Free Cash Flow: Back to Basics

128.61k views7082 WordsCopy TextShare

Aswath Damodaran

In every market correction, investors discover old truths, and this one has been no different. Not o...

Video Transcript:

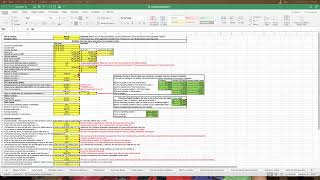

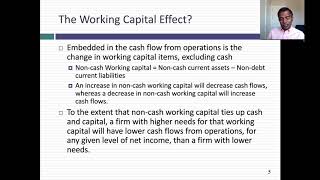

hi welcome back today we're going to talk about free cash flows in fact it's a testament to the times that it's been a long time since we've actually talked about free cash flows but a market correction like an impending execution focuses the mind when you think about losing your investment Capital all of a sudden you come back to your census notice that there's been a lot less talk about growing users and subscribers and revenue growth and much more about earnings this year a greater talk of free cash flows companies are talking about it investors are talking about it now part of me feels Vindicated I'm as an intrinsic value believer I've always talked about cash flows but I'm a little wary about this current talk about free cash flow because I'm not quite sure what people are talking about in fact I would argue that the first thing we need to do is nail down what we mean by free cash flow because the definitions that are floating around Boggle the mind second we need to get some perspective what if free cash flows look like I mean we have a sense of what earnings look like but what do free cash flows look like so with those missions in mind let me start with free cash flow I've often said in my classes that there is no more dangerous term in finance and free cash flow sounds like hyperbole but the reason I say that is I've seen analysts use free cash flow to mean whatever they want it to mean I've seen people say look we had depreciation and amortization back to earnings you get free free cash flow the fact that you've stopped at an intermediate stop doesn't seem to make them give them pause of course in companies especially young companies have carried this to an art form with adjusted ebitda to begin with ebitda by itself is not a free cash flow why isn't it free because it's before taxes and before capex and before working capital needs but even if you took appetizer cash flow the way these adjustments are made again push the limits of what what free cash flow is supposed to measure you'll see companies adding back stock based compensation why we'll come back and look at the logic which actually makes no sense but the pro the point I'm trying to make is if you're in a debate with somebody about free cash flow the first thing you need to nail down is whether your definition of free cash flow and their definition of free cash flow converges so let's start by looking at what free cash flow is and how it's measured before you start to think about free cash flows you need to specify to whom you say what are you talking about too if you think about a firm firm can raise capital from Equity investors or from lenders whether it's a private or a public firm the only two ways you can raise capital there are two ways you can Define free cash flow one is free cash flows to just Equity investors that's a cash flow left over after every other need has been met and debt payments have been covered that's free cash flow Equity but there's another measure of free cash flow that's floating around that sometimes confuses people it's called free cash flow to the firm let me give you my intuitive understanding what free cash flow to the firm is free cash flows Equity measured cash flows that Equity investors get from The Firm free cash flows a firm measure the cash flows that both Equity investors and lenders get from The Firm so what kind of cash flows do lenders get but they get interest payments they get debt repayments and to the degree that you take on new debt you might be able to offset some of those those debt repayments but it's cash flows to debt and cash flows to equity combined is a free cash flow now later we'll come back and talk about why we have two measures of free cash flow but it's let's be clear free cash flow to equity measures the cap cash flow left over for just the equity investors free cash to the firm is a pre-debt cash flow it's a cash flow that all claim holders get stock mechanics to estimate free cash flow equity here's what you start with you start with earnings to equity investors net income then you add back non-cash expenses depreciation and amortization the most common of those but there might be other non-cash expenses and then you subtract out what you put back into the firm completely discretion you can choose not to but if you put money back into Capital expenditures cash acquisitions and of course if you invest money in working capital your working capital increases