Poor Man's Covered Call Tutorial

105.31k views2896 WordsCopy TextShare

tastylive

Subscribe to our Second Channel: @tastylivetrending

Check out more options and trading videos at www...

Video Transcript:

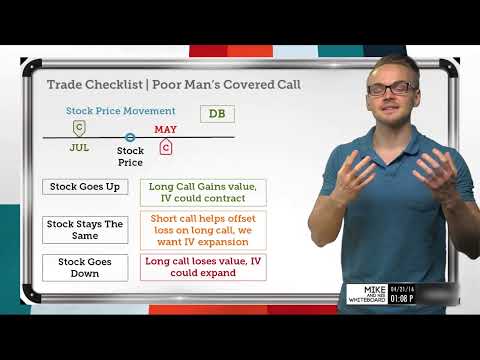

[Music] hello everyone welcome back to the show my name is mike this is my whiteboard today we're going to go over the trade checklist for a poor man's covered call otherwise known as a long call diagonal spread yesterday we talked about the long put diagonal spread and how we can use that in a low volatility environment when we have a bearish assumption on an underlying today we're going to look at the long call diagonal spread we're going to talk about the differences between the long call diagonal spread and the long put diagonal spread both of

which will be impacted and benefited by an increase in implied volatility although they do have opposing directional assumptions so let's get right into the long call diagonal spread and you'll see it's very much like the poor man's covered put or the long put diagonal spread where we have an in the money option that we're buying and we're selling an out of the money option against that to reduce our cost basis on that long option so here we've got the poor man's covered call and in this case in the money would mean below the stock price

when we're looking at a call option a call is in the money when it's below the stock price because a call contract is the right to buy 100 shares of stock at a certain strike so if we can buy it down here when the stock price is trading up here then this is going to have intrinsic value at expiration it'll be worth something because it gives that person the right to buy shares of stock at a lower price than they could in the market one interesting thing to point out when we're looking at these diagonal

spreads is that it's really just a combination of a calendar spread and a vertical spread so we know that a vertical spread is where we're just buying an option on a different strike then we're selling the option or if we're looking at a credit spread it would be the same thing but both of these options would be out of the money we're still just selling an option on a different strike than what we're buying but what's interesting about the diagonal spread is the combination of that vertical spread aspect with the calendar spread so the calendar

spread would be if we were just purchasing an option right here on this strike in july and selling an option on that same exact strike in for example may when we combine these two where we're buying an option in a further date at expiration and we're selling an option on a different strike in a near-term expiration that's what creates that diagonal spread and gives us the benefit of the directional assumption that we have but also that implied volatility assumption where we want implied volatility to increase that's how this spread works and that's why it's so

beneficial this is also going to be routed for a debit just like the poor man's covered put which was also routed for a debit but in this strategy it's going to be a covered call replacement strategy this is another one of those strategies where if we're looking to get that bullish assumption or bullish bias and have that replication of a covered call strategy but we don't want to put all the capital down that would be required for that covered call this would be our go-to replacement strategy again it is ideal for low iv environments and

that's because of the fact that we're going to have long vega exposure volatility is going to impact longer dated options or options that have longer days till expiration much more than shorter dated options so because i'm buying the longer dated option in july and i'm selling the option in may i'm going to have a long vega exposure i want implied volatility to increase because it would increase the value of my july call much more than we would see the loss on that may call that we're selling so we want implied volatility to increase in this

scenario and again our assumption is bullish because at the end of the day we want the stock price to move up because when the stock price moves up our long call that we have in july is going to gain intrinsic value and our short call here that we've sold for purely extrinsic value since it's out of the money here even if it moves in the money if it moves a couple points in the money we're still going we're going to be able to offset that loss that we see here with the gain that we'll see

on that july call if we remember when an option moves in the money it's just moving in the money by its intrinsic value so if it moves two points in the money here with my short call i'll see two points of loss but that also means i'll see two points of gain or profit on that long call because that's going to gain intrinsic value so don't worry about if the stock price blows through our short strike here that would be exactly what we want in this strategy and that's what's going to make us profitable here

but let's talk about a few other ways that the stock price can move and how it will affect this particular strategy on the next slide so we did talk about how when the stock price moves up that's exactly what we want and that's because the long call will gain value one thing to point out is that this strategy differs from the poor man's covered put or the long put diagonal spread in the sense that iv is going to contract or could contract when the stock price actually moves in our direction so in this strategy we

