 500,000 is $40,000 and we can see here how that will rise at 3% per year with inflation in year 1 the S&P 500 returns 33% while you withdraw the 40,000 in year two the market loses 5% while you withdraw 41,800 you can see here what happens to your account value using these Stellar returns during the first 10 or so years of retirement you're actually growing your money while you withdraw your 8% and again if you happen to retire at the beginning of a great Bull Run you can easily withdraw 8% of your initial retirement portfolio and if any of you have access to that crystal ball that tells you when those years start and end let us know in the comments below okay all jokes aside let's look at what could easily happen which is that you retire at the start of a decade with a flat to a slightly positive return you might ask well when has that happened one example would be the Lost decade from 2000 to 2010 other examples include 1929 to 1952 and between 1966 and 1978 I want to point out that the returns I'm using in this example are the exact same returns that I used in the first example in exact reverse order so instead of ending the 20-year time frame with a negative 28% year we're going to start the 20-year time frame with that 28% year 2 is -3% here where it's year 19 here so if we start with the same $500,000 and we withdraw 40% in that same year when the S&P 500 loses 28% we then withdraw 41,00 while the market loses another 3% and then in year three the P 500 returns positive 21% but by this time you can see the damage that's been done in fact by year 10 they've completely run out of money using Dave Ramsey's 8% withdrawal rate this is why it is so important to bucket your money upon retirement more on that in my video here and this doesn't mean that you need to stay conservatively invested throughout your retirement it actually just means that you need to make sure that at least 5 years of living expenses are fixed your first 5 years of retirement within your portfolio so that you're not forced to sell during a Down Market the last reason this rule is decisively wrong is that there's already been a comprehensive study on the likelihood of retirement success AKA not running out of money using an 8% withdrawal rate and the results were terrible after the 4% rule was published three professors at Trinity University in Texas research portfolio allocation and sustainability in retirement using withdrawal rates from 3% per year all the way to 10% per year what they found was that a portfolio invested in 100% stocks only has a 7 4% chance of surviving for 15 years this is not a good success rate and 15 years does not come close to covering the average person's retirement in fact over a 30-year retirement 63% of those with portfolios of 100% stock would run out of money it's important to remember that Dave Ramsey makes a living on your views and the more Sensational his headline and the less people think they have to save and work the more popular he becomes thus the more money he makes okay let's move on to the second worst piece of financial advice from a famous Cal Guru and this one comes from Susie Orman I actually really like Susie Orman especially her budgeting tips and find her to be very inspirational especially for women in finance however she has a retirement rule that is so outrageously inaccurate and that is her 5 million plus rule in episode number 153 of the afford anything podcast Orman told her listeners that 2 million is insufficient to retire early on she said quote but if you only have a few hundred, or a million or two million I'm here to tell you if a catastrophe happens what are you going to do you are going to burn up alive when asked what a safe amount would be she explained it would be in the millions but that it depends on several factors such as where you live your expenses and whether you own a home outright she believes the amount you need to retire early on would be closer to 5 or 10 million not only is this clearly wrong straight off the bat and I'll show you why in a moment but the worst part about her saying this is that she's making her listeners feel guilty for not accumulating 5 to 10 million which we know only very few are able to do but she's also making them feel obligated to work much longer than they have to I know this rule is completely bogus because our firm has helped hundreds of families retire most with less than $5 to10 million but I want to show you using an example let me introduce you to Dan and Kathy Smith a hypothetical Florida couple both 58 years old and they want to retire next month here's the basic overview of their investable assets this does not include their home or other tangible assets just their liquid invest able assets and this is because in retirement your liquid assets are what actually drives your cash flow so they have a high yield savings account worth 100,000 and a jointly owned brokerage worth roughly 375,000 the majority of their investable assets are in Dan's traditional or pre-tax Ira worth a little over $1 million he also has a Roth IRA worth roughly 54,000 Kathy has a traditional IRA worth around 200,000 and a Roth IRA worth a little over 20,000 now we're going to move to our Flagship soft Ware e-money to show you how we would analyze Dan and Cathy's situation here's their Baseline Dan and Cathy are 58 and we're using a life expectancy of 95 years old their goals are to be able to maintain their lifestyle at $100,000 per year or just over $8,300 per month this does include their mortgage which is in a different section under expenses and taxes which I'll show you in a minute at just under 16,000 per year you'll see here that under leave to airs it says zero dollars but that doesn't mean that Dan and Kathy want to leave nothing to their kids it just means that whatever's left will go to them but they don't want to downgrade their lifestyle just to leave their children an inheritance under net worth we can see their liquid investable assets that we reviewed earlier as well as the value of their home at $500,000 and their $200,000 mortgage this brings their net worth to roughly $2. 1 million now Dan and Cathy want to retire next month so they'll have earned half of their annual income for 2024 which is 75,000 gross for Dan and $45,000 gross for Kathy below we have their full retirement age or age 67 Social Security benefits under expenses and taxes we see that everything but their mortgage cost $85,000 net per year in today's dollars between now and their Advanced age or age 85 recognizing an advanced age reduced spend is really important because there comes a point where you just can't do what you did when you first retired typically around 80 to 85 years old this is otherwise known as those noo years that we discussed earlier where expenses typically reduce to 70% of your early retirement spend which for them is $60,000 in today's dollars the software will inflate these expenses at 3. 5% per year we account for their mortgage separately because it's only for a specific time frame and the amount does not increase with inflation unless you have a specific type of variable loan which they don't their annual mortgage payment is $5,673 a year and will be paid off in 17 years the software will drop the expense at that time the software also accounts for federal and state tax but since Dan and Cathy live in Florida it will only calculate federal tax we're going to run several Monte Carlo analysis to determine if they're able to retire next month as is and if not what they need to do to get there a Monte Carlo analysis is the best way to test the success of a financial plan simply put the computer takes a thousand different stock market scenarios between now in Dan and Cathy's life expectancy a third of the scenarios use above average market performance a third use average and the final third use below average market performance the computer then takes your Baseline of information and it runs it against all thousand of these stock market outcomes giving us a percentage of likelihood that you will make it to your life expectancy without running out of money we're looking for a score of 85% or higher but before we do this we need to run an analysis on their current Investments to see what they stand to lose in a major bare Market because I'm going to use that scenario as a stress test to run in the Monte Carlo analysis here we are in riskalyze and this is software that can quantify how much risk a client is taking so that we can see how vulnerable they are to the sequence of returns risk which I explained earlier essentially we want to make sure that Dan and Cathy can withand a major bare Market in the beginning of their retirement so they do not run out of money in their 80s or sooner riskalyze scores portfolios from 1 to 100 one being cash CDs fixed annuities High old money markets basically Investments that can't lose value the S&P 500 scores a 73 and Bitcoin or a very volatile individual stock would score 100 we can see here that their overall portfolio scores a 66 out of 100 and their asset class breakdown is 79% stock 18% cash or in this case a high old money market fund and 3% other which refers to some Commodities you can also see that each separate account has its own risk score under the overall score we can see that their average annual return is 99.

