No Caminho do Superendividamento [ minidoc completo ]

17.1k views2707 WordsCopy TextShare

Idec

61 milhões de brasileiros estão endividados.

Muitos fazem empréstimos para pagar outros empréstimo...

Video Transcript:

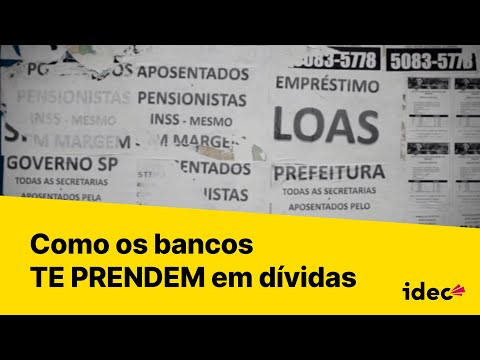

Realization: Idec and Brazilian Fair Finance Guide Member of the coalition Fair Finance Guide International (FFGI) Support: OXFAM Novib and Sverige Production: Coletivo Bodoque de Cinema In Brazil, 62 million people are indebted. (Source: CNDL/SP) When you have 61 million adults in debt in a 210 million-people country we have around 130 million adults, if you include these adults with their families you are talking about half of Brazil's population, that is struggling with debts 25 million Brazilians cannot afford to pay their debts They are the overindebted. The over-indebted has no face, race or age no, it can be any of us I would say that there are some privileges that I have as a middle-class is a type of access to the financial banking system an access that can make me vulnerable to this system, as a matter of fact it already did And when people are over-indebted they lose their dignity I’m leaving the economy, I’m not a consumer anymore Title: "In the Path of Over-indebtedness" My name is Rubens and I’m a Professor of a Public University I’ve been teaching classes for 42 years I’ve been doing research projects in University for 35 years Nowadays I continue to work, I continue mentoring students, doing research and so on As I was earning more money, I was also starting to receive more offers from the banks and the financial system Idec is following the discussions about over-indebtedness more regularly for the past 10 years The most recent research indicates that 60% of the consumers find it difficult renegotiate their debts either because it is difficult to reach the banks because the payment is not late yet or because they receive proposals that are well above their ability to pay We receive an Idec associate that came asking for help, because he was in this process at first, he was listened by Idec’s Relationship with Associates Area Idec’s advisor was taking care, as we usually do we normally give a guidance and we recommend going to the bodies which are in fact competent to assist people however, the case of this associate caught our attention by the size of Rubens’s over-indebtedness and by the socio economic profile that he is part so being a very qualified person with an income well above the average of the Brazilian population Analyzing the whole history, we took this process as a case study he has 120% of is income fully committed to credit operations in only four banks The alarm was already on for a long time but things were happening and I knew I had to find a solution I had to go to some government body and look for some help, so I started looking on the internet for these questions What I feel is that these loans at a given moment were being exchanged for other loans in which the bank itself said: “look, now the interest rate changed, so you can take some money, then you pay your credit card, pay the overdraft Picture this, over time, it began to happen much faster than before first, you have this appeal, more or less intense, that has the idea of producing desire effectively, creating a need then you have the credit as a tool to enable you to satisfy the need and the desire and then you have the publicity, the offering the credit offer, the products and services’ offer and the credit offer also as a product and service Jonas, renew your payroll loan!

You have a system extremely concentrated on the credit offer, the publicity is extensive, aggressive it is constant and then you have the responsibility of these companies and industries for the desires and necessities that they create and the facilities that they allow so everything is very connected "Money without Bureaucracy" "Credit for your dream! " Get out of a financial struggle Credit without complication! Money for people with bad credit Buy now, pay only in 90 days You, retired, pensioner, needing money?

Credit pre-approved Money? Credit pre-approved The first impression we had was “wow, this is a person without financial control” it was the first one, “he is a shopaholic” So we analysed the case internally, we analyzed his personal accounts all his personal accounts and we identified that he is the “ideal” person for the banking system How much Rubens paid monthly Credit operations with fixed payments he pays a lot of fees, he pays home insurance, he pays health insurance he pays insurance for the protection of credit operations, he pays capitalization bonds in other words, he does not have investment, but he pays all the products that a bank can offer Total Net Debt: R$ 628 thousand Somehow I was treated as the “VIP customer” I never knocked on the bank’s doors at some point, the bank manager’s phone calls were being weekly sometimes twice to three times a week Why had not his situation been questioned at any time before? and even after all this history and process the banks are still offering him credit so he still has credit, he has received a credit card he received a proposal to increase the overdraft limit to have more freedom They never told me, I mean, I do not know They must have a training, including this new generation of bank managers, that orients them to not mention risks and to not mention negative things The credit manager has a salary bonus, that will depend on how much he can shove a set of insignificant items a insurance here and one more of another item the bank’s internal decision-making process has a bank manager that smiles for you, but screws you it is not because the bank manager is evil, but it is how the system works He always succeed in these adjustments and he could afford to pay until some point, we cannot say he doesn't, he did that for 3 years, almost 3 years and half so he really managed to keep his life without default, but this does not mean that he had quality in financial life actually he did not because he transferred his entire outcome, he stopped being a consumer because he became a credit consumer the reality is that a large proportion of consumers when you keep constant and pointless credit lines, “Why am I taking credit?

