Keynesian economics | Aggregate demand and aggregate supply | Macroeconomics | Khan Academy

1.34M views2237 WordsCopy TextShare

Khan Academy

Courses on Khan Academy are always 100% free. Start practicing—and saving your progress—now: https:...

Video Transcript:

Voiceover: What I want to do in this video is start introducing and we've already talked about him a little bit. So actually they've already been introduced, but maybe flesh out a little bit more Keynesian thinking. This right here is a picture of John Maynard Keynes and I often mispronounce him as Keynes, because that's how it's spelled, but it's John Maynard Keynes.

He was an economist who did a lot of his most famous work during the Great Depression, because in his view, classical models did not seem to be of much use during the Great Depression. To understand this a little bit better, let's compare purely classical aggregate supply aggregate demand models to maybe one that's more Keynesian. Some of what we've talked about - Keynesian, I should say.

I already did my first mispronunciation. One that's a little bit more Keynesian. Keynesian right over here.

In some of the conversations, we've already begun to introduce a little bit of Keynesian thinking, but in this video we're going to try to show the difference between the two and it's not to say that one is right or one is wrong. In fact, Keynesian felt that in the long run, the classical model actually made sense, but he also famously said, "In the long run we are all dead. " I also want to emphasize that this isn't a defense of Keynesian economics.

There are some points to what he has to say, but there are other schools of thought. Unfortunately, they often get very dogmatic, but they also have some reasons to be wary of Keynesian economics and we hope to go over some of that in future videos. In this one, we just want to understand what Keynesian economics is all about and how it really was a fundamental departure from classical economics.

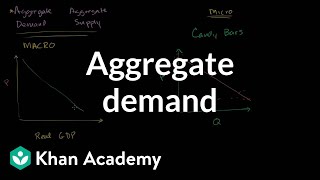

In classical economics, I'm going to use aggregate demand and aggregate supply in both. This is classical, this is price, this right over here is real GDP and I'm going to do it for the Keynesian case, as well. This is price and this right over here is real GDP.

In both views of reality, or both models, you have a downward sloping aggregate demand curve for all the reasons that we've talked about in multiple videos. That's aggregate demand right over there. We've already seen it, the classical view is that in the long run, an economy's productivity, or productive capacity, or its output shouldn't be dependent on prices.

We've seen the long run aggregate supply curve something like this. This is the aggregate supply in the long run, or sometimes you'll have long run aggregate supply. Sometimes it'll be referred to that.

Saying, look, all prices are, they're a way to signal what people want and demand and things like that, but at the end of the day, prices and money, they're just facilitating transactions. You go to work and you get paid and all that, but then you go and use that money to go and buy other things that the economy produces, like food and shelter and transportation. All money is is a way of facilitating the transactions, but the economy, in theory, based on how many people it has, what kind of technology it has, what kind of factories it has, what kind of natural resources it has, it's just going to produce what it's going to produce.

If you were to just change aggregate demand, if the government were to print money and aggregate demand were to - and just distribute it from helicopters, in this classical model, you would just have aggregate demand shift to the right, but you have this vertical long run aggregate supply curve so the net effect is it didn't change the output in this classical model. All that happens is that the price goes from this equilibrium price to this equilibrium price over here. You have the price would go up and you would just experience inflation with no increased output and there's multiple ways you could've shifted that aggregate demand curve to the right.

You could have a fiscal policy where the government, maybe it holds its tax revenue constant, but it increases spending, or it goes the other way around. It does not decrease, it doesn't change its spending, but it lowers tax revenue. Either of those, it tries to pump money into the economy and pushes that aggregate demand curve to the right.

In this purely classical view, it says in the long run, that's not going to be any good, just will lead to inflation. The only way that you can increase the output of economy is by making it more productive. Maybe making some investments in technology, make the economy more efficient, maybe your population grows.

The only way is to really shift this curve to the right on the supply side right over here. Keynes did not disagree with that, but he sitting here in the middle of the Great Depression, saying, "Look, all of a sudden people are poor in the 1930s. "Factories did not get blown up, people didn't disappear.

"In fact, there are factories that want to run, but they are being shut down, because no one "is demanding goods from them. "There are people who want to work, but no one "is asking them to work. "They could work and produce wealth that could then "be distributed to - "But no one's demanding for them to do it.

" He suspected something weird was happening with aggregate demand, especially in the short run. In a very pure, very, very short run model, I know we have talked about a short run aggregate supply curve that is upward sloping. Something that might look something like that.

That is actually starting to put some of the Keynesian ideas into practice. What I like to think of is something in between, but if you think in the very, very, very short term, Keynes would say prices are going to be very sticky. Especially in the short run, and I'll call it the very short run, you have, especially if the economy's producing well below its capacity, like it seemed to be doing during the Great Depression, prices are sticky.

That makes intuitive sense. If the economy's trying to get overheated, people are being overworked, you want them to work more, hey, I want overtime. You want factories to operate faster, people are going to start - The utilization is high, people are going to start charging more and more, but if I'm unemployed and I'm desperate to work, I'm not going to ask for a pay raise.

If my factory is at 30% utilization and someone wants to buy a little bit more, that's not the time that I'm going to say, "Hey, I'm going to raise prices on you. " I'll say, "Yeah, exact same price. "You want another 5% of my factory to be utilized?

"Sure, that sounds great. " In the very short run, it has the opposite view of the aggregate supply curve than the classical model. It says at any level of GDP in the short run, prices won't be affected.

It won't be affected. So in this model right over here, this is aggregate supply I'll call it, in the very short run. You can debate what short run or very short run means, whether we're talking about days, weeks, months, or even a few years here, but once you start looking at the world this way, then something interesting happens.