that change in non-cash working capital increase becomes a reduction in cash flows net income you add back depreciation amortization you subtract capex you subtract our change in working capital you've come up with a measure of free cash flow before you factored in cash flows to and from debt so what are you talking about well if you repay that that's a cash outflow so you need to net it out and if you take on new debt that's a cash inflow the net debt cash flow when you take it out of the free cash flow gives you a free cash flow to equity for Equity investors I think of it as potential dividend this is potential dividend because it's cash left over after you've met every conceivable need companies can choose to pay it out as a dividend they can choose to buy back stock or they can just choose to hold on to the cash and increase their cash balance that's free cash flow equity what about free cash for the firm well if you compare the free cash for the firm to free cash Equity calculations noting that my starting point is different rather than start with net income I start with operating income or earnings before interest in taxes now you can go accounting on me and finesse the two but to me the two are two expressions for the same number that you're trying to estimate you start with operating income why because net income is after interest expenses and free cash for the firm as we said is cash flows before debt payments so you start with operating income then you act like you pay taxes on that operate income notice the word I used act I know you don't pay taxes on operating income you pay taxes on taxable income but you act like you have no interest expenses and you're paying taxes on your operating income it's a hypothetical tax you net that tax out you come up with after tax operating income now different Services different authors use different terms for it McKinsey for instance call this no plait but it's after tax operating income and whatever guys you decide to put it in then you subtract out exactly the same reinvestment we talked about in the free cash flow Equity context you add back depreciation amortization you subtract capex in fact capex minus depreciation I call Net capex and change working capital that becomes the reinvestment what you're left with is the free cash for the firm notice that there are no dead inflows and debt outflows because we're looking at a pre-dead cash flow cash flows to and from debt don't get counted saying what is the free cash flow to the firm measure at one level it measures cash flows to all claim holders in The Firm another way to think about the free cash flow of the firm is this is the cash flow you'd have had if you'd be in an all Equity funded company we've chosen not to borrow money that's why some people call this an unlevered cash flow but basically you're saying if I had no debt what would my cash flows look like now with that structure let's talk about using this to actually compute free cash flow to equity and free cash to the firm for a company I'm going to use Microsoft as my example and I'm using that 2021 fiscal year numbers to compute free cash flows equity now if you're Computing free cash flows Equity every number you need is on One financial statement you know which one right go to the statement of cash flows everything you need will be there I'm going to use Microsoft statement of cash flows to compute the free cash flow equity I'm going to start with net income so right from the top 61. 271 billion dollars I'm going to add back depreciation and amortization the 11 08 686 million that you see there I'm also going to add back the the not the the gains that I showed in Investments that's a non-cash gate so when you add back these expenses you basically also have to add back any other non-cash items and because I counted these gains and then non-cash I'm taking them out of the process to the minus 1249 is my removing gains because they're not cash gains you're saying what about stock based compensation I'm going to come back and talk a lot more about this but to me stock based compensation is not a non-cash expense it's not like depreciation amortization it's more of an in-kind expense in other words you're using Equity to pay somebody you're going to treat it very differently from depreciation so I'm going to ignore it for my free cash flow Equity calculation then if you look at all of the other items below the all of these Inside the Box those are all short-term items accounts receivable accounts payable and if in fact if I consolidate them I get a number one I basically get an an increase in working capital 1. 086 billion and when working capital goes up it decreases cash flow so I'm subtracting out the one up 1.

