Can you SAVE $69,000 within 24 Months? YOU CAN with this trick. #mortgage #DeathNote

2.77M views2337 WordsCopy TextShare

VANNtastic!

📞Book Me For 1-1 Coaching: https://calendly.com/vanncwi

🙌 Have My 7-Figure Coach Help You Launch ...

Video Transcript:

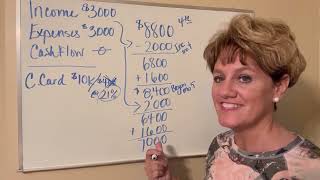

hello and welcome back to my channel I am Christy van with fantastic finances and on this channel I teach velocity banking today I wanted to talk about mortgages I am getting clients coming to me about every week now saying hey we bought a home and we have a seven percent interest charge so when I hear that I want to get down in a fetal position on the floor and just cry out loud for you and I want to explain to you when they say to you oh go get you a little four percent mortgage don't pay a 12 line of credit let's go get a little four percent mortgage I wonder if you know what they're saying a four percent mortgage what does that really equal well take four times two that equals eight right mm-hmm now add a zero to that you are paying 80 percent interest on a mortgage when you are paying four percent now I'm going to show you the difference between a 12 line of credit and a 7. 35 percent mortgage interest loan that they are giving you right now to buy your home so I'm going to do a comparison this is a five hundred thousand dollar home at 7. 35 percent now I'm doing this because I actually have a client that just did this a five hundred thousand dollar home at 7.

35 percent like I said I wanted to sit and cry with him but he wasn't even aware because we haven't been told we just don't know any better but after this video is over you're going to know better you're going to know why when I say a line of credit at 12 percent is much healthier for your finances than this baby 7. 35 percent that they tricked you into so let's talk about it if you have a ten thousand dollar line of credit and you decide hey I want to put this down on the principal of my home how much interest would that save me if I put ten thousand dollars on the principal of my home so we take the ten thousand dollars we put it on the five hundred thousand dollar home and let's just say that our payments begin July the 1st of 2023 okay so you take the ten thousand you've put it into the home and you're at four hundred and ninety thousand dollars now now remember you're still making your mortgage payments without taxes and insurance the mortgage payment on this loan is three thousand four hundred forty one dollars and forty six cents a month it's just a baby payment but you've got this huge home right so you brought the ten thousand now your home balance is at four hundred and ninety thousand what if you just decided to go ahead and make the payments on that mortgage and just see how long that took you to get to 490 000. well if you paid your payments for 23 months to June 1st 2025 you are going to be at four hundred and ninety thousand dollar balance approximately so it took you 23 months to get there making 3441 in payments every month right but how much interest did you pay to pay that 23 months so if you take the 10 000 and you put it directly on the 500 000 home when is it four hundred and ninety thousand dollars today July the 1st 2023 win your first mortgage payment is due you took the ten thousand you put it on your loan you're now at four hundred and ninety thousand dollars and it didn't take you 23 months to do it but how much interest did you pay on this I mean this is a 12 line of credit right let's see so ten thousand times twelve percent equals what twelve hundred dollars right now remember that's a year this is simple interest so ten thousand times twelve percent is twelve hundred dollars a year now what if you said well I'm not even going to pay on this I'm just going to leave that sitting at 10 000.

I'll just pay the interest every month and yeah it's like a hundred dollars a month right so if you divide 1200 by 12 months you're going to get a hundred dollars yeah I don't even care I'll just I'll just leave it sitting there or you could take your income of ten thousand dollars this person makes ten thousand dollars in income has eight thousand dollars in expenses he could say you know what I'm just going to use this line of credit as my checking account and I'm gonna put my ten thousand dollars in here well what did that do to your balance as soon as you put in your income exactly what is the payment on this line of credit exactly when you put in your income into a line of credit you have just satisfied that payment and how much interest is on this loan now that he has put in his ten thousand dollars zero right so yes his expenses could come out of that now he could pay his expenses which is eight thousand dollars a month use this account as his checking account his income goes in his expenses come out he has put ten thousand dollars on his mortgage and it did not cost him another payment to do so now let's talk about what happened over here with the 23 months that you paid on the mortgage remember it took you 23 months just to get to 490 000. here you got there in one day and if you decided not to pay it you've paid twelve hundred dollars a year right in interest if you let this run through June of 2025 you are going to pay sixty nine thousand at two hundred and thirty dollars in interest alone think about that 23 months of these three thousand four hundred forty one dollar payments three thousand of that is going to buy the bank a house it is not going to pay for your home your little four hundred dollars here that's all that's going into your home twenty nine thousand two hundred and thirty dollars oh you paid 79 000 Plus in payments for 23 months but 69 of that plus went to the bank not to your home do you know that if you let this loan run out for 30 years that you're going to pay one million two hundred thirty eight thousand nine hundred and twenty four dollars in payments do you know that you're going to pay 738 924 dollars in interest alone how many homes did you just buy the bank exactly you paid for the bank's home first you paid for the bank a home and almost a half just to get your five hundred thousand dollar home over here you saved yourself 23 months you actually cut 23 months off of this mortgage you actually saved yourself sixty nine thousand two hundred and thirty dollars in interest in 23 months all in doing one ten thousand dollar chunk if you don't believe me pull up a Carl's mortgage calculator or any mortgage calculator put in the numbers 500 000 at 7. 35 percent and see if I'm wrong no payments here baby interest if you do velocity banking right you'll pay very very little interest at making ten thousand dollars a month and let me tell you what's even worse on top of this 69 000 for 23 months is when you get to about 48 months if that far you're gonna start getting letters from your bank that holds your mortgage and they're going to say hey you've done real good on making your payments for 48 months we want to give you twenty five thousand dollars of equity in your home why don't you refinance and if you refinance we'll even take a percent we'll knock you down to six percent we're gonna do you a favor do you know what they just did if you refinance you are paying this all over again it's a trick you already bought them a home in the first four years this is just 23 months 23 months of interest that could be in your pocket this hard-earned money for you need to support your family you just supported the bank and their family this could have been in your pocket and they'll do it to you again if you refinance that home so you have to make a decision am I going to adult up and decide hey wait a minute what there's no excuses after seeing this video I don't even care if you got a 2.