82% this is great information but the real question is with this specific investment allocation what do they stand to lose if we go into recession next year or their first full year of retirement under stress test we can see several scenarios and their outcomes but I want to focus on the third scenario the if a financial crisis were to happen again this model is what occurred between October 15th of 2007 and March 2nd of 2009 where the S&P 500 lost 53. 1% of its value if that occurred again Dan and Cathy would lose 47% or roughly $800,000 of their 1.

Related Videos

14:10

Is a Fully Paid Off Home in Retirement REA...

Holy Schmidt!

376,544 views

13:05

10 Possible Changes to the Federal Employe...

FIRE Psy Chat

107,389 views

18:14

This Is The Only Withdrawal Strategy That ...

Ari Taublieb, CFP®

152,320 views

34:54

Full Show: 6 Mistakes To Avoid Before Reti...

Clark Howard: Save More, Spend Less

10,212 views

13:31

The $1.8 Million Retirement Lie: How Much ...

Humphrey Yang

442,177 views

8:27

Why Net Worth SKYROCKETS After Retirement

Holy Schmidt!

124,596 views

16:51

Retirement Regrets: The Biggest Regrets Fr...

Parallel Wealth

307,727 views

21:49

Dollar General CEO: "Consumers ONLY HAVE E...

Michael Bordenaro

34,229 views

9:36

What Does it Take To Retire on $7,500 per ...

Azul

80,997 views

16:45

Retire With 5 Million Dollars: Here’s What...

Three Oaks Wealth

148,929 views

26:18

17 Challenges Single Retirees Will Face

Parallel Wealth

122,001 views

12:27

I QUIT Traditional Retirement Planning and...

Kevin Lum, CFP®

160,702 views

23:06

I’m 60 with $2M How Much Can I Spend in Re...

James Conole, CFP®

125,569 views

14:41

My Honest Advice TO Anyone Under 59... Sto...

Nick Davis, CFP®

254,147 views

27:35

We Have Over $2 Million (Age 57) | How Muc...

Ari Taublieb, CFP®

21,457 views

10:22

6 Negative Retirement Surprises After 6 Mo...

Azul

140,158 views

30:59

How to Retire at 55. 3 Crucial Steps to Op...

James Conole, CFP®

169,183 views

11:22

5 Years From Retirement? Do These 5 Things...

Atterbury Investment Management

13,101 views

14:28

Fidelity Is Wrong! Use This Savings Rule I...

Retire with Julia, CFP®

29,198 views

12:13

Money Lessons From Older Americans Who Lea...

Business Insider

1,181,330 views