086 billion so that takes care of the items the operating cash flows let me move to the investing cash flows there are two items in the investing cash flows I'm going to count it the first is capital expenditures because for obvious reason that's a cash outflow the addition to plant neck weapon but I'm also going to count in cash Acquisitions you're saying but Acquisitions are not capex says who Acquisitions to me are gigantic capex I net those out I come up with free cash flows before I factored in debt repayments and debt issuances at least in this period all that Microsoft did was repaid 5. 5 billion debt it took on no new debt so debt repair raised to zero debt repaid is 5. 5 billion and net that out you come up with a free cashword Equity after that of 36 397 million now actually you can if you find this too involved too many calculations I've taken all of the items from Bill from between the net income and the free cash flow Equity prior to that and Consolidated them and call them reinvestment so reinvestment includes net capex capex minus depreciation includes cash Acquisitions includes change in working capital the nice thing about consolidating it is basically allows you to tell a story about what Microsoft did in 2021 and um it in I'm sorry in 2021 it had net income of 61.

2 billion it reinvested 19. 4 billion got free cash flow Equity before that 41. 9 billion debt removed 5.

5 billion leaving them with free cash flow Equity after that payments of 36. 4 billion that's a free cash flow Equity calculation incidentally there's one item here this tiny foreign exchange item which you can see jumps back and forth I could have brought it in it was just too small to even worry you know to factor in but if you if you have a foreign exchange item consistently showing up across time you can also bring that into the free cash flow equity say what about free cash flow to compute free cash to the firm I have to leave the statement of cash flows to get two items one is operating income which will be on the income statement the other is an effective tax rate which should also be in the income statement for those who have forgotten effective tax rates it's just the taxes payable divided by taxable income in the income statement in 2021 Microsoft had an effective tax rate of 13. 83 percent its operating income is 69.

9 billion so here's what I'm going to do I'm going to act like I pay that effective tax rate on my operating income again it's acting I don't pay taxes on operating income I'm going to act like I do the taxes I get is 9. 7 billion and net that out I get after tax operate income of 60. 2 billion then the reinvestment I subtract out is exactly the same reinvestment I talked about in the context of net income 19.

37 billion which leaves me with the free cash flow to the firm of 40. 9 billion since Microsoft is a company with a relatively little debt the free cash flow equity and free cash for the firm are pretty close another way of presenting the numbers you saw on that page is an a waterfall chart basically you start with your net income for free cash flow Equity you net out the reinvestment you net out the debt payment you come up with free cash flow equity for free cash with the firm you start with operating income you net out the taxes you will have to pay hypothetically on that operating income and the reinvestment you come up with free cash for the firm so those are the mechanics let's talk about how free cash flows get used there are three contexts in which you're going to see free cash flows used one is to explain what happened last year you're purely interested in explanatory power which is what did the company do last year so you're going to be able to use the free cash flows to see where cash came from and where it went in fact you're doing what accountants doing the statement of cash flows the second use of free cash flow is in valuation where you project out future free cash flows to be able to Value business the third place you're going to see free cash flows used is in pricing you see what does that mean well you know how people price companies right they compute a pricing multiple p e ratios Price to Book EV tablet they compare that across companies how do free cash flows help rather than use price earnings ratios you might use price to free cash flow equity for some reason there's some analysts some I think using free cash flow will give them better pricing we'll come back and see whether that's true you say why distinguish between the missions because the way you compute free cash flows can be very different depending on your mission if your objective is to just explain the past you should stay with the past so if you ask me what happened at Microsoft in 2021 I'm going to show you the table that I just showed with the actual cash flows in 2021. the acquisition they made the you know this so essentially my objective is to explain what the company did in 2021.