” “What is the purpose of this credit? ” and I’m transferring this for the system I’m leaving the environment I’m leaving the economy I am no longer a consumer And within this history that he reported, he was not able to talk to the banks to continue negotiating his debts Good afternoon. Good afternoon.

My name is Rubens Adorno and I'm calling this cannel because I already tried to call my account bank manager for loans and financing: click 2 for an individual account: click 3 for negotiations SERADA "Name Clean". . .

The reason I'm calling is because I want to regotiate. . .

Click 1 for loans I see, but you cannot negotiate here because of this how your bills are paid, I cannot do a simulation because you don't have any arrears The credit is economically positive, for a country’s economy but not in the way it has been used in Brazil People are taking credit to integrate to their income to pay their day-to-day expenses There is a very particular relationship between payroll loan, concession of payroll loan and the transformation of loans into automatic payment with automatic payment back, with the rising of the phenomenon of over-indebtedness I say this without a doubt and also affirm that the banks’ refusal to negotiate contracts on time that is, the person is seeing that he will not be able to pay knocks on the banks’ door and says: “look, I’m suffocated next month I will not be able to pay anymore” this also boost the phenomenon of over-indebtedness Default Ranking By line of credit (%) Credit Card - Revolving 33,2% Debts composition (Renegotiation) - 17% Overdraft - 13,6% The loans that the person can not stop paying are the most severe ones payroll loans, loans with automatic debit payment because the person can not choose not to pay I’m short of money I will pay this first, pay that first to reorganize myself Look, it is not in the bank interest to have over-indebted consumers this is why the sector has developed a series of actions focused on this theme is a series of measures under discussion that will improve the Positive Credit Law it can benefit the consumer in several ways The first measure is based on knowing the consumer better You know more about the indebtedness and his payment possibility degree it can turned into more beneficial rates to the consumer The Negative Credit Law already exists, and it works when the person delays a debt or do not pay his name goes to a database called Negative Credit Then the government proposed to create the Positive Credit Law The good payers list where people are being evaluated by their credit history and will have a better offer of interest rate If I have some more structural situations a person that tends to be a bad client, if I have some type of articulation, of overload, which will tend to lead that person to take out the loan and not pay it properly he will be always in the bad payers list and never in the good list therefore, the Positive Credit Law will not be a solution for him Rubens adopted the Positive Credit list in 2013 he is within the requirements In thesis he is in the Positive Credit list, all the banks have the access to his record and even so, he became over-indebted with low interest rates I welcome many international economists to show banks’ documents, because they do not believe that a bank can charge 485% over revolving credit The indignation in the United States is because reached 16% per year in certain cases Interest Rates Average for Loans (per year) Source: World Bank We also started to follow the process of Rubens physically we went to bank agencies, where he has accounts we presented his bank past information, we talked about the importance of having means to renegotiate his debts, because he no longer had conditions to pay and even then every bank looked at the situation inflexibly the alternatives were always reversed in the form of more credits more credits and more credits So in reality the financial system has become a dominant way of extracting surplus from the purchasing power of households equalizing or surpassing what is extracted from people through wage exploitation, wage reduction and rights limitations that is, we live a policy that keep people in the world of credit forever In 2003, credit corresponded to 26% of Brazil's GDP In 2017, this percentage rose to 47% Most of this growth is a result of the influx of payroll-deductible loans into the market. When you pressure many families with interest rates you gradually reduce the purchasing power of these families the payment in installments will not only present interest per annum, but per month how they are going to present an installment that "fits in the pocket" But it is what happens in Brazil, especially because of the very high interest rate One or two wrong financial decisions and a person is already almost over-indebted Today you have Banco do Brasil, Caixa Econômica Federal Bradesco, Itaú e Santander, concentrating 85% of the asset market in the country How did the banks organize such a surrealist high interest system? The logic is very simple because we have already studied this in countless sectors that practice overprices In this case the overprice is the interest rate This is a cartel Cartel (noun): "Comercial agreement between enterprises, aiming the distribution between them of production and market quotas in order to determine prices and limit competition.