In this model right over here, the only way to increase GDP was on the supply side. In this model right over here, the only way to increase GDP is on the demand side, to actually either through monetary policy, print more money, or through fiscal policy, lower taxes while holding spending constant or maybe do both, essentially deficit spending. Someway, without holding taxes constant, but the government's spending more, whatever.

Shift the curve to the right and that might be a way to increase the overall output. Keynes' real realization was that, look, the classical economist would tell you if you have a free and unfettered market, the economy will just get to its natural, very efficient state. Keynes says, "Yes, that is sometimes true, "but that's sometimes not true.

" We'll talk about different cases. By no means do I think the Keynesian model is the ideal and I don't think even Keynes would have thought the Keynesian model describes everything. Depends on the circumstance.

Keynes would say, "Look, let's think "of a very simple idea. " You have person A, person B, person C, and person D. Let's say person A sells to person B, person B sells to person C, person C sells to person D, and person D sells to person A.

Let's say that they're all selling two units of whatever good and service that they offer. For whatever reason, let's say C, all of a sudden, just got a little bit pessimistic, had a bad dream, woke up on the wrong side of the bed and says, "You know what? "I'm not feeling so good about the economy.

"I'm going to hold off from my purchase from B. Instead of two units, I'm going to purchase one unit. Well, B says, "Well, gee, my business is bad.

"Now I'm only going to purchase one unit. " A does the same thing for the same reason, D does the same thing. Now it all came back to C and now C says, "Wow, I was right, that dream was predictive.

" It was a self-fulfilling prophecy. Now they're going to operate in this state and there might not be any natural way to get them bumped up to that state where they're all buying two units from each other without maybe some outside, especially some government act or maybe all of a sudden saying, "Hey B, if C doesn't want to buy two, I'm going "to buy two temporarily. " There are dangers to this, huge dangers, and we'll talk about that in future videos, but then someone else, let's say the government, tries to shift the aggregate demand curve through fiscal policy and they say, "Hey, I'll buy one from you, B.

" Then B says, "Okay, now I can buy two again," and A can buy two again and then D can buy two again and then C can buy two again. Then in an ideal world, and this is the danger of the government, the government would step back and say, "Okay, everything is fine again. "I don't have to buy this.

" As we know, it's very hard once the government starts spending money in some way, to actually cut this spending right over here. This was the general idea behind the Keynesian versus the classical. He says, "Look, there are circumstances, "like the Great Depression, where the economy "is operating well below its potential "and in those circumstances, you need to have "a stimulus on the demand side, not just a supply side.

" The correct answer, as with all things, is probably something in between. A probably more accurate model is something like this. Let's draw .

. . This is price, this is real GDP right over here and we'll still draw our downward sloping aggregate demand curve and the more accurate thing might look something like this.

Let's say that this is the absolute theoretical maximum output, if everyone in the country isn't sleeping, the factories are just being run to the ground, that's the absolute theoretical output. Let's say that this is its potential. Just a healthy state where the economy might be operating.

The real medium run supply curve or short run aggregate supply curve. This is aggregate supply in the very long run. This is the long run aggregate supply.

The best model would be something that's in between and might look something like this. Our aggregate supply curve might look something like - I want to do it in a different color. Let me do it in magenta.

It might look something like this. For whatever reason, maybe someone has a bad dream or a bunch of people have a bad dream or something scary happens, aggregate demand - The stock market crashes, something happens, aggregate demand shifts over there. When we're out here, now all of a sudden our output is well below potential, we have a lot of excess capacity and now the Keynesian ideas seem maybe they'll make sense.

Maybe there should be some outside stimulus happening. On the other side, if we're performing well at potential, then all of a sudden the government wants to do Keynesian policies and we'll see in future videos, the government will always want to do Keynesian policies, even if they're not justified. It will push aggregate demand out here and then the net effect is, especially the more vertical this is, the more this net effect will be true, that you really just get more inflation and you don't really get a lot of increase in output.

It really depends on the circumstance, but an aggregate supply curve that starts flat at low levels of output and then gets higher and higher slope and becomes almost vertical in your high levels of output, this is probably a better model that takes into consideration both the classical and the Keynesian ideas.

Related Videos

8:14

Risks of Keynesian thinking | Aggregate de...

Khan Academy

188,828 views

13:53

Aggregate demand | Aggregate demand and ag...

Khan Academy

1,533,070 views

9:20

Keynesian Cross

Khan Academy

387,311 views

13:32

Macro: Unit 2.6 -- Classical v. Keynesian ...

You Will Love Economics

386,217 views

18:21

THIS is Why Your Heat Bill is So High

Home RenoVision DIY

317,169 views

8:46

Tim Walz 'struggling' to accept election loss

Sky News Australia

309,431 views

5:06

Italian Restaurant Commercial - SNL

Saturday Night Live

316,103 views

16:06

The Greatest Mathematician Who Ever Lived

Newsthink

384,709 views

1:43:36

Chapter 33: Aggregate Demand and Aggregate...

DrAzevedoEcon

89,722 views

4:03

Gladiator II Trailer - SNL

Saturday Night Live

476,997 views

18:50

Who are the Syrian rebels and where is Bas...

BBC News

283,405 views

1:38:06

Best Fails of the Year | Try Not to Laugh ...

FailArmy

2,977,088 views

34:47

1. Introduction and Supply & Demand

MIT OpenCourseWare

2,559,993 views

33:01

蔡霞有话说:从末世到乱世—中国模式的失败

美国之音中文网

249,894 views

13:00

1 Year Later: How Has Argentina Been Going?

Economics Explained

99,161 views

29:58

Macroeconomics- Everything You Need to Know

Jacob Clifford

3,513,578 views

5:16

Keynesian Economics and Deficit Spending w...

Jacob Clifford

617,488 views