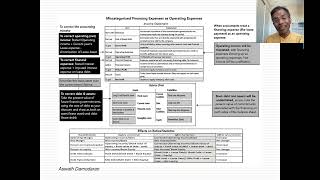

in fact you can learn a great deal about the health of a company during a year by looking at its cash flows so you've all seen accounting statements of cash flows accountants also try to do that but their mission is very different the statement of cash flows doesn't try to give you free cash flows to equity tries to explain what happened to cash during the course there how much the cash balance change the information you need for free cash flows to equity is in there so here's how I think about free cash flows to equity and how they're useful earlier I described free cash flowist Equity as potential dividend I said this is what you can afford to pay out as a company in the statement of cash flows companies also report what they are actually returned investors either in dividends regular or special or in the form of stock BuyBacks and we have stock issuances if you want you can net them out against the BuyBacks so potential dividends of actual cash return now you might find that rare company which pays out exactly what it could afford to every year a residual cash flow policy I don't think I've ever seen one that does us for whatever reason companies either pay too little or paid too much for the most part in other words some companies hold back cash they return less cash than they have available as free cash trade Equity other companies return more cash than they can and each has consequences if the cash you return is less than your free cash flow Equity at 100 million free cash flow Equity you chose to return 70 million that difference of 30 million you know where it's going to go don't say retain earnings wrong side of the balance sheet it's going to go into your cash balance a company that consistently returns less cash than it can afford to is going to build up a cash balance how do you see how companies end up with 50 100 or 200 billion dollar cash balances it's not Mana from Heaven it's a direct consequence of year after year holding back cash you could have returned you can also return more cash than ever available as free cash flow Equity if a hundred million free cash flow Equity you might choose to return 120 million again for good reasons or bad reasons a good reason might be that your free cash Road Equity jumps around you're smoothing out what you return to reflect what you make in a typical year the reciprocal or a commodity company you might smooth things out and return cash that's actually greater than your free cashword equity in a down year and return Less in and up here it could also be there because you're involved in metooism what does that mean you're paying dividends because everybody else is paying dividends you're buying back stock because you've always bought back stock or everybody else is buying back stock if you return more than your free cash flow Equity you have a bit of a hold right and here's how you might fill the hole if you have cash balances from past periods you might use it to cover the difference so in this example that I just gave you return 120 million you're only 100 100 million free cash flow Equity you can draw down your existing cash balance by 20 million and if you have enough cash you could do this for a long time but if you return so much cash that you don't have enough in your cash balance to cover it you know what you'll have to do you'll have to raise fresh Equity that makes no sense right you say why would I raise Equity to pay dividends and buy back stock because you get locked into doing something and you're afraid to change it so if you return more than you have available as free cash flow Equity either draw down the cash validation new equity now of course there are some companies with the free cash flow Equity is going to be negative why either because you're losing money or because you reinvested large amounts everybody returns no cash okay already in a deficit right so it has to do the same things it either has drawdown in existing cash balance or raise new Equity we'll come back and talk a little bit more about that in the context of free cash flow to the firm remember free cash for the firm is the cash flow you're available to service not just what Equity investors would need but also what you promised lenders from the free cash flow to the firm the first claim is going to come from the lenders you've got to make interest payments and of course you have to repay that you've got to repay the debt you might raise fresh debt so you covered debt cash flows from the free cash of the firm you also get the free cash flow Equity that we talked about from which you have dividends and BuyBacks and of course if you collectively return less cash than you have available to lenders and Equity investors that if available is free cash to the firm again you're going to see an increase in cash balance if it's less than your what you've returned then of course your cash balance decreases or you've got to raise fresh capital from equity and debt so there's an advantage to looking at the past but they're using a very strict definition of free cash sort of equity and firm you're looking at what happened that year now when you talk about using free cash flows and valuation your task is different right you might estimate the free cash flows from last year but you're doing it not because your interest in lost it has no relevance to Value today but because you want the base Year from which to build off your forecast for the future it's a very different mission so when you compute free cash or equity and free cash to the firm for valuation you're looking forward you're saying what should my base year look like so I get the best estimates for the future a little bit of attention you're saying well which one should I use when I when I do valuation depends again whether you want to Value just the equity in a firm where you can take free cash flows to equity project free cash flows equity and discount them at the cost of equity and value the equity over developing