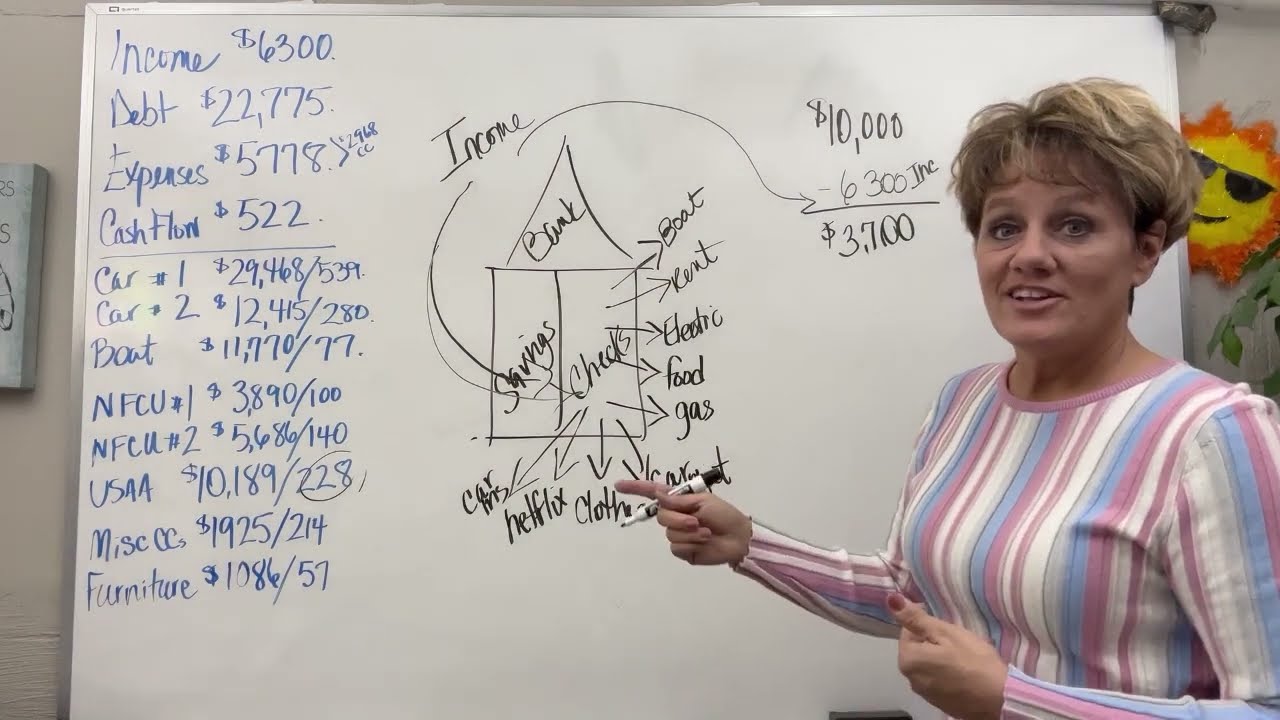

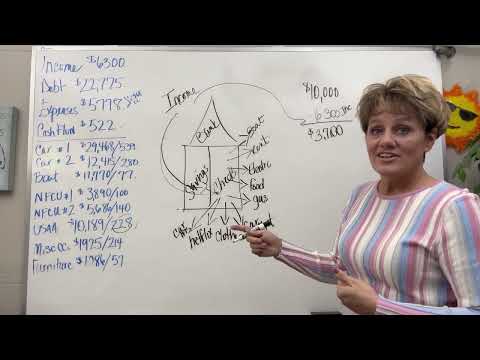

hello and welcome back to my channel I am Christy van with fantastic finances and I teach people how to get out of debt very very quickly using velocity banking that's exactly what we're going to be talking about today I have a military family that I wish I could go into the story of how I know this family they know who they are and they are so precious to my soul I just feel like that the least I can do is to give them a strategy to get out of this debt very very quickly but this will just be part one for them because I want to show them the strategy and the concept in general so that when we get into the numbers in the next video then they will have an idea of what I'm even talking about because I'm sure they don't know we are going to make 2023 a wonderful year for them financially I feel it and I know it and let's begin so when we talk about velocity banking we are talking about using your money like you've probably never experienced before you've never heard before the whole concept is to keep your money working for you instead of working for the bank we turn 16 and we get a job and the first thing that you know our parents tell us is hey you got to go get a checking account you got to get a savings account because you know now they do direct deposits right into your accounts the bank loves that because every time you make a deposit into a checking or a savings you are making a deposit into their finances and they appreciate you I'm sure and that's why they give you that . 0152 percent that they give you back when you have money in their savings and if you have a high yield check-in account you might get point one two three four back right so that's how they show appreciation for you keeping those deposits coming into their bank but we want to stop that we want our money to work for us we don't just throw it out into a payment and let it go into Never Never Land and we never said it again right no we want the money to come back we want the money to work for us and you learn to control your debt so that it doesn't control you anymore and that brings us Financial Peace when you get your account at the bank and the first thing that they usually have you do is they will have you set up a savings account right almost everywhere needs you to have a savings account then you can get you a checking okay so with the checking account that's where we pay our bills out right okay so here's your income and you automatically say hey the income goes into the bank right so when your income goes into the bank and it sits there uh this is where the bank is making money off of your deposits then after your money is in the bank you always have bills to pay so we might pay our rent out of the checking we might pay our electric out of the checking we'll pay our food we'll pay our gas we probably have a car payment we buy clothes we pay for Netflix so all subscriptions we pay our car insurance what else do we pay everything that we do comes out of this checking account right because we let our money go in and then everything comes out from there right so this is what we want to stop because when your money goes and just sits in a checking account it is doing nothing for you it is not making you money it's not saving you money it's doing nothing for you so the velocity strategy is is if you have a credit card why wouldn't you take and pay yourself by putting this income into your credit card so if you have a credit card and it's got ten thousand dollars on it and you're paying 21 interest and that's twenty one hundred dollars a year now this is simple interest okay so simple interest means that you will take the amount of Interest on the balance that you currently have so if this is a twelve thousand dollar credit card and you only have a ten thousand dollar balance and you only pay the interest on what you're actually using unlike this here your boat payment or your car payment that you will make 539 dollar payment on this amount until every last dime of that has gone to 539 dollars so if you are paying your car payments out of this checking account where does it go well it goes into the bank into this loan right and it's gone I mean can you go say hey um I made that 539 dollar payment uh but I'm gonna need 400 of that back so could you like you know pick up the phone and call and say that no you can't now once you throw a payment out it's gone right whether it be a mortgage car payments whatever is that the way