Entry, Exit, and Supply Curves: Decreasing Costs

57.97k views833 WordsCopy TextShare

Marginal Revolution University

In this video, we talk about the special case of the decreasing cost industry. As output increases, ...

Video Transcript:

♪ [music] ♪ - [Alex] Today we're going to wrap up our discussion of entry, exit and supply curves by talking briefly about the fascinating case of the decreasing cost industry. What's important and interesting about decreasing cost industries is that we think that they explain clusters. If you look around the world, you'll see places like Dalton, Georgia, known as the "Carpet Capital of the World," because about 90% of the world's manufactured carpet is made in this one small town in Georgia.

Or think about Silicon Valley for computer technology or Hollywood for movies. Or how about Hangji, China where they make three to four billion toothbrushes a year in this one small town. Now what is it about Hangji, China?

Is there something special which makes this town just the ideal place in all the world to make toothbrushes? No, not at all. It's not like mining diamonds or gold.

Toothbrushes can be made anywhere. Is there anything really special about Dalton, Georgia which makes it the ideal place for making carpets? No, so why then do we see these industrial clusters?

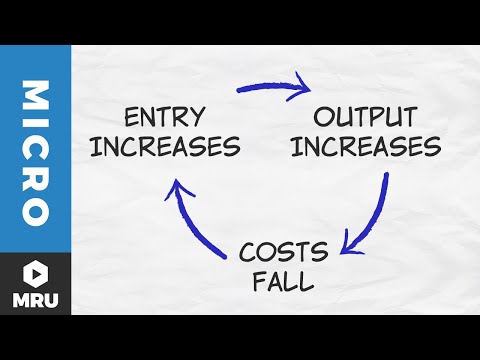

The idea is this: clusters evolve when greater output decreases local industry costs, and the best way to explain this is to give kind of a stylized history which fits the facts for many of these clusters, such as the one in Dalton, Georgia. The idea is that the first firm locates more or less randomly. However, the first firm creates some local knowledge.

In the case of Dalton, Georgia, it was knowledge about how to produce carpets. It began to train workers in specialized techniques in order to produce carpets. Some input suppliers for the backing of the carpet, for example, also began to locate in Dalton, Georgia.

So there were advantages which began to develop in Dalton, Georgia simply because one firm was there already. A second firm looking around the country and deciding where to locate then chooses to locate in Dalton, Georgia next to the first firm, because that's where the specialized inputs already exist. That's where there's some workers -- which already understand the technology -- can be more easily found.

Once the second firm does that, it contributes to the local knowledge. And the third firm looking around also now finds that costs are even lower in Dalton, Georgia than they are elsewhere, and the process continues. You can think about this as a virtuous circle.

Output increases with the first firm. That produces some decreases in costs; costs fall. That increases entry as other firms come into that area to take advantage of those lower costs.

And that increases output, and the process continues. Of course, the process doesn't continue forever. We don't find costs going to zero, but the process can continue long enough so that Dalton, Georgia gets an overwhelming advantage.

So many firms locate in Dalton, Georgia producing carpets that it would be crazy to produce carpets anywhere else, because Dalton, Georgia is where you can easily find the workers, where you can easily find the knowledge, where the suppliers understand the business. In Dalton, Georgia, even the community colleges teach the techniques needed in order to produce carpet. So these virtuous circles can generate decreasing costs.

Okay, I'm not going to say anymore about that. I'm going to leave it briefly for today. If you do want to learn more, I've provided a bonus lecture, which is from MRUniversity, on international trade, particularly on trade and external economies of scale.

I talk much more about these clusters and their influence on trade in that video, which you'll also find in your course materials. Okay, let's sum up. So in this chapter, we've really done two things.

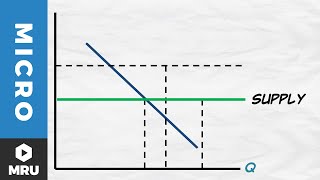

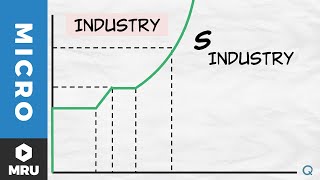

First, based upon profit maximization in a firm's cost curves, we've shown how a firm decides how much to produce and also when to enter or exit an industry. Second, based upon those production decisions, we've shown how a supply curve is built up founded upon the choices of firms in entering and exiting and how much to produce. And we've looked at three particular cases, the constant cost industry with examples of domain name registration, or spoons, or waiters, or rutabagas has a flat supply curve.

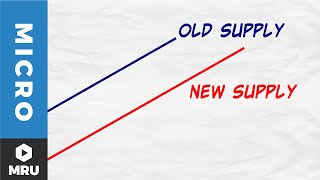

Costs don't change as output of the industry changes, and so the supply curve is flat. The increasing cost industry -- oil, steel, nuclear physicists -- costs increase -- industry cost increases as output increases -- and as a result, the supply curve increases. And finally the uncommon but important case of a decreasing cost industry where at least over some range, and in a particular location, costs can fall with increased quantity, and how this type of cost structure generates clusters, clusters like Dalton, Georgia, like Silicon Valley, and Hollywood, and so forth Okay, that's it.

Thank you. - [Narrator] If you want to test yourself, click, "Practice Questions. " Or if you're ready to move on, just click, "Next Video.

Related Videos

19:08

Trade and External Economies of Scale

Marginal Revolution University

13,108 views

10:29

Entry, Exit, and Supply Curves: Constant C...

Marginal Revolution University

85,974 views

9:06

Minimization of Total Industry Costs of Pr...

Marginal Revolution University

92,305 views

12:18

Maximizing Profit and the Average Cost Curve

Marginal Revolution University

217,333 views

34:47

1. Introduction and Supply & Demand

MIT OpenCourseWare

2,505,063 views

6:33

Entry, Exit, and Supply Curves: Increasing...

Marginal Revolution University

94,035 views

5:58

Long run supply when industry costs are in...

Khan Academy

51,595 views

50:15

8. Competition II

MIT OpenCourseWare

72,183 views

10:46

Supply and Demand Practice

Jacob Clifford

653,044 views

21:23

From Short-run to Long-run in Perfect Comp...

Jason Welker

317,324 views

1:07:33

Chapter 14: Perfect Competition - Part 1

DrAzevedoEcon

80,663 views

6:38

Long run supply curve in constant cost per...

Khan Academy

70,435 views

7:04

Maximizing Profit and the Shut Down Rule- ...

Jacob Clifford

319,026 views

6:52

Introduction to the Competitive Firm

Marginal Revolution University

221,799 views

7:14

Perfect Competition- Microeconomics 3.7

Jacob Clifford

418,764 views

12:15

What Shifts the Supply Curve?

Marginal Revolution University

583,939 views

16:55

The "Shut-down Rule" - When should a firm ...

Jason Welker

138,641 views

1:08:35

Chapter 14: Perfect Competition - Part 2

DrAzevedoEcon

37,142 views

5:17

Short-Run Costs (Part 1)- Micro Topic 3.2

Jacob Clifford

2,491,582 views

8:32

Long run average total cost curve | APⓇ Mi...

Khan Academy

120,000 views