The international banking system is an enigma. There are more than 30. 000 different banks world wide, and they hold unbelievable amounts of assets.

The top 10 banks alone account for roughly 25 trillion US-Dollars. Today, banking can seem very complex, but originally, the idea was to make life simpler. 11th century Italy was the centre of European trading.

Merchants from all over the continent met to trade their goods, but there was one problem: too many currencies in circulation. In Pisa, merchants had to deal with seven different types of coins and had to exchange their money constantly. This exchange business, which commonly took place outdoors benches, is where we get the word "bank" from; from the word "banco", Italian for "bench".

The dangers of travelling, counterfeit money and the difficulty of getting a loan got people thinking. It was time for a new business model: home brokers started to give credit to businessmen, while genevese merchants developed cashless payments. Networks of banks spread all over Europe, handing out credit even to the church, or European kings.

What about today ? In a nutshell, banks are in the risk management business. This is a simplified version of the way it works.

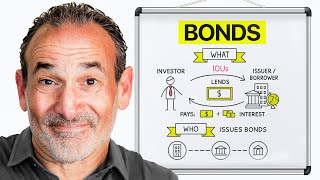

People keep their money in banks and receive a small amout of interest. The bank takes this money, and lends it out at much higher interest rates. It's a calculated risk, because some of the lenders will default on their credit.

This process is essential for our economic system, because it provides ressources for people to buy things like houses, or for industries to expand their businesses and grow. So banks take funds that are unused by savers, and turn them into funds society can use to do stuff. Other sources of income for banks include accepting saving deposits, the credit card business, buying and selling currencies, custodian business and cash management services.

The main problem with banks nowadays is, that a lot of them have abandoned their traditional role as providers of long-time financial products, in favour of short-time gains that carry much higher risks. During the financial boom, most major banks adopted financial constructs that were barely comprehensable and did their own trading in habit to make fast money, and earn their executives and traders millions in bonuses. This was nothing short of gambling and damaged whole economies and societies.

Like back in 2008, when banks like Leeman Brothers gave credit to basically anyone who wanted to buy a house, and thereby put the bank in an extremely dangerous risk position. This led to the collapse of the housing market in the US and parts of Europe, causing stock prices to plummet, which eventually led to a global banking crisis, and one of the largest financial crises in history. Hundreds of billions of dollars just evaporated.

Millions of people lost their jobs and lots of money. Most of the world's major banks had to pay billions in fines and bankers became some of the least trusted professionals. The US government and the European Union had to put together huge bailout packages to purchase bad assets and stop the banks from going bankrupt.

New regulations were put into force to govern the banking business, compulsary bank emergency funds were enforced to absorb shocks in the event of another financial crisis. But other pieces of tough new legislation were successfully blocked by the banking lobby. Today, other models of providing financing are gaining ground fast.

Like new investment banks, that charge a yearly fee and do not get commissions on sales, thus providing the motivation to act in the motivation in the best interests of their clients. or credit unions - cooperative initiatives that were established in the 19th century to circumvent credit sharks. In a nutshell, they provide the same financial services as banks, but focus on shared value rather than profit maximisation.

The self proclaimed goal is to help members create opportunities like starting small businesses, expanding farms or building family homes while investing back into communities. They are controlled by their members, who also elect the board of directors democratically. World wide, credit union systems vary significantly, ranging from a handfull of members to organisations with several billion US-Dollars and hundreds of thousands of members.

The focus on benefits for their members impacts the risk credit unions are willing to take, which explains why credit unions, although also hurting, survived the last financial crisis way better than traditional banks. Not to forget the explosion of crowdfunding in recent years. Aside from making awesome video games possible, platforms arosed that enabled people to get loans from large groups of small investors, circumventing the bank as a middle man.

But it also works for industry - lots of new technology companies started out on kickstarter or indiegogo. The funding individual gets the satisfaction of being part of a bigger thing, and can invest in ideas they believe in. While spreading the risk so widely, that, if the project fails, the damage is limited.

And last but not least, micro credits. Lots of very small loans, mostly handed out in developping countries that help people escape poverty. People who were previously unable to get access to the money they needed to start a business, because they weren't deemed worth the time.

Nowadays, the granting of micro-credits has evolved into a multi-billion dollar business. So, banking might not be up your street, but the banks' role of providing funds to people and businesses is crucial for our society and has to be done. Who will do it and how it will be done in the future is up for us to decide, though.