want implied volatility to increase but if we know that there is a general market relationship between a market increasing and implied volatility decreasing where we usually see when a market drops pretty quickly we'll see implied volatility spike that's going to benefit the poor man's covered put in a way that's going to accelerate that p l or accelerate the profit if it does move down but it would also accelerate the loss on the upside implied volatility affects a poor man's covered call more like a hedge so we if the stock goes up we will see profit

on that long call but we're going to probably see iv contract which is going to pull down the value of these options a little bit so we're not going to see that accelerated profit as we would in a poor man's covered put in this strategy we're going to see we're going to see profit at the end of the day but it's not going to be as drastic as a poor man's covered put could be when the stock price stays the same the short call is going to help offset the loss on that long call because

remember we do purchase this long call for more than intrinsic value we're purchasing it for at least intrinsic value but since there's so much time on that option there's going to be extrinsic value applied to that option as well so every single day that goes by where the stock price stays the same we're going to see that long call lose a little bit of value and a little bit more and a little bit more every single day that goes by but since we sold this option we're going to see this option lose value as well

so that's going to help us offset that theta decay that we would normally see if we were just long this option and that's exactly why we sell this option against that long option to help us offset that basically what we want to happen if the stock price stays the same is we want to see implied volatility increase that would be the best case scenario because again when implied volatility increases that's going to increase the value of our long call more than it will see the loss on that short call here so we want implied volatility

to expand when we're dealing with these diagonal spreads or calendar spreads for that matter as well when the stock goes down we are going to see the long call lose value but again we can see iv expand so if we realize that when a stock price tends to drop we usually see implied volatility increase that's going to help us hedge our losses so just like when the stock price goes up and we don't we won't see that expansion in profit just like we would for maybe a poor man's covered put when the pr when the

stock price goes against us with the poor man's covered call here it's going to actually help us a little bit because if implied volatility is expanding while the stock price is going down the expansion in implied volatility will help us offset the losses that we see on this spread because of the fact that when implied volatility expands that's just a reflection of the option prices increasing so even though we'll see a lower intrinsic value on that long call the extrinsic value should increase in terms of value so that's going to help us hedge our losses

here so when we compare a performance covered call to a poor man's covered put poorman's covered put the directional assumption and the implied volatility expansion will work hand in hand together whereas a poor man's covered call they work as more of a hedge against each other so if we're directionally wrong with appointments covered call we should see implied volatility increase a little bit which should help us with those losses and if we are directionally right we're usually going to see implied volatility contract a little bit or it could contract a little bit which could hinder

those profits a bit but it's still going to be profitable in the end so what are some ways that we like to think of this strategy here at that on the next slide the very first thing i want to cover again is that when we're calculating the break evens for any diagonal spread or calendar spread for that matter it's really hard to calculate because of the fact that we're dealing with these different expirations so when we're dealing with these different expirations particularly in july and may in this example the july expiration cycle is going to

change differently with a change in implied volatility if i see a one percent implied volatility increase or decrease the july options are going to be changed a little bit differently than the may options would be and for that reason we can't really ever know what our breakeven is even if we're at this stock price right here at the may expiration it's really important to realize that yes this may option would expire worthless if it was out of the money as it is here but we are still long an option in july so we would be

long a naked option at that point if we let this one expire and we didn't deploy another one we'd be long this this call here in july and we would never really know where the implied volatility would be i can't tell you right now where implied volatility will be at the may expiration cycle for july so it's hard to calculate the break evens accurately and if there's a huge massive spike in implied volatility or if implied volatility comes down even further my break even would be different in both scenarios so we don't really look to

calculate the break even but we are very comfortable with the debit we paid because that will be our max loss we can't lose more than the debit we paid in this particular situation unless we're dealing with the volatility product but we'll get into that in just a bit so the iv factor here the iv profit will be more rare and again that just goes to show the hedge against this strategy that usually takes place so unlike an iv profit from a poor man's covered put where when we're directionally correct we usually tend to see implied

volatility increase because when we're using a poor man's covered put we want the stock price to go down which usually also results in an increase in implied volatility but here iv profit will be more rare this is more of a directional play using less capital than a covered call because when we're directionally correct we usually will see implied volatility decrease a little bit it's not a sure thing but that's normally what happens in a market so an iv profit will be more rare unless the stock price stays right here and we see implied volatility explode