the entire business we take free cash to the firm but if that's a cash flow you're discounting you're going to discount it back not at the cost of equity but at a weighted average of your cost of equity and cost debt cost of capital and you'll come up with the value of the operating assets then you can add cache subtract out and do all the cleaning up but you got to make the choice up front you can't just say free cash flow and not tell me which of these two approaches you're using so let's talk a little bit about what you might do differently if you're Computing free cash flow the free cash flow either to equity or the firm for a base year remember when you looked at last year's cash flows there are there are items that you pulled off the statement of cash flows in fact one item you saw for Microsoft was a gain that they made a one-time cake which pushed up there and compared with non-cash now that is a unusual item it's not grouper every year so if you have unusual or one-time items take them out of the calculation because if you build them into the base here you risk forecasting something that's not going to be there second when we looked at 2021 numbers for Microsoft we looked at the actual change in non-cash working capital the actual capex the actual cash acquisitions but 2021 might have been an unusual year working capital is the most volatile of all items some years it goes up some years it goes down using last year's change in working capital might give you a very bad indication of what's going to happen in the future the case of Microsoft one thing I think might be worth doing is replacing last year's change in working capital with some variant that's more normalized smooth out I'm going to show you the variant that I'm going to use if last year you had a big acquisition you don't think the company is going to do it more than once every four or five years again you might have to normalize numbers so when you're estimating free cash flows is a basis for forecasting you have a lot more discretion in what you do to those numbers some numbers you might normalize some you might leave as is some you might remove altogether now let me talk about stock based compensation to me one of the biggest malpractices in valuation is what we do with stock based compensation what companies do what analysts do here's the logic they use I'm trying to compute cash flows talk based compensation is not a cash flow Zone when I add it back that's convenient but here's what it's missing let's assume I add back stock based compensation I'm going to increase my free cash flows to equity in The Firm right and let's say project out those cash future cash flows based on that higher base think of what I'm implicitly assuming I'm implicitly assuming that I will not have compensate employees in the future because I'm acting like that compensation is not an expense it's an in-kind expense I'm giving a share of My Equity as an equity investor it makes my Equity less valuable if you keep doing that and by the same logic remember I added back cash-based Acquisitions why does cash-based Acquisitions if you do an acquisition you pay with shares you're effectively using my equity and if you plan to keep doing it I want to build that in so don't fall for the trick of adding back stock based compensation and ignoring stock-based Acquisitions treat them as if they're cash flows on taxes when I did Microsoft's free cash for the firm last year I used the actual effective tax rate but as we all know tax rates swing around they are high in some years low in others using a year in which your tax rate is unusually low or high can give you a very misleading base from which to make forecasting finally there is this issue of accountants being inconsistent about what they call operating expense and what they call capex let's face it r d is a capex but accountants treated as an operating expense by itself it doesn't change your free cash flow Equity but it can change your views about how profitable your company is and how much it reinvests Microsoft for instance in 2021 the fiscal year 2021 at 20. 7 billion dollars in r d that was expensed it lowered their net income but in fact it was one of the biggest Capital expenditures so just to show you what would be different if I were Computing a free cash with equity for Microsoft for forecasting and valuation as opposed to doing it just for last year to explain what they did last year first I would capitalize r d I've kind of done used a shortcut you added the entire r d but there's a little more involved exercise you'd go through we'll push up my net income and I do that when I capitalize r d there will be an amortization to bring in but here are the other changes I would make last year working capital was actually a cash it was a cash outflow why because working capital went up that's unusually Microsoft Microsoft is a history of negative non-cash working capital whereas it grows it actually makes becomes more negative so here's what I did instead of using last year's change in working capitals I looked at working capital as a percentage of revenues over the last decade it's minus 10. 18 and estimated what the change would have been last year based on that percentage so what it does is it makes working capital go from being a cash outflow to a cash inflow because that's the type of business Microsoft is at now for the capex notice I've added the r d as I said it's a very simplistic adjustment where I've added the r d to both my net income and my capex and that's why it doesn't affect my free cash flows the net effect is zero and for Acquisitions I've brought in both cash and stock based acquisition so it's not just the cash acquisition I've included an acquisition of a company called Nuance that Microsoft bought in 2021 for 19 billion plus but paid forward still what I'm trying to say is the free cash flows to equity that I get with these normalized values is the base that I'm going to use to project out future cash flows it's 21.