35 percent mortgage you are still getting hit with interest that you do not deserve this little trick right here I've taken at a 12 percent oh they'll tell you all day long I can't tell you how many clients in a week I talk to that tell me they went into the bank to get a line of credit and the line of credits are usually like nine percent right now in the high nine percent and then when they asked for a line they will try to throw them in a loan every single time and what do they say you don't want no nine percent line we can give you this loan over here for five percent right because that's amortized too just like the mortgage all of that interest is front loaded to hit you so that you have to pay the bank first then as it trickles down you get to add a little bit more to pay for your motorcycle your car your home with a mortgage when you get to the 15-year Mark now if you're in a 30-year and you get by the refi and you don't do it and you keep struggling on through in year 15 you're going to start breaking even with your payments so if you're paying a three thousand dollar payment on a mortgage in 15 years about 1500 of that is now going to your home and 1500 of that is still going to the bank I get angered when I hear that our young people in America are getting long to seven percent mortgages right now seven percent literally highway robbery it's been going on since 1929. and now you know how to fix the problem you have to go get you a line of credit I don't care if it's at 18 you're going to beat this because 7 times 2 is 14 add a 0 to that 140 percent this one's paying over 140 percent because they're at 7.

Related Videos

29:26

This WILL CHANGE Your Mindset On MONEY. $7...

VANNtastic!

78,975 views

7:46

Home Equity Line of Credit - Dave Ramsey Rant

The Ramsey Show Highlights

1,363,338 views

12:18

How To Pay Off A Credit Card with -0- Cash...

VANNtastic!

2,171,211 views

23:56

Velocity Banking - The Truth about Paying ...

School of Personal Finance

678,551 views

14:25

It’s Over: Trump ‘Purposely’ Crashing The ...

Graham Stephan

722,566 views

14:54

Trump Spins After Musk & Rubio Blowup, Pen...

Jimmy Kimmel Live

2,197,026 views

3:33:33

Just Listen! Frequency Of God 1111 Hz: Une...

Frequency Harmony

3,476,211 views

17:29

Elon Musk exposes why Democrats don’t want...

Fox Business

4,451,149 views

19:49

How to Turn Your Home Equity into Monthly ...

Commercial Property Advisors

961,494 views

16:16

Paying off $30k in debt made EASY with the...

VANNtastic!

859,021 views

17:34

BREAKING NEWS: JD Vance, Pete Hegseth, And...

Forbes Breaking News

3,254,151 views

9:21

Does It Make Sense To Pay Off My Mortgage?

The Ramsey Show Highlights

492,195 views

12:04

Karoline Leavitt Unleashes FURY on Ilhan O...

Priscila Luz

1,023,517 views

1:30:10

20 Trump Supporters Take on 1 Progressive ...

Jubilee

2,643,427 views

18:50

How to get rid of your Visceral Fat in 30 ...

Doug Campbell

1,066,428 views

5:29

MUST WATCH: Byron Donalds Absolutely Light...

Forbes Breaking News

2,260,850 views

20:18

8 GOOD REASONS to File for Social Security...

Financial Fast Lane

2,013,043 views

20:22

How Vail Destroyed Skiing

More Perfect Union

1,089,073 views

9:21

Where Do I Start When I’m Paid Biweekly?? ...

VANNtastic!

65,544 views

24:23

A Home Loan Where NO PAYMENTS are Required...

Get Rich Education

162,822 views