for whatever reason we like to close this strategy for 25 to 50 percent of our debit paid since we can't really calculate the max profit because of the differing implied volatilities between expirations we usually just take the debit that we paid and add 25 or 50 to that to figure out our closing order so if i paid a thousand dollars for poor man's covered call as opposed to five thousand dollars to get long those shares and sell the call let's say i paid a thousand dollars and i want to capture 25 of my debit paid

i would look to close that spread for twelve fifty or twelve hundred fifty dollars so i bought it to open so i would sell that spread for twelve hundred fifty dollars to close and that would give me that twenty five percent of my debit paid so yesterday we talked about volatility products and how we don't trade these diagonal spreads or calendar spreads in volatility products such as vxx uvxy or the vix because each of those expirations act as their own product and when we're talking about volatility products yesterday we said how we're not going to

trade that with a poor man's covered put but it's especially important that we don't trade that in a poor man's covered call because if we think about what implied volatility really is and what tends to happen with implied volatility we don't usually see implied volatility drop to zero we usually see implied volatility explode to the upside and if we remember in this strategy i'm short a naked call so if i have a volatility product diagonal spread here and i'm long a call in one expiration and short a call in another if the volatility explodes in

that underlying i could see massive losses here because if i'm short an option and volatility explodes to the upside i could see massive losses on this option and they couldn't they wouldn't necessarily be offset by the gains on my further date at expiration so even more of a massive no when we're looking at trading poor man's covered calls poor man's covered puts or calendar spreads in volatility products especially when we're looking to add a naked call to the strategy so this has been some information for you but let's get all some let's get some takeaways

for you to wrap it up here so we do have a bullish covered call replacement strategy with a poor man's covered call like i said instead of having to buy those shares for a lot of money we can look to deploy this strategy a poor man's covered call to use less capital define our risk much better and we can have a higher return on capital because of the fact that we're not using as much capital at trade entry market volatility will usually go against the strategy so unlike a poor man's covered put where both worked

hand in hand to accelerate profits or accelerate losses the volatility factor in this strategy will act more as a hedge if we're directionally right volatility will usually contract which will bring our profits down a little bit but if we're directionally wrong implied volatility could expand which could help offset our losses setup is key just like the poor man's covered put and usually we look to cover the extrinsic value with the sale of a short option so if i'm able to calculate that i've got two dollars of extrinsic value in my long option i would look

to sell that short option for two dollars or more to put myself in a positive theta scenario and lastly if you want to see some defensive tactics for this strategy check out my three poor man's covered call adjustments and i'll include that in the description below so thanks so much for tuning in my name is mike if you've got any questions or feedback shoot me an email here or you can follow me on twitter at dotradermike we've got jim schultz coming up next from theory to practice though so stay tuned you

Related Videos

11:47

What is a Broken Wing Butterfly? | Options...

tastylive

106,011 views

16:56

How to Trade a Poor Man's Covered Call

tastylive

135,072 views

24:13

How to Trade Covered Calls Properly (The 3...

SMB Capital

283,232 views

7:38

Is This Potentially the Best Strategy For ...

tastylive

14,938 views

48:33

Poor Man's Covered Call Explained! 📈

OptionsPlay

31,684 views

15:31

Vertical Put Credit Spread Tutorial | Opti...

tastylive

115,527 views

12:35

The Secret to Faster Cash Flow from Covere...

SMB Capital

118,906 views

10:12

What is a Jade Lizard Strategy? | Options ...

tastylive

61,989 views

13:13

Trading The Poor Man's Covered Call in 3 C...

tastylive

12,671 views

17:34

Top 3 Options Trading Strategies for Small...

SMB Capital

451,111 views

14:59

Avoid Locking in Losses When Rolling Options

tastylive

79,452 views

5:45

How To Do A Poor Man's Covered Call Option...

Brad Finn

6,290 views

12:58

Avoid this Covered Call Mistake (Guarantee...

projectfinance

86,470 views

19:27

Poor Man’s Covered Call better than LEAPS ...

Invest with Henry

23,789 views

13:16

What is a Poor Man's Covered Put? | Option...

tastylive

42,323 views

11:31

What is a Short Strangle & How do I Trade it?

tastylive

139,964 views

14:56

3 Important Concepts Options Traders Shoul...

tastylive

93,431 views

15:47

Buy Debit Spreads For Less Than Intrinsic ...

tastylive

43,914 views

15:43

Wider Options Spreads: 3 Benefits | Option...

tastylive

85,096 views

17:43

Best Short Strangle Adjustments: 3 Short S...

tastylive

148,054 views