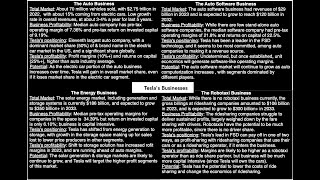

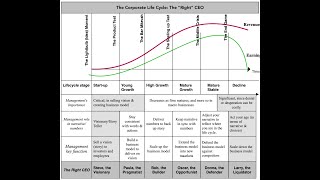

6 billion not the actual free cash flow equity if your question is am I allowed to do all this stuff when you're doing valuation you get the discretion the freedom to replace numbers that you don't think are numbers that you would see every year going forward finally let's talk about pricing as I said in pricing you scale the market price to something so you can compare across companies price earnings ratios is scaling market price to net income Evita beta you're scaling the Enterprise Value which is a market value of operating assets to ebitda now there are some analysts argue that you shouldn't trust accounting earnings and I don't trust accounting earnings but they think instead of accounting earnings would be better to use free cash flow I'm not so sure about that but what they are arguing for instead of using price earnings ratios why don't we look at price to free cash flow Equity multiples why don't we look at EV to free cash flow to the firm sounds reasonable right the logic is cash flows are better than earnings and that logic sounds compelling but we'll see in pricing the logic doesn't always hold up because you're looking at last year's free cash flow equity and last year's free cash for the firm and the question is are they better indicators how how healthy and profitable your furnace so let's get to get some perspective on free cash flow what I have in this graph is one of my favorite you've seen this before a corporate lifecycle where I graph out what happens to companies over time startups young companies middle-aged companies declining companies dying companies and what I've done here is is looked at the items that go into free cash with Equity at each stage so let me cut to the chase you should expect to see negative free cash flows to equity at Young companies why because often you start with the loss the business model is still evolving you have huge reinvestments because you want to grow and you take a loss and you put reinvestments in you get huge negative free cash flows Equity it's called cash but it's a feature not a bug and you cover it with Equity issuances why because you don't have a cash balance available to cover those those cash flows as you grow and your business model takes form you start to make money but you will start to make money well before your free cash flow Equity turns positive and here's why you start to make money because you're growing your business model is evolving but remember you're still growing you're reinvesting a lot so often in the early years your income can be positive but your free cash flow Equity can continue to be negative as your growth starts to level off and that's the key as your growth starts to become lower your reinvestment needs drop off your free cash flow Equity will turn positive and it'll actually grow faster than your net income as a mature company it'll level off when you become a mature company and then when you're going to decline your earnings are going to decline much more quickly because in Decline you're shrinking as a company you might divest your assets you might actually have this strange phenomena of free cash flows Equity running ahead of earnings as you go to liquidation mode you tell me where you are in the life cycle I can kind of guess what kind of free cash flows Equity you should have I used two things to illustrate this point one is I've taken one of my favorite companies Tesla and graphed out their net income and free cash flow Equity every year since 2006. it's pretty much all the financial statement numbers I could find through 2021. you start with an obvious statement through much of its life Tesla has been a money losing company not because it's a bad company but because the young growing company with huge ambitions it's free cash flows Equity have been even more negative than its net income it finally turned the corner and profitability in 2020 it started making money but it's still a negative free cash flow equity in 2021 for the first time net income Was Not Just Not only was net income positive but so was free cash flowed equity if you're an optimist in Tesla the good news is Tesla is growing up the bad news is if you've been ascribing growth rates of 60 70 80 percent of the company it's time to stop I mean that is the downside of growing up is your growth rates will start to level off now if you look across companies is there any evidence of this phenomenon we talked about a free cash flows to equity changing his company's age here's what I did I took all U.