it is with your credit card a lot of people think it is credit card is not debt credit card should be your new checking account and let me show you how okay now remember credit cards and lines of credit are a simple interest your only charge for the balance that you're actually using here's where velocity starts you have the ten thousand dollar credit card what if with your income the sixty three hundred dollars what if you were to put that into your line of credit or your credit card now this USAA which is the example I'm going to use it is at a ten thousand one hundred eighty nine dollar balance but it is attached to a checking account which means they can more than likely use it as a line of credit meaning they can transfer money into the checking account as cash as needed so that being the case the sixty three hundred dollars income instead of going here into the bank guess what it would go right here what does that do to this credit card uh this is a high balance credit card at 228 dollars a month what does it do when you come over here and you put the money into the credit card instead of throwing it in the bank well it looks like that you would take the sixty three hundred dollars income minus it off of your ten thousand right what's your credit card balance now thirty seven hundred dollars did you go get another job did you stop eating out did you stop doing anything did you change your lifestyle what did you do that brought this balance of this ten thousand dollars down to thirty seven hundred dollars you just put your income in a different place you didn't park it in a checking account so immediately you're saying well I have expenses and yes you have expenses so what would we do you have 5778 dollars in expenses in this example so throughout the month on the first you'll pay your electric bill on the third you'll pay your water bill on the fifth you'll go to the grocery store on the six you'll buy gas slowly throughout the month these expenses start coming back in but we're going to ride them in so 57. 78 right no because the 5778 includes this 228 right here and that's gone you know why that payment's gone is because when that income went in it satisfied the payment you don't do the 57.

78 let's just do it because I am not a mathematician I can do velocity but I use calculator right so that means that we are going to be at five thousand five hundred and fifty dollars now will be our expenses so we will add the five thousand five hundred fifty dollars and expenses back for month one and then when you add that back in 92. 50 is now your balance on the credit card this amount would get charged the 21 percent then the next month you do it again you would bring your income in sixty three hundred dollars which would bring that to zero five nine and 29. 50 is now your balance on your credit card right so what do you do again you're going to have those expenses again so guess what you'll bring it over the 5550 you will add that back in this is expenses month two 8 500 is now your balance in your second month you went from ten thousand to eighty five hundred in two months doing nothing different all you did you you didn't change a thing about your lifestyle you just decided that you were going to put your money in a different place that works for you instead of the bank so this ten thousand is no longer a twenty one hundred dollar a year or five dollars seventy five cents a day charge what is it no now you're at 8 500 which is 17.

85 a year and about four dollars and 89 cents a day in two months you've gone from ten thousand to eighty five hundred and the interest is not going to be 4. 89 it's not going to be 5. 75 because the bank figures your interest on your average daily balance so as your balance as your balance comes down from the initial chunk of your income then it slowly goes back up through the month you're never ever getting charged on the whole eighty five hundred dollars you're just not because it's not in there it's gradually building up so you might have a day at 29.

50 you might have a day at uh three thousand you might have a day at 3 500 but it's gradually building back up so you can't say that your interest is going to be 4. 89 because you are not letting this ten thousand or this eighty five hundred sit for the entire year the 21 is for the entire year at this balance but we're not going to allow that balance to sit on that even 30 days so it's never going to be be your 4.

What are the key takeaways?

Based on the transcript, here are the key points...