(Source: Dicio Dictionary) So we throw the ladder higher interest rates make families go into debt freeze their consumption capacity 61 million adults, the majority of the population what freeze the capacity of business activities and also freeze the money that goes to the State that generates a federal budget deficit and reduces the State capacity to provide the other side of welfare to the families what we call “indirect salary” which is the free school and the Public Health System and a set of rights that in well developed countries work and are universal and free because it is an investment in people In my last attempt to solve the volume of loans to solve other loans was suggested it was advantageous to make another loan with a property as guarantee and I’m paying The bank itself offers him to pay the bank itself with a loan modality that would be able to take the only family asset that he has whereas he could default on those other credits that don’t pledge a family asset, he would default, period and living in his home and a bank offers to him to solve the problem with the bank itself with a credit modality that takes his house bad faith, at a minimum, right We do not have regulatory body that regulates the relation between credit provider and the final consumer Today we do not have a law that can welcome the consumer to treat the over-indebtedness what we have today is still very far from a treatment that will bring to these indebted families the possibility of leaving this cycle Public policy to reduce the over-indebtedness the regulatory body can penalize banks that lend irresponsibly is to bring resolutions of responsible lending of credit not just punish, but also guide This goes through self-regulation and policy debate and also through debate in institutions concerned with consumers involving institutions concerned with the financial system involving the academia, this question goes through the judiciary, legislative and executive powers There are moments in this process that you informing yourself I mean, for me, is like a night sleep we feel like this At night you begin to think “Well, what if such thing happens? ” “What if they send me a letter, if this and that? what do I do?

What do I do? ” I would not want to give up this space every object has a bit of history of what marks a little of our life trajectory After undergoing two collective conciliation attempts without agreements in early 2017, Rubens went into default and had his name in the bad payers list by the four creditor banks. After 42 years of work, he retired.

Their monthly income was reduced. The situation got worse. He continues to pay on time only the home equity loan, which represents 40% of his debt.

The total of the current debt without interest is R$ 628. 000,00. Hardly will he pay that debt in life.

Since 2015, the Bill 3515 has been passed in the Brazil's Chamber of Deputies. It aims to include two new chapters on over-indebtedness in the Consumer Defense Code. One chapter deals with debt prevention, regulating lending, advertising and making risks more evident.

The other aims to guarantee better conditions for reconciliation of debt with financial institutions. The bill is still pending before the Chamber of Deputies and can be voted on at any time. Access www.

idec. org. br/superendividamento to follow the process and strengthen the cause.

Related Videos

18:46

Como funciona a LEI DO SUPERENDIVIDAMENTO?...

SuperRico - Saúde Financeira

8,260 views

20:15

Qual a Questão - Insegurança alimentar

Câmara dos Deputados

9,050 views

58:47

Superendividamento é o tema do Entender Di...

Superior Tribunal de Justiça (STJ)

9,464 views

2:29

DÍVIDAS: quase METADE DA POPULAÇÃO adulta ...

Jornalismo TV Cultura

1,698 views

8:49

SE VOCÊ TEM DÍVIDAS EM EXCESSO PRECISA ASS...

Geraldo Rufino

1,243,650 views

15:12

COMO BBAS3 VAI TE DEIXAR RICO - BANCO DO B...

Clube do Valor

37,163 views

10:29

O partido que faz alemães temerem a volta ...

DW Brasil

341,736 views

5:35

Entenda o "OURO" da LEI DO SUPERENDIVIDAME...

E-Goulart Advocacia

43,391 views

7:41

Jovens que não estudam e não trabalham est...

Domingo Espetacular

414,794 views

26:40

🎥 Documentário - Educação financeira

Rádio e TV Justiça

19,164 views

12:09

COMO LIMPAR SEU NOME E SAIR DAS DÍVIDAS (p...

Me Poupe!

3,232,221 views

17:13

Método BOLA DE NEVE para pagar as dívidas ...

Em Casa Com Joice Milacci

697,449 views

1:57:26

O primeiro ano de implementação da nova no...

Idec

762 views

9:30

CIENTISTAS DESCOBRIRAM os segredos do VÍCI...

Olá, Ciência!

188,312 views

2:16:56

Financiamento da Cadeia da Carne: Instrume...

Idec

453 views

42:54

Decisões de acordo com a lei!#lei14181 #su...

Alencar Advocacia

6,201 views

3:55

Lei do Superendividamento: O que é? Como F...

Acordo Certo

29,147 views

6:30

Semana Sustentável 2023 - Comunidades que ...

Idec

494 views

1:00:35

Entendendo "O Dilema das Redes" e Como Voc...

Fabio Akita

211,645 views

7:42

CONSUMO X CONSUMISMO X COMPULSÃO POR COMPR...

PodPeople - Ana Beatriz Barbosa

128,233 views