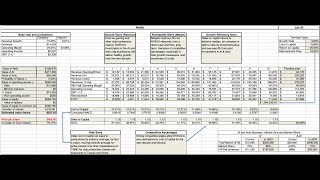

S companies and broke them down by age from youngest to oldest by deci and then I looked at net income and free cash flow equity for each of these companies start with a couple of things that jump out at you young firms are more likely to lose money than older firms I should be surprised by that both absolute and relative terms young companies are more likely to have negative free cash flows equity than older folks so what you see here is as companies age their earnings and free cash flows to equity go from negative to positive it's the natural course of being it doesn't make young companies bad and old companies good but it does mean that if your investing is focused on big positive cash flows you will end up with older more mature companies in your portfolio in fact it does show up in what these companies actually return to investors you know if you go in fact on the previous basis a couple of things I want to point to one is if you look at the youngest companies the company 73 of the youngest companies are money losing 76 percent of negative free cashless Equity those statistics improve as you mature and you see that reflect on what companies returned young companies are the least likely to pay dividends only 15 pay dividends older companies 75 pay dividends young companies buy back stock lot less frequently than older companies why because they don't have the cash flows in fact I'm surprised that 23 of the youngest companies actually buy back stock if you're trying to explain why some companies pay dividends on others don't why some companies buy back stock the answer lies in where they lie in the life cycle of course some companies do dysfunctional things but across in the aggregate at least it makes sense to expect companies that are young to pay out less than dividends and buy backless stock close with a very short discourse in pricing clear about why people prefer to price companies and value them seems simpler right dividing the price by the earnings per share to come up with the PE Ratio is a lot easier than projecting out free cash flows equity for the next 10 years and a terminal value invaluing it today people like pricing because it's simple and people like pricing because of a frame of reference what am I talking about if I came to you with a stock with a PE ratio of a hundred you probably said that's a high number that's an expensive stock tell me why why because you have a frame of reference whether that frame is right or not you're saying well I think 15 is an average if I'm paying 25 or 30 times earnings I'm paying more than I should it's an expensive stock so it's nice with pricing a frame of reference allows you to make quick judgments this is expensive this is cheap so when an lbo guy says look you know six times ebitda is cheap he's talking with a frame of reference the prom with free cash flow multiples is unlike PE ratios they haven't been around long enough we haven't seen them often enough to have a frame of reference the second is earnings are noisy right analysts can and accountants can move things around but free cash flows are even noisier because you start with the noisy earnings and then you're putting in things like capex and Acquisitions and working capital what I'm trying to say is sometimes free cash flows are a worse indicator of how well a company is doing than earnings are because of all of those additional adjustments the frame of reference though you're saying if I decide to use price to free cash or vehicle what do the numbers look like well I've tried to help you out here by taking all publicly traded firms 48 788 companies in my sample and Computing PE ratios and price to free cash flow equity for every firm so let me start with the broad statistics the median global company has a price earnings ratio of about 17 and a price to free cash flow equity ratio of about 15.

Related Videos

45:16

AI Winners, Losers and Wannabes: Valuing A...

Aswath Damodaran

115,811 views

8:18

Why Economists Hate Trump's Tariff Plan | WSJ

The Wall Street Journal

144,661 views

40:21

A Tesla Revisit: Story Twists and Turns wi...

Aswath Damodaran

49,603 views

41:50

Facebook (Meta) Lesson 2: Accounting Incon...

Aswath Damodaran

46,797 views

46:44

Facebook (Meta) Lesson 1: Corporate Govern...

Aswath Damodaran

97,805 views

1:01:30

Valuation in Four Lessons | Aswath Damodar...

Talks at Google

1,640,327 views

31:00

How The Economic Machine Works by Ray Dalio

Principles by Ray Dalio

40,686,269 views

43:27

Valuation Tools Webcast: Reading a 10K

Aswath Damodaran

125,065 views

28:48

Aswath Damodaran – Laws of Valuation: Reve...

Nordic Business Forum

1,537,849 views

1:31:29

The Value of Stories in Business | Aswath ...

Talks at Google

528,039 views

15:09

Session 8: Estimating Growth

Aswath Damodaran

157,368 views

24:07

Bloomberg Wealth: Catherine Keating

David Rubenstein

8,526 views

32:47

NVIDIA’s Valuation and AI’s Negative Sum G...

The Prof G Show – Scott Galloway

297,055 views

16:15

Session 1: Introduction to Valuation

Aswath Damodaran

2,214,582 views

1:19:04

Session 9: More on cash flows

Aswath Damodaran

17,295 views

16:50

Session 4: Equity Risk Premiums

Aswath Damodaran

359,316 views

31:01

Chapter/Session 6: Business Investing acro...

Aswath Damodaran

1,909 views

1:53:51

Uncertainty in Investing and Valuation: Wh...

Aswath Damodaran

50,943 views

13:24

Session 4: The Statement of Cash Flows

Aswath Damodaran

66,037 views

27:33

Discounted Cash Flow - How to Value a Stoc...

Learn to Invest - Investors Grow

707,410 views