How to Hedge Your Positions | Options Trading Concepts

185.58k views2399 WordsCopy TextShare

tastylive

Subscribe to our Second Channel: @tastylivetrending

Check out more options and trading videos at www...

Video Transcript:

[Music] Welcome back, everyone, to Mike and his whiteboard! My name is Mike, this is my whiteboard, and today we're going to be talking about hedging. We talked a little bit about this when I covered Delta, and we discussed Delta hedging, which is what we're going to talk about today.

But we're also going to explore some other aspects of hedging that aren't so orthodox. We'll look at some unorthodox ways of hedging our portfolio, and I think it's going to be very revelatory in that sense. So, let's get right into it, and we'll talk about the difference between just buying stock and using a covered call instead to hedge.

Because, at the end of the day, a covered call is a form of hedging stock. When we look at hedging, we're basically looking at minimizing risk. So when we're focusing on minimizing risk while discussing long stock, I've got this full circle here, which signifies direct directional risk.

If I'm just buying long stock and I'm fully exposed to that, I'm also fully exposed to that directional risk. However, if I use a covered call instead, which is buying stock and selling a call against it—both of which have differing assumptions in terms of direction—I take a chunk of that directional risk out of the equation, reducing that directional risk for me. This is great for a few reasons, and we're going to talk about that on the next slide.

When we go to the next slide, we'll discuss how we can use long stock and sell a call against it, and what that means directionally. We know that if I'm buying 100 shares of stock, let's say at $50, which would be an investment of $5,000 in a cash or IRA account, that's going to be a bullish assumption. A bullish assumption just means that I want the stock or underlying to go up.

If I buy shares of stock, for me to profit, I would sell those shares for a higher amount. So obviously, I would want that underlying to go up in price for me to do that. Instead of just buying the long shares, I can also sell a call against it.

We have to remember that a call contract—or any option contract for that matter, unless you're trading a mini—is going to represent 100 shares of long or short stock. In this case, if I'm selling a call contract at expiration, it's going to represent 100 short shares of stock. If I'm buying 100 shares at $50 and I'm selling a short call at $55—this still gives me some room to the upside to be profitable, while also collecting a credit of $1.

50, which is really $150—it has a bearish assumption. What this does is it gives me two positions that battle against each other, but my long shares will eventually outweigh that short share loss. Let's say the stock goes from $50 to $60.

I would see the profit all the way up to my short call at $55. But once the stock price reaches that $55 strike, that’s when the profits would be offset. If I have 100 long shares and 100 short shares at $55, any movement above $55 is going to be a wash.

This would still be a profitable situation, but I’m hedging my risk to the downside as well. This is something we covered in Delta, and if you missed that segment, you can find shows at the top of the section, go down to "Mike and his whiteboard," and it’ll be there. We covered how basically selling a call against shares, and we also have a segment on covered calls which went into this pretty in depth.

It basically reduces our directional risk to the downside, and also, when we’re selling a call against it, we’re increasing our probability of profit, which is really what we're trying to do here as well. If we go on to the next slide, we’ll talk about another way we can hedge. Doing covered calls is not the only way to hedge our portfolio; we can actually get pretty creative with it.

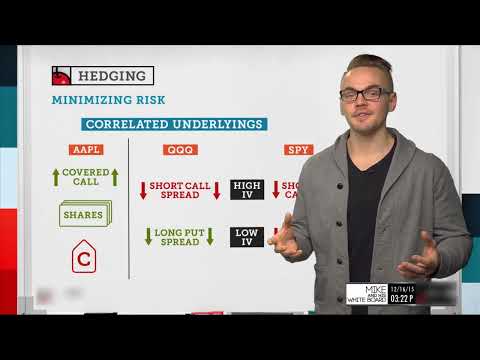

I think it really comes down to correlation and understanding it. If I have a covered call in Apple, for example, and let’s say I want to hedge some of those Deltas—maybe I'm not comfortable with having long Deltas in Apple; perhaps I want to look to neutralize those a bit—instead of doing another trade in Apple, I could look at other correlated underlyings. For example, the Q's, which have a very high correlation with Apple, could be a place to make a negative or bearish assumption in that underlying.

Let’s say I’ve got a high IV environment; I might look to sell a call spread in the Q's, which would effectively hedge my position in Apple. If, for whatever reason, my main portfolio is based on Apple stock and I'm looking to hedge it, I could use the Q's as a way to hedge it. Because at the end of the day, a covered call is a bullish assumption, while a short call spread would be a bearish assumption.

Also, if I didn’t want to look at that, I could consider the SPY. SPY and Apple have a very high correlation; Apple actually makes up a significant sector of the SPY stocks that are considered in that bucket. Perhaps instead of a call spread, if I’m not very risk averse, I could just short a call outright.

There are different ways we can do that, and even in low environments, maybe if I'm not happy with the implied volatility in the market, but I still want to hedge my position in Apple some way, maybe I'd look at a long put spread, which would pretty much be unaffected or maybe benefit from an increase in implied volatility. Or, if I just want to avoid the options in general, maybe I could short stock in SPY; so I don't have to short 100 shares of stock, maybe I could short 15 or 20 shares, which would give me a small notional value and a small hedge against my long stock in Apple. So these are different ways that we can hedge our positions, and really, it all boils down to understanding what underlyings are correlated and what we can do to be creative to hedge against our position.

Once we understand how everything works together, that gives us a better understanding of what we're doing in our portfolio as a whole. Another way we can measure hedging is going to be on the next slide, and that's what we're talking about when we talk about Delta hedging. If you missed the Delta segment, it was a previous whiteboard segment; you can definitely check it out.

What Delta hedging is, is just measuring your deltas and then using the option deltas to offset that. When we're talking about shares of stock, if I'm buying 100 shares of stock, I would have a positive 100 Delta in that underlying. Each share of stock represents one Delta.

If I've got 200 shares of stock, then I would see a positive 200 Delta. If I had short shares, it would be just the opposite. If I shorted these shares outright, I would see -200 Delta, and if I shorted these 100 shares, I would see -100 Delta.

What I can do to utilize that in my portfolio as a hedge is look at the option Delta if I'm going to, for example, create a covered call position. There are three terms here that are great to understand: we have underhedging, which is basically hedging under 100% of that Delta value. So let's say I've got 100 shares of stock at 100 Delta; an example of an underhedge would be just a standard covered call.

If I sell a call option with a 30 Delta, it would actually be a negative 30 Delta since it's bearish and I'm selling a call. Now, instead of having 100 shares or 100 Deltas of exposure, I would have 70 Deltas of exposure because I've got 100 shares of long stock but -30 Delta on my short call. Another thing I can do is create a perfect hedge.

A perfect hedge would be using multiple call contracts, for example, to perfectly hedge my scenario. So let's jump down to 200 shares. Let's say I've got 200 shares of long stock and I know that selling an at-the-money call would give me roughly -50 Delta.

To perfectly hedge that, I would need to sell four calls against it. If I've got 200 positive Deltas with my 200 shares and I sell four calls that have -50 Delta each, then my Delta should be pretty neutral, should be pretty close to zero. Lastly, what we can do is overhedge.

Let's say we're holding on to stock but we're really not comfortable with what might be happening, but for whatever reason, we still want to hold the stock. Instead of getting out of it, maybe we see some downside potential in the future. We could overhedge the position.

It's pretty rare that we would do this; normally, we would just get out, but we can always overhedge the position. So let's say I've got 100 shares of stock and I've got 100 Delta. One thing I could do is look to sell maybe three at-the-money calls.

If I sold three at-the-money calls that had -50 Delta, that would give me -150 Delta against my 100 Delta here, so I would actually have a net negative 50 Delta position in this scenario. What's really important to know is that when we're dealing with covered calls, for example, which is what we've been using in this example, if I've got 100 shares of stock, I can sell one option against it, and I won't have any additional risk. If I sell more than one option, like two options, for example, my risk is defined on my 100 shares and my short call together.

The risk can be associated with one another, but since I don't have another 100 shares that represents my short call, with my additional short call, I'm actually exposed to one naked short call. It's really important to know and remember that each option contract that we're selling must be associated with 100 shares of stock for it to be correctly correlated in terms of risk. If we don't want any additional upside risk, then we need to be mindful of the fact that 100 shares of stock is associated with one short call, and that risk will outweigh itself.

Another thing to consider when we're talking about Delta hedging is that it's not static; this is considered a form of dynamic hedging. For example, if I have 100 long shares and I sell a call against it, let's say it's an out-of-the-money call with a 30 Delta, now I've got a positive 70 Delta. Everything's fine, but if the stock price starts to move down since I sold the call out of the money, it's now going to be farther.

. . Out of the money, which means my Delta is going to be lower.

So let's say my Delta is now up, uh, 15 Delta negative. If I have 100 shares of stock, which is going to be a static Delta, but now I'm selling a call that's only a 15 Delta, now I've got an 85 Delta. So it's important to understand the relationship, and basically, the further out of the money an option goes or is, the smaller the Delta it will be.

The relationship here, even if I create a perfect hedge, when the stock price moves, that hedge is going to change. So that's another thing to be mindful of when we're Delta hedging dynamically. So that's been a lot, but we'll wrap it all together with some top takeaways here.

Hedging can reduce our risk. Instead of just buying 100 shares of long stock, something we can do is create a covered call. So it not only helps us on the downside if the stock price moves down; it increases our probability of profit as well.

So the only thing we're really reducing is our max profit. We don't have that unlimited profitability, but we're having that increased probability of profit, which is going to help us in the long run. Another takeaway is that deploying opposite strategies is our go-to.

Whether that be deploying an opposite strategy in a positively correlated underlying, or if you want to get creative, we can create a bullish strategy in both. For example, if I've got an underlying that is completely negatively correlated with another, if one underlying goes up and it has a negative correlation with another underlying, the other underlying should go down. So if I've got two situations where I know that's true, if I create a bullish scenario in both of those, that's technically a way of hedging one of those positions.

So we can get creative with it, and that's one of the beauties of options trading. Another takeaway is that understanding correlation is key. If I've got a position in Apple, like we talked about in the previous example, and I want to hedge that position elsewhere, maybe I would look to use the Q's (QQQ) or SPY, which is an ETF of the S&P 500.

There are many ways we can hedge. Lastly, we use Delta to measure our hedges, and this is really key, especially when we're getting really down into it and understanding where we want our portfolio Delta to be. It's really important to understand how we can use Delta to hedge that position, but it's even more important to understand that that number is not static.

It will change as the underlyings move. So this has been hedging. Hopefully, you've enjoyed it.

Thanks so much for tuning in. My name is Mike. If you've got any questions or feedback at all, shoot it over to support.

com or support, or you can shoot me a tweet at @TraderMike. We're going to be off tomorrow, but we'll see you on Tuesday. [Music] What's up, everyone?

Thanks for watching our video. Click below to watch more videos, subscribe to our channel, and visit our website.

Related Videos

15:00

Trading Options In A Small Account | Optio...

tastylive

167,677 views

30:26

How 0 DTE Turned This Uber Driver Into A M...

tastylive

381,700 views

57:33

You'll NEVER Buy Stocks Again: Deep in the...

OptionsPlay

77,795 views

28:47

How 0 DTE and 45-day Strategies Took This ...

tastylive

32,659 views

1:03:18

How to Hedge a Portfolio Using Options

OptionsPlay

45,311 views

52:56

The BEST 0DTE Strategies for Profit with T...

OptionsPlay

83,161 views

22:09

How He Trades Full Time with ONE Strategy

tastylive

198,494 views

24:13

How to Trade Covered Calls Properly (The 3...

SMB Capital

492,089 views

15:17

0DTE Options Trading Explained With Examples

projectfinance

135,406 views

35:32

How To Hedge your Portfolio like a PRO (Op...

OptionsPlay

8,957 views

10:58

How to Manage Your Deltas In Options Trading

tastylive

16,846 views

14:08

0 DTE Options: How to Turn a Losing Trade ...

SMB Capital

84,083 views

15:04

“The Bull Market Is Dead” – Tom Sosnoff

tastylive trending

15,859 views

45:20

Revealing the Secrets of Index Options: He...

OptionsPlay

12,214 views

14:59

Credit Strategies For Earnings

tastylive

75,919 views

13:54

Gamma Explained: What is it & How to Trade it

tastylive

176,217 views

12:35

Hedging Explained - The Insurance of Inves...

The Plain Bagel

258,237 views

32:04

Bull Call Spread Tutorial & Trade Examples...

projectfinance

46,073 views

45:35

How to Trade Options for Beginners: Covere...

Charles Schwab

94,479 views

24:40

⚠️ The Risks Of Selling Covered Calls - D...

Rick Orford - Trading Stocks and Options For